Bitcoin is beating inflation (if you hold on to it long enough)

Also banks stopped the bleeding and perception is all that matters.

Welcome to the Friday edition of the Ecoinometrics newsletter.

Every week we bring you the three most important charts on the topics of macroeconomics, Bitcoin and digital assets.

Today we'll cover:

Bitcoin vs inflation over a multi-year time horizon.

Banks have stopped bleeding depositors money.

Managing perception: the only thing banks needs to do right now.

Each topic comes with a small explanation and one big chart. So let’s dive in.

In case you missed it, here are the other topics we covered this week:

If you aren’t subscribed yet, hit the subscribe button, to receive this email every week directly in your inbox:

Bitcoin is beating inflation (if you hold on to it long enough)

Is Bitcoin a hedge against inflation? The answer depend on what you mean by that.

Some people think that to be a hedge against inflation Bitcoin’s price should rise when inflation is rising and fall when inflation is falling. But honestly that’s asking a bit much. There is no reason for Bitcoin to track the speed at which the Consumer Price Index changes. Even gold (usually accepted as an inflation hedge) doesn’t do that.

A better definition is this one.

Bitcoin is a hedge against inflation over a given time period if it is growing faster than the CPI during the same time window.

Said differently, if Bitcoin’s real return (return adjusted for inflation) over a time period is positive then it is effectively a hedge against inflation.

Now if you play the game of picking a random date in Bitcoin’s history and looking forward to see if it has been growing faster than the CPI then you’ll observe (chart below) that as long as you are considering time periods of at least 4 years then Bitcoin is winning over inflation (sea of blue on the chart).

That should settle the debate: historically Bitcoin is a good hedge against inflation over multi-year time periods.

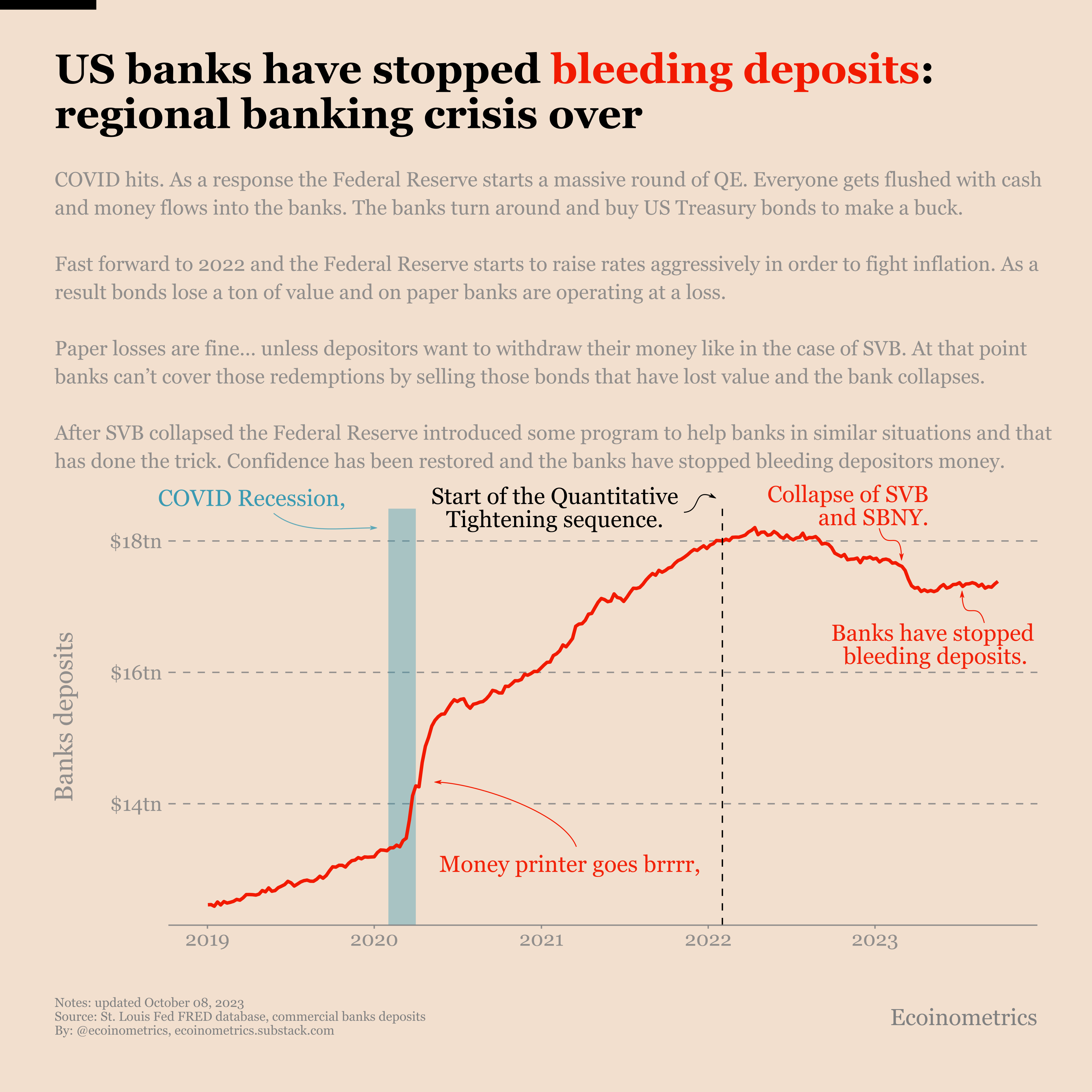

Banks have stopped bleeding depositors money

Arbitrage. That's what banks do with depositors money. You put money in your bank account. The bank turns around and takes that cash to buy US Treasury bonds. They earn whatever the interest is on those bonds. As a depositor you get a small fraction of that back if you are lucky.

Apart from running casinos and peddling SPACs there is no cleaner business model than that.

Except when things go wrong.

Say depositors want their money back. Say you are running a paper loss on your US Treasury bonds. And say you are forced to realize those losses to honour redemptions. Then you (the bank) are in deep trouble.

That's exactly what happened to Silicon Valley Bank, First Republic and SBNY earlier this year.

Higher interest rate since the since the Federal Reserve raised the Fed Funds rate have driven cash out of banks deposits and into money market funds. That's where depositors can actually get returns. That was draining out deposits and creating pressure on the banks.

Then in a few cases we had full blown panics (bank runs) like SVB, FRB, SBNY.

Tough times.

But look at the chart below. Banks have stopped the bleeding. Depositors have seen the Fed has their back. Banks are giving slightly more interests on those deposits. That was enough to keep it under control.

That being said the underlying issue of the bound rout persists.

Managing perception

Continuing on the same theme.

Banks have made a bad trade by getting heavy on US Treasury bonds just as the Federal Reserve was about to raise rates.

But you don't lose money until you sell (said every degenerate gambler I've ever known).

In theory banks can just hold on to those bonds until they mature. Then they will have lost nothing. Zip. Nada. They get the principal plus the interest over that period. (Those interests are lower than they could be but you get my point).

So the only thing that matters to the banks is that they do not face too many customers redemptions at once. Sit tight. Fingers crossed.

And control the public's perception.

That's about the only pro-active thing that banks can do. It works.

Because how many banks have been in real danger since March?

There is like $22 trillion worth of deposits in commercial banks in the US. And the Federal Reserve has put in place a special loan facility at which banks can swap US Treasury for cold hard cash for the value of the principal. How much did this special facility loan since SVB went down? About $100 billion.

That's not much in the grand scheme of things.

What it means is that the banks that really were in real danger of a bank run are really a handful. But the Fed is backing the banks. That’s the important part. The message it sent.

So yes banks will see their margin squeezed. Yes revenue will suck for a while. Yes they will need to dangle some carrots in front of the customer to keep them happy. But if that’s what it takes to maintain the perception that funds are safu. You got to do what you got to do.

That’s it for today. I hope you enjoyed this. We’ll be back next week with more charts.

Cheers,

Nick

P.S. We spend the entire week, countless hours really, doing research, exploring data, surveying emerging trends, looking at charts and making infographics.

Our objective? Deliver to you the most important insights in macroeconomics, Bitcoin and digital assets.

So if you liked this, please refer Ecoinometrics to your friends to help us grow.

Bonus: referrals give you access to the premium content of the newsletter normally only accessible to paid subscribers.

3 referrals give you one month access for free

10 referrals give you 3 months access for free

25 referrals give you 6 months access for free