Ecoinometrics - December 02, 2020

Paper Bitcoin or Physical Bitcoin...

If you are like me you are probably wondering what’s fuelling the current Bitcoin bull run.

One half of the answer is easy. The halving happened earlier this year which means that the supply from mining activities is lower.

Of course the other half of the equation is demand. This part is more tricky.

But one possible reason for the surge in demand is that institutional investors are buying into the store of value narrative and what they want is physical Bitcoin.

The Ecoinometrics newsletter decrypts Bitcoin’s place in the global financial system. If you want to get an edge in understanding the future of finance you only have to do two things:

Click on the subscribe button right below.

Follow Ecoinometrics on Twitter at https://twitter.com/ecoinometrics.

Done? That’s great! Thank you and enjoy.

Paper Bitcoin or Physical Bitcoin

That’s it, this week Bitcoin is back to its all time high. The exact number doesn’t really matter but we are just short of $20k.

But things feel quite different from the last time that happened.

At the peak of the 2017 bull run everyone and their dog would ask me if it was a good time to buy.

It felt like Bitcoin was on everyone’s mind even though in practice not that many people bought around the top as it happened so fast.

I’m saying everyone was interested but actually as I recall not that many of the professional investors in my circle looked into it.

Fast forward to 2020 and the situation is reversed.

For sure there is some interest in Bitcoin from the general public. But mostly it is the professional investment world which is warming up to it.

With that comes the potential of a large influx of money into the Bitcoin network that should change its status from aspirational store of value to actual store of value whose size is at least a large fraction of the gold market.

What I find the most interesting in that story is that professional investors are really buying into the Bitcoin as digital gold narrative.

This is not a pump and dump scheme orchestrated by Grayscale as suggested by Peter Schiff...

Think about it for a minute.

We are in 2020. If institutional players wanted to make a short term play on Bitcoin they now have access to very large regulated derivative exchanges such as the CME on which they can trade paper BTC.

For them that would be easy or at least easier than having to worry about Bitcoin custody. And on top of that they could trade with all the leverage they want.

When you trade cash settled paper assets at the end of the day everything is just a balance sheet game.

But this is not what’s happening.

Despite BTC rushing back to all time high, the amount of open positions is not trending up on the CME Bitcoin futures.

Sure, when denominated in US$ the open interest is at an all time high level with more than $1 billion worth of positions. Still that’s below the peak number of contracts recorded last summer.

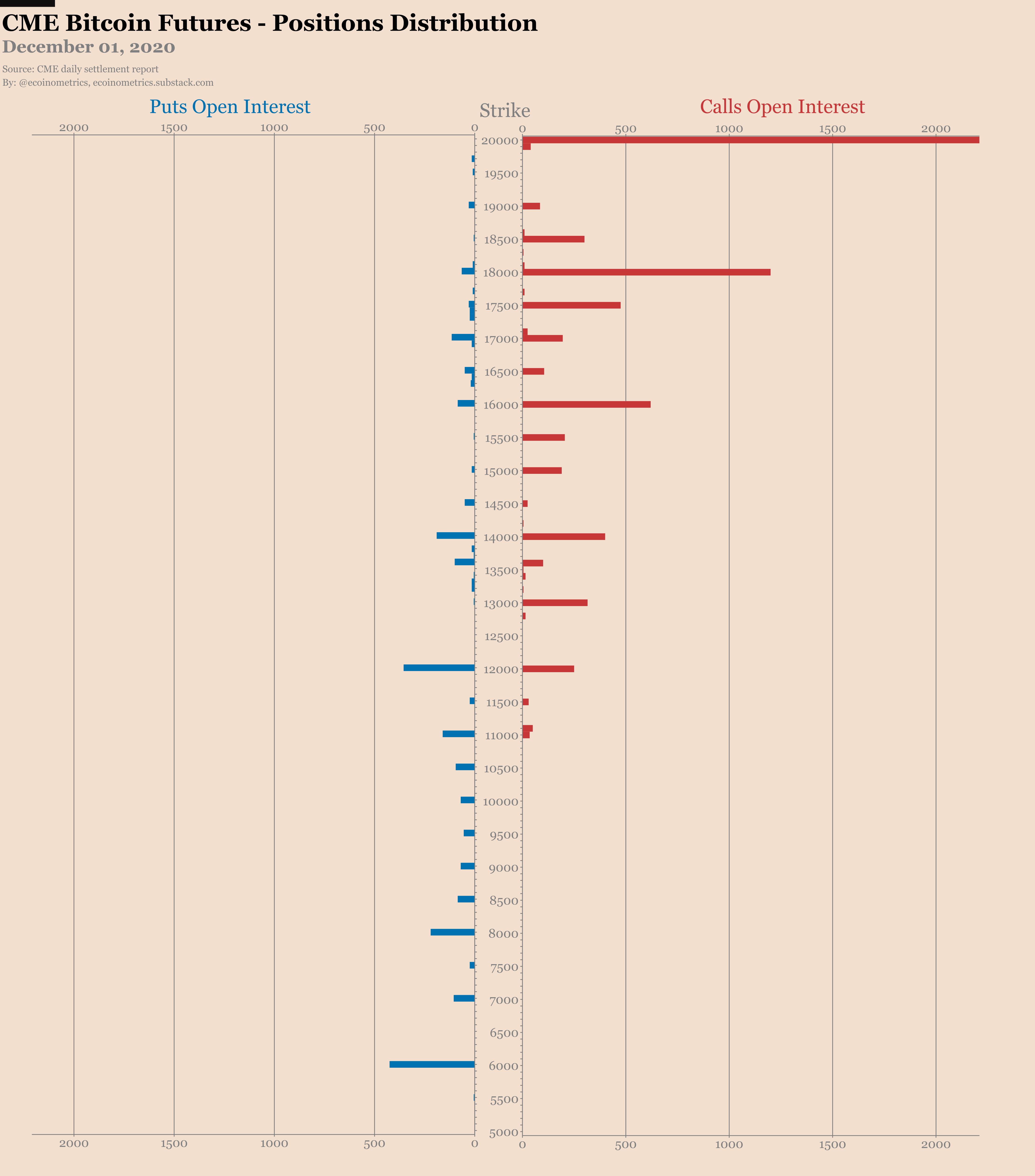

And it is not like traders have chosen to use options instead. On the CME Bitcoin options market the trend is even worse.

The number of open positions continues to decline.

There is a good number of far out of the money positions betting on BTC moving way past $20k in the next 12 months. But the total value they capture does not scream massive institutional interest.

Check it out.

The picture is even more interesting when you dig deeper into the latest Commitment of Traders report.

For retail traders not much as changed in terms of net positions.

Still net long although far from record levels.

When you look at the details though it is surprising to see that the amount of short positions is growing.

I don’t really believe some retail traders are shorting this BTC move. So these are either hedging long positions from somewhere else or they are an attempt for retail traders to put up some basis trade.

That means they are long spot BTC and short the futures at the same time to capture the futures premium over spot.

This basis trade idea has legs. Just look at what the smart money is doing…

Pretty big increase in the amount of short positions for them.

That makes sense if you consider that last week combined a strong Bitcoin momentum with the last trading days on the derivatives contracts. Those are all conditions that tend to increase both the time spreads and the premium of futures over spot BTC.

This time hedgers took the other side of the trade. They are now at a record net long position.

These guys' whole strategy normally is to be neutral so they must be short BTC somewhere to balance their book.

What is lacking from all this is institutional money piling in on the momentum trade.

So I continue to be surprised by the lack of trend following play on the futures market.

Maybe the kind of institutional players that would put on that trade still considers the Bitcoin market too small to be worth it.

Or… maybe it is simply that many institutional players are really buying into the store of value narrative.

In that case they wouldn’t want to own paper Bitcoin. They’d want to get as close as possible to owning physical Bitcoin.

That could be what’s currently fuelling demand in the market and moving the price back to record level.

We can’t know for sure at the moment. But we might get a clue when we see the Bitcoin treasury holdings expand over the next 12 months.

Regardless don’t forget that Bitcoin is one of those rare asymmetric bets that is not reserved to elite institutional players.

You can be part of it too.

All you have to do is start stacking sats now!

That’s it for today. If you have learned something please subscribe and share to help the newsletter grow.

Cheers,

Nick

The Ecoinometrics newsletter decrypts Bitcoin’s place in the global financial system. If you want to get an edge in understanding the future of finance you only have to do two things:

Click on the subscribe button right below.

Follow Ecoinometrics on Twitter at https://twitter.com/ecoinometrics.

Done? That’s great! Thank you and enjoy.