Ecoinometrics - December 09, 2020

MicroStrategy is going all in...

On Monday we heard that MicroStrategy is trying to raise another $400 million to buy more Bitcoin just as BTC is at its all time high.

Ballsy move by Michael Saylor.

The original plan was for MicroStrategy to preserve the purchasing power of its cash reserve by converting it to Bitcoin.

But that worked so well that they are raising the stakes.

That’s what I call going all in...

The Ecoinometrics newsletter decrypts Bitcoin’s place in the global financial system. If you want to get an edge in understanding the future of finance you only have to do two things:

Click on the subscribe button right below.

Done? That’s great! Thank you and enjoy.

Michael Saylor’s bet

Some investment opportunities are obvious. You hear about something, do your own research and BANG! the truth smacks you in the face.

When you watch interviews of Michael Saylor, the CEO of MicroStrategy (MSTR), it seems to be exactly what happened to him.

Whether all that is true or not, it is still a good story. And the result is the same, MicroStrategy has a plan.

In case you haven’t followed the whole story let me summarize. It is really simple:

As a business MicroStrategy generates a lot of excess cash.

That excess cash goes into their treasury where it sits doing nothing.

Now thanks to asset price inflation you don’t want to keep your cash not invested since it is losing its purchasing power over time.

MicroStrategy decided that converting all their excess cash into Bitcoin was the best way to preserve its purchasing power over the long run.

Their plan until now was to convert all their excess cash reserves to Bitcoin:

In August 2020 they purchased $250 million worth of BTC.

In September 2020 they purchased another $175 million worth of BTC.

In early December 2020 they added $50 million worth of BTC to their treasury.

This is just stacking sats for businesses.

So how is this strategy working for MicroStrategy?

I’d say it is working great.

Take a look at the stock performance of MicroStrategy this year.

Until August there wasn’t much to write home about. The year started pretty much flat until March when MSTR dropped like everyone else.

From March to August the NASDAQ pushed higher thanks to the FAANG stocks. Over that period MicroStrategy remained flat.

Then in August Michael Saylor started to be very public about his Bitcoin treasury move. Since then MSTR has outpaced the NASDAQ to follow the parabolic rise of Bitcoin.

So when it comes to its stock price, this is a mission accomplished for MicroStrategy.

On top of that their Bitcoin bet itself is paying off. They are currently hodling 40,824 BTC for a 63% return on investment.

For sure that’s better than buying bonds with negative real yield...

Again so far Michael Saylor’s strategy makes sense.

Then comes the new move. MicroStrategy announced that they are planning to raise more cash with the explicit goal of buying more Bitcoin.

That’s quite different from the idea of stacking sats for business isn’t it.

Stacking sats for business means that you generate cash reserves and convert those to Bitcoin reserves in a store of value play.

But the store of value play is only half the story.

As I’ve noted countless times the other part of the Bitcoin investment thesis is that we are early on an adoption curve that will see BTC compete directly with gold.

And that means asymmetric returns for those who can accumulate Bitcoin early.

With institutional investors starting to get their eyes on Bitcoin as a store of value who knows how long the asymmetric bet opportunity will remain open.

My guess is maybe 10 years. However the longer you wait to accumulate the lower your potential returns.

I’m guessing this is the kind of calculus that Michael Saylor is doing.

Which is why MicroStrategy is trying to boost the rate at which it is stacking sats by trying to raise some debt.

That’s an interesting play and it raises some questions regarding how you are supposed to value MicroStrategy.

MSTR current market cap is in the low single digits billion dollars. That means their Bitcoin treasury is a significant fraction of their market cap, around 30%.

As you have seen on the year to date performance chart MicroStrategy has already started decoupling from the NASDAQ and moving more and more in parallel with Bitcoin.

Obviously that only started a few months ago so there isn’t that much data yet. However you don’t need too much data to follow the logic.

From 2019 to the start of MicroStrategy’s Bitcoin treasury investment program MSTR had a +51% correlation to the NASDAQ and a +22% correlation to Bitcoin.

Since the start of their BTC treasury investment program earlier this year MSTR correlation has flipped to +21% with the NASDAQ against +52% with Bitcoin.

The more aggressive Michael Saylor gets with this Bitcoin play, the more BTC are accumulated by MicroStrategy, the more MSTR will get correlated with Bitcoin.

At what point MSTR will turn into something like a SPAC for a Bitcoin ETF? Who knows. But this is definitely something we are going to follow.

CME Bitcoin Derivatives

This week’s tour of the CME cash settled Bitcoin derivatives is once again going to be quick.

There is nothing happening.

For weeks now the open interest has flatlined and except for the traded volume spike that came around the expiry of the November contract the level of activity is low.

It looks even lower when you consider that Bitcoin is holding pretty well in the $18k to $20k range.

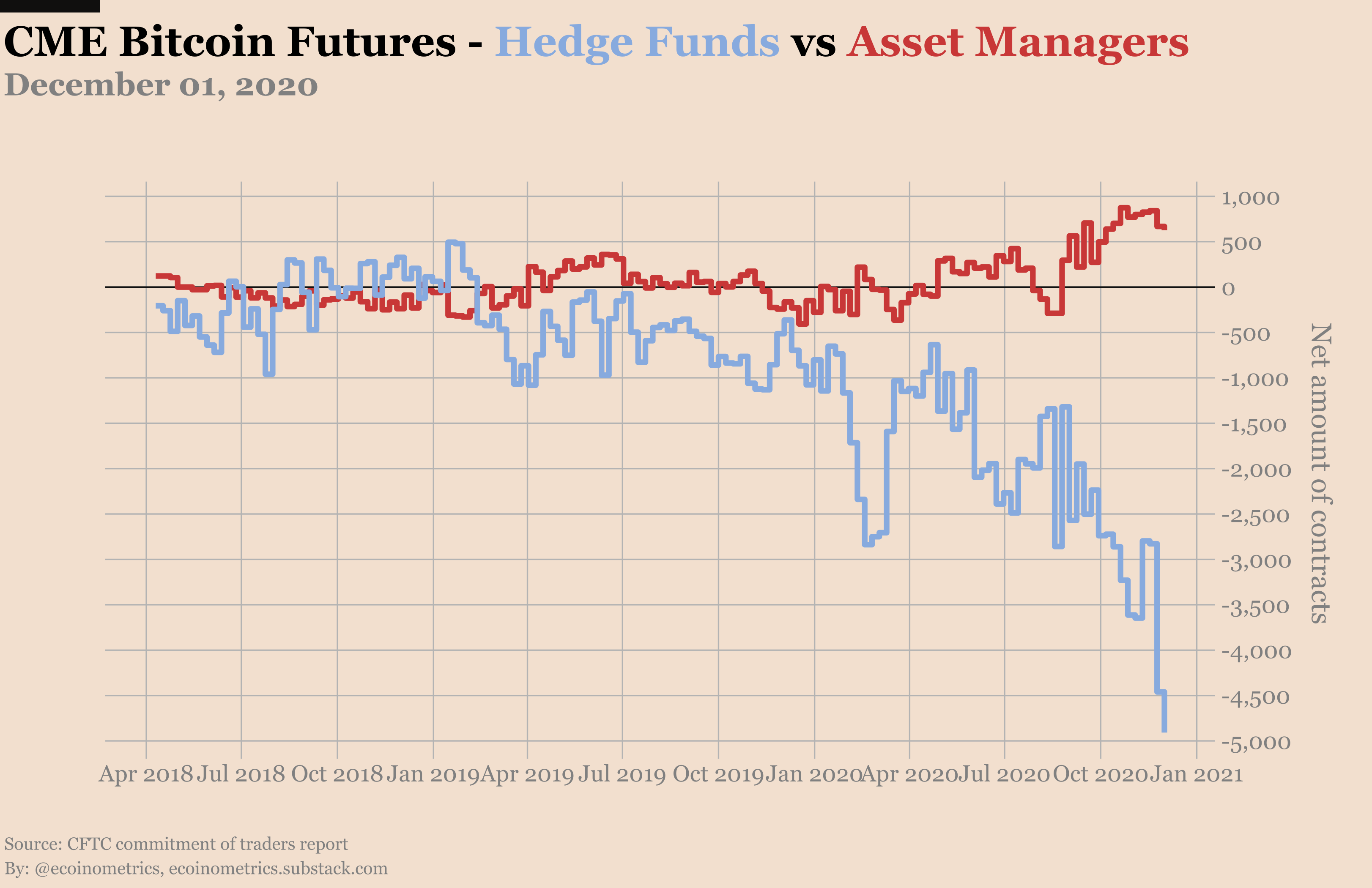

According to the most recent Commitment of Traders data, retail traders have dropped their short positions. But as you can see it doesn’t mean they have turned ultra-bullish instead.

Well at least retail traders are net long. Because by comparison the smart money has never been so short.

Of course as usual these are unlikely to be net short positions. The most likely explanation is that those short positions are part of the arbitrage play between the spot market and the futures market. Apparently the basis trade has never been so juicy.

Earlier this fall it looked like we were starting to see a real divergence between leverage funds and asset managers:

Leveraged funds were playing the arbitrage game with the basis trade. This placed them always more short the BTC futures.

Asset managers were building some trend following positions getting more and more long the BTC futures.

While leveraged funds continue to milk the basis trade, asset managers have stopped adding to their long positions.

My guess is that they might have turned to getting long on the Bitcoin spot market instead. But at the moment we don’t have enough data to confirm that thesis.

Meanwhile the options market continues to be a ghost town.

Half of the calls are already in the money this month. However that doesn’t seem to encourage traders to take more risk.

The activity on the options market is losing momentum. Consider the following statistics:

Three months ago 34% of all positions were on the near month.

Two months ago 48% of all positions were on the near month.

One month ago 30% of all positions were on the near month.

This month 74% of all positions are on the near month…

That means options traders are not creating new far dated positions to express their long term view.

Maybe a break above $20k will revive the market. But I’m not holding my breath. Bitcoin is a spot game these days.

That’s it for today. If you have learned something please subscribe and share to help the newsletter grow.

Cheers,

Nick

The Ecoinometrics newsletter decrypts Bitcoin’s place in the global financial system. If you want to get an edge in understanding the future of finance you only have to do two things:

Click on the subscribe button right below.

Done? That’s great! Thank you and enjoy.