Ecoinometrics - March 01, 2021

Ecoinometrics - March 01, 2021

Where are we now?

There is still a couple of months before the first anniversary of the 3rd halving but now isn’t a bad time to see how much progress has been done.

So how close are we from Bitcoin’s next milestone?

The Ecoinometrics newsletter decrypts Bitcoin’s place in the global financial system. If you want to get an edge in understanding the future of finance you only have to do two things:

Click on the subscribe button right below.

Done? That’s great!

Now let’s dive in.

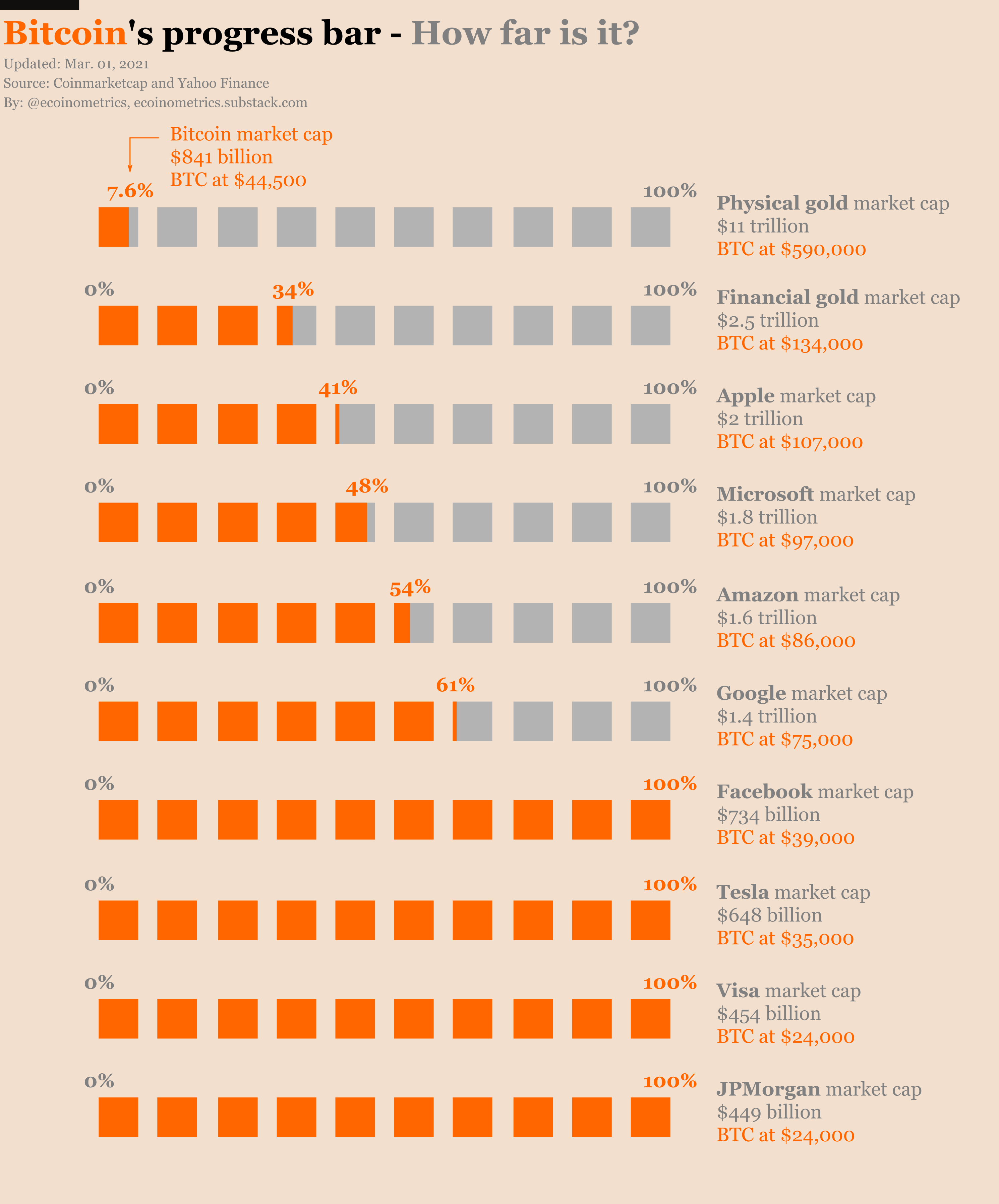

Progress status

A few weeks ago I talked about the Bitcoin ABZ framework. Go read that if you need a refresher, but the conclusion was that the next big step for Bitcoin is to become larger than any company listed in the stock market.

Getting there would go a long way in showing that the real market for Bitcoin is indeed closer to physical gold than it is to a more standard asset.

So how are we doing on that front?

Not bad. Not bad at all.

Bitcoin is already larger than JPMorgan, larger than Visa, larger than Tesla and larger than Facebook.

There are only a handful of mega cap stocks that are still larger than Bitcoin:

Apple $2 trillion market cap.

Microsoft $1.8 trillion market cap.

Amazon $1.6 trillion market cap.

Google $1.4 trillion market cap.

Apple like the rest of the tech sector is suffering from the recent rise in bonds yields. As a result it is a lower target for BTC.

At the current AAPL price we need one BTC at $107k to make the flippening happen.

We haven’t even celebrated the one year anniversary of the 3rd halving so it feels very likely we’ll get there during this cycle.

Check it out.

But once Bitcoin flips Apple there is another very close target that we should watch out.

In the previous chart I’ve called that one “financial gold”. What I mean by financial gold is the fraction of the physical gold market that is used directly in traditional investment vehicles like say gold ETFs and such.

I haven’t done any attempt at estimating this myself but some googling gives a ballpark figure of $2.5 trillion for this category.

That’s actually very close to the market cap of Apple. We would only need BTC to get to $134k per coin to get there.

This target also seems within reach during this cycle and it would certainly be a big milestone for the digital gold narrative.

Looking forward to it.

Coinbase IPO

Coinbase is about to be listed so get ready for a new entry in the Bitcoin Treasuries Index.

According to the prospectus for their IPO, Coinbase had $130.1 million worth of Bitcoin as of December 31 last year. Given where BTC was trading at the close on that day we can estimate that they hold about 4,342 Bitcoins in their treasury.

That’s… not a lot.

For comparison Marathon Patent Group (a miner) has 4,813 BTC and Tesla has more than 10 times as many Bitcoins on their balance sheet.

But it isn’t very surprising either.

The prospectus only gives us their income statement over the past two years but two things are clear:

While they made money during 2020, in 2019 Coinbase was losing money ($46 million operating loss).

From 2019 to 2020 their operating expenses are up significantly (about 3x).

That screams a positioning for growth in order to gain as much market share as possible.

When you are positioned for growth, using the cash you get to purchase more Bitcoins is not your priority.

The investors who backed Coinbase didn’t give them money to buy Bitcoin. Those investors don’t need Coinbase for that. What they want is growth.

The larger the crypto market the larger the expected revenue for Coinbase.

So in that sense the value of the business is already tied to the success of Bitcoin (BTC represents 70% of the assets held on Coinbase). Spending cash now to maximise your market share and thus your future revenues as the crypto market becomes larger is not a stupid idea.

That probably explains the relatively small Bitcoin reserve.

Let’s see how that plays out.

Central Bank Digital Currencies

Here is a research paper tied to the Swiss National Bank on how to issue a Central Bank Digital Currency that would “replicate physical cash” without affecting “monetary policy or financial stability”.

This paper essentially explores how a central bank could design a CBDC for retail users i.e. an electronic version of physical cash.

Spoiler alert, their solution completely forgo the idea of using a blockchain for that purpose. Instead their CBDC is essentially a centralized database managed by the central bank where retail users keep an account.

At this point you are probably thinking “how is that an innovation, isn’t fiat money mostly digital already?”.

True.

But there is a significant difference that is captured within the paper:

A significant difference between central bank money and privately issued commercial bank money is, therefore, that the latter entails counterparty risk. A central bank can always meet its obligations using its own nonredeemable money. Central bank money is the only monetary asset in a domestic economy without credit and liquidity risk. Therefore, it is typically the preferred asset to settle payments in financial market infrastructures.

For the most part we as private citizens deal with money in the banking system. Individuals don’t have accounts at the central bank.

Banks are the intermediary between the retail users and the central bank. And as we can see with the decline in the velocity of money that’s a problem.

Even if the Fed injects money in the banking system by increasing bank reserves, there is no guarantee that the banks will make that money flow all the way to retail users issuing loans.

This is arguably one of the reasons why the monetary policy of the Federal Reserve has failed to achieve their goals of a 2% target CPI inflation for so long despite the amount of liquidity put into the system.

The Federal Reserve can issue money but they need either the banking system (via loans) or the Federal Government (via fiscal policy) to make that money flow.

That is why retail oriented CBDCs are so tempting for central banks. This is not a story about a technological revolution. This is a story about a monetary system evolution where central banks disintermediate from the government and the banks.

In that world the algorithmic monetary policy of Bitcoin, as an island of stability, might end up being worth way more than we can imagine now.

That’s it for today. If you have learned something please subscribe and share to help the newsletter grow.

Cheers,

Nick

The Ecoinometrics newsletter decrypts Bitcoin’s place in the global financial system. If you want to get an edge in understanding the future of finance you only have to do two things:

Click on the subscribe button right below.

Done? That’s great!