Ecoinometrics - March 17, 2021

Ecoinometrics - March 17, 2021

Catching up...

The US still does not have a Bitcoin ETF. There are plenty of other options though.

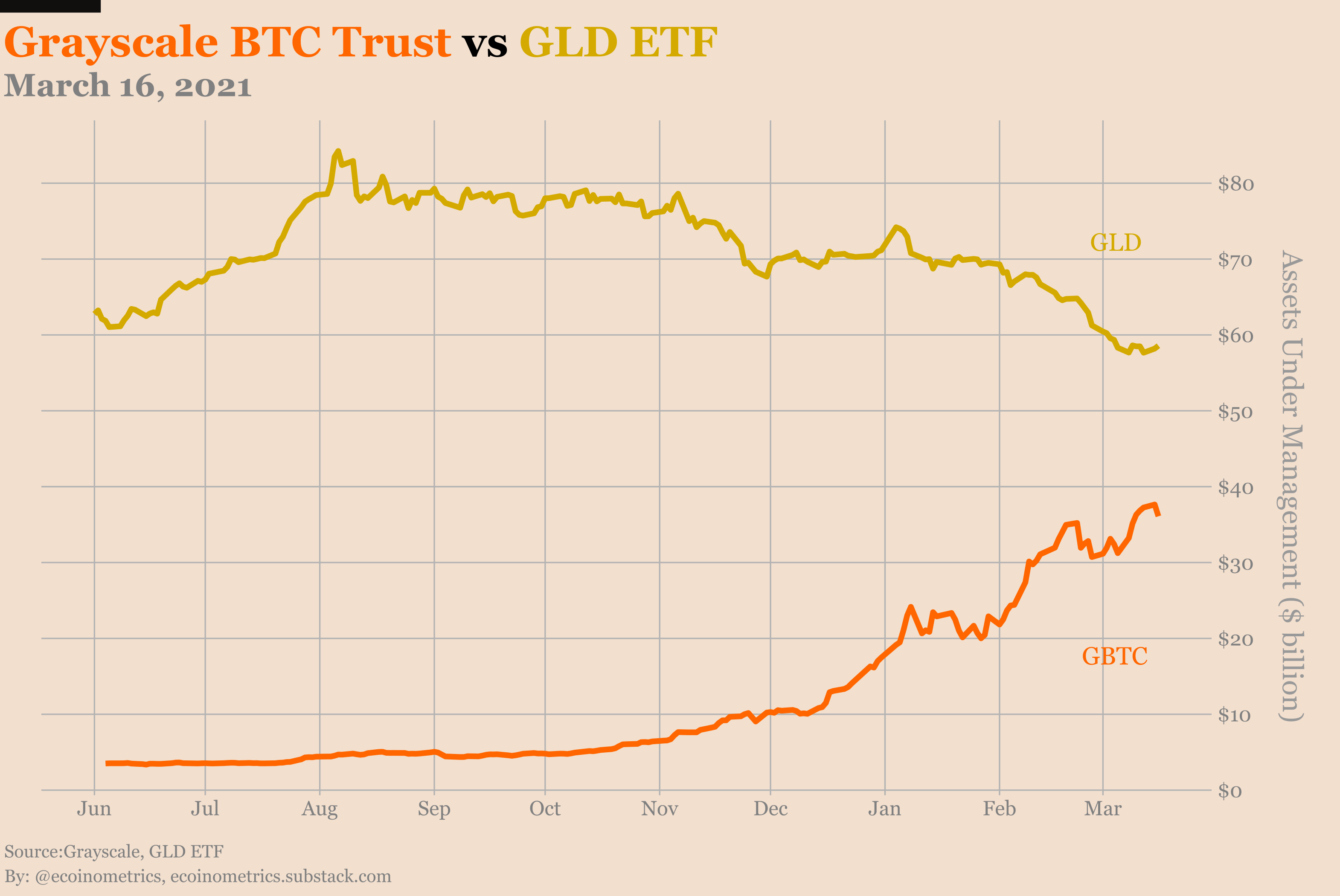

Of those options the Grayscale Bitcoin Trust is as close as it gets to fulfilling the role of THE Bitcoin ETF of reference.

And it is catching up to GLD… fast.

The Ecoinometrics newsletter decrypts Bitcoin’s place in the global financial system. If you want to get an edge in understanding the future of finance you only have to do two things:

Click on the subscribe button right below.

Done? That’s great! Now let’s dive in.

Catching up

Last time I checked on Grayscale vs GLD (the major gold ETF) Bitcoin was trading at $23k and gold was trading at $1,860.

Fast forward three months later:

One Bitcoin is now worth about $56,000.

One ounce of gold is now worth about $1,730.

So yes, it is not very hard for BTC to chase a target that has been shrinking.

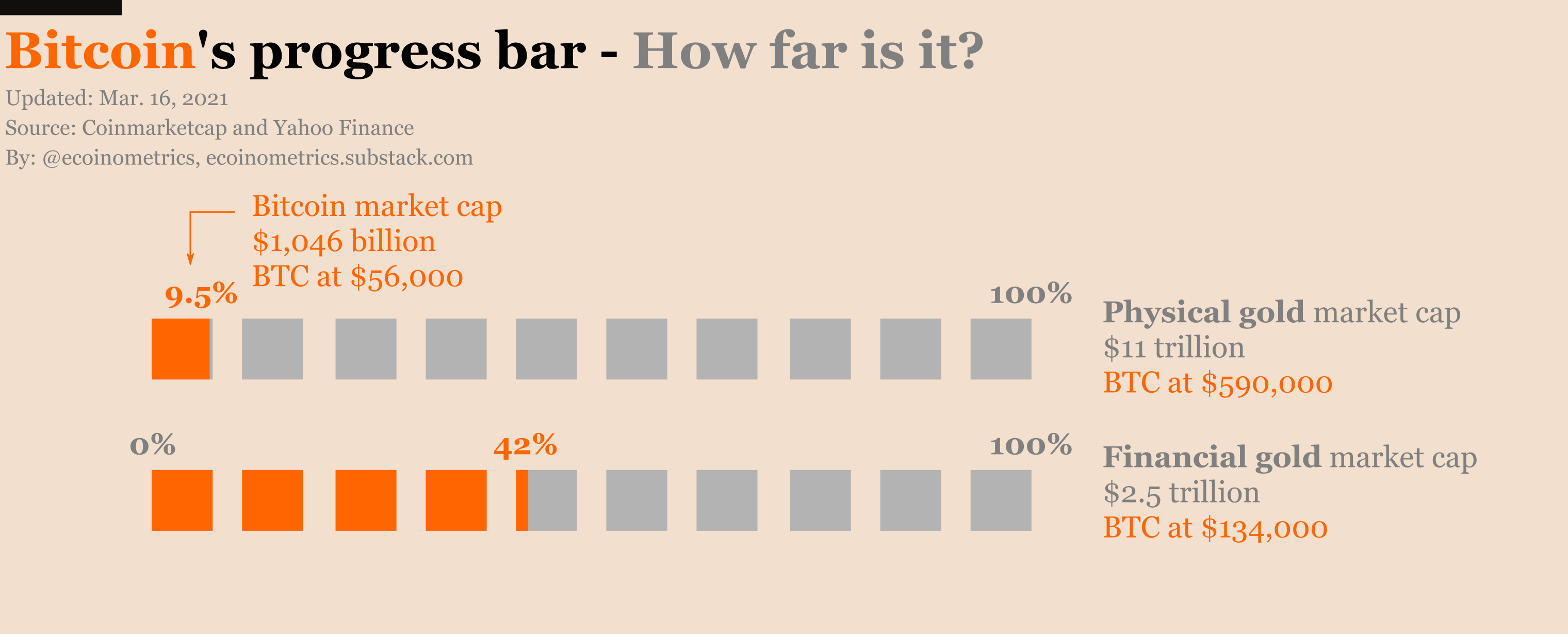

The three numbers I like to observe when comparing Bitcoin to gold are:

How large Bitcoin is relative to the market size of physical gold.

How large Bitcoin is relative to the market size of financial gold (the part of physical gold that is wrapped in financial instruments).

How large GBTC is relative to the assets under management of GLD.

Bitcoin is 10% of the market size of gold and it captures 42% of the market size of financial gold.

Meanwhile the Grayscale Bitcoin Trust assets under management represent 62% of that of the GLD ETF.

If GLD stabilizes at those levels and Grayscale does not see any major inflow or outflow the flippening should happen when Bitcoin trades around $90k.

Which means that we could see the de-facto “Bitcoin ETF” get larger than the major gold ETF this year.

That would certainly be another milestone for the “Bitcoin is digital gold” narrative.

But I guess there are a few reasons why this might not happen.

One reason is that gold could start rising sharply. Honestly I don’t see that happen. The US 10-year yield has been rising a lot this year and obviously that’s bad for gold. Even if we had some inflation scare my guess is that it would benefit Bitcoin more than gold.

The other reason is that, even without a Bitcoin ETF available in the US, Grayscale has more and more competition.

You are no longer limited to GBTC if you want to have some long exposure to Bitcoin. MicroStrategy is clearly positioned as a pseudo-ETF but you can see that there are a host of smaller public companies holding BTC on their balance sheet offering various degrees of exposure for those who are interested.

Some of those companies are miners like Marathon, Riot or Hut 8. Others are just hodlers with big exposure like Galaxy Digital and so on.

My point is that investors looking to get some indirect exposure to Bitcoin have a lot of choices. They don’t have to bet on GBTC and that might slow their growth.

But we’ll see how that plays out.

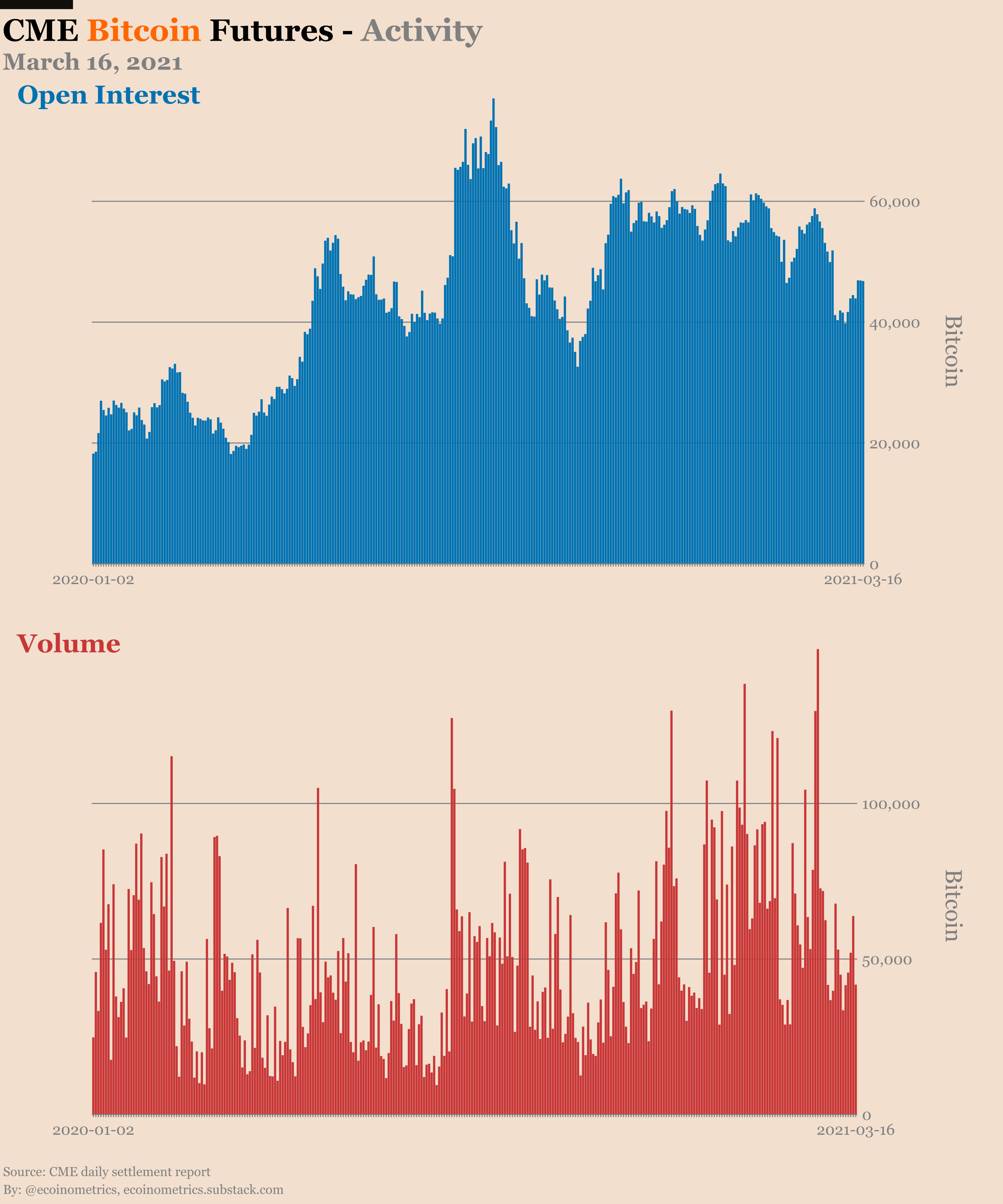

CME Bitcoin Derivatives

It looks like things have settled down on the CME Bitcoin derivatives. The theme over the past few weeks had been deleveraging:

Retail traders closed more than a quarter of their long positions.

The smart money closed a third of their short positions while the long positions hit a low of 10,000 BTC worth of contracts.

But all that stopped last week. It didn’t stop with a reversal though. And one week does not make a trend. So we’ll have to see where this is going.

For the big picture there is no change. The open interest expressed in BTC has peaked last year when we got the early breakout above $10k.

Back when that happened I had guessed that the open interest would continue to climb. I was wrong.

My idea was that the bull market would trigger trend following kind of strategies to get after Bitcoin. That would have significantly increased the amount of long positions on the CME futures.

Obviously we didn’t see that.

Instead the basis trade, which is an arbitrage strategy, kept expanding.

Thinking about it now there are a couple reasons why the trend following trade using the CME futures is not very popular.

First you have the volatility. To manage these kind of trend following positions you typically decide on your position size based on the volatility of the asset. The larger the volatility the smaller the position size. That constraint might cap out your position size on the CME pretty fast given that each contract is the equivalent of 5 BTC.

Second there is the amount of available options to get long Bitcoin. These days you can hodl Bitcoin, buy futures on a host of crypto-exchanges, buy GBTC, buy MicroStrategy or do a Bitcoin miners play. With many options available it might be that there is no winner takes all asset that captures everyone who wants to play the momentum trade.

There might be other reasons but those are the most obvious.

Now let’s move on to the CME Bitcoin options market. Traders are buying puts. There are now 3 puts for every 4 calls. That’s as high as we have seen the puts to calls ratio in a year.

Most of the recent puts are concentrated in the $40k to $60k strikes range. So my guess is that they are more protective puts than bets on the bull market actually tanking.

That kind of checks out with the constant rise of the number of puts relative to the calls since January.

Keep in mind that there is only a limited amount of information we can get from those options. The market has been shrinking for months and we are left with about 1,500 open contracts as I write those lines. That’s the equivalent of 7,500 BTC...

That’s it for today. If you have learned something please subscribe and share to help the newsletter grow.

Cheers,

Nick

The Ecoinometrics newsletter decrypts Bitcoin’s place in the global financial system. If you want to get an edge in understanding the future of finance you only have to do two things:

Click on the subscribe button right below.

Done? That’s great!

I love these articles showing up in my inbox. Thank you very much