Ecoinometrics - Monetary regime risk

September 01, 2021

When central banks pump trillions of dollars into the financial system it is easy to feel like an investment genius. The strategy is simple: stonks go up.

But with inflation running a bit hot, we might see the Federal Reserve trying to taper their purchasing program at some point.

What are the risks associated with that? Let’s have a look.

The Ecoinometrics newsletter decrypts Bitcoin’s place in the global financial system. If you want to get an edge in understanding the future of finance you only have to do one thing, click on the subscribe button right below:

Done? Thanks! That’s great! Now let’s dive in.

Monetary regime risk

Flashback to March 2020. COVID is hitting the US and the stock market which had totally ignored that until then is in for a big correction.

From the previous top, the SP500 drops no less than -35%.

But this correction wasn’t confined to the stock market. The reason is simple:

Investors didn’t expect a large dip, instead many were geared for leverage.

When the dip happened all those leveraged investors had to face margin calls.

But to raise the necessary cash to meet those calls they had to sell some other assets.

Result, everything (even gold or Bitcoin) got sold off to get liquidity.

That’s what it was. In a liquidity crisis, everything ends up becoming correlated.

Obviously the Federal Reserve doesn’t like it when the stock market goes down. As far as they are concerned, the stock market is the economy.

They do have an easy way to fix that though: just print money, buy assets with it and pump the market with liquidity.

And so they did exactly that...

Almost $3 trillion was added to the Fed’s balance sheet in just a few weeks last year. Now we are at $4 trillion and counting. For scale this is more than they did in the entire 12 years that followed the 2008 financial crisis.

With the financial markets drowning in liquidity the stock market is once more breaking new records regularly. For reference, the SP500 is up +34% from the top BEFORE the March 2020 correction...

But as we just said, this bull market is fuelled by money printing… which means that one major risk here is well… the Fed stopping to do so. And who knows if we might not get another liquidity crisis that would bring down Bitcoin as a result.

So. Can we quantify that risk?

Well, we can try.

To stay at a high level we can say that there are two kinds of broad monetary conditions:

Expansion i.e. the Fed is expanding its balance sheet.

Contraction i.e. the Fed is reducing the size of its balance sheet.

To capture those two regimes let’s say that we are in expansion when the Fed’s balance sheet is growing on a 4 weeks average basis and in contraction otherwise.

Now the things we really care about are the stock market drawdowns. So let’s see what those look like depending on the monetary regime.

We’ll use the SP500 as our representation of the stock market and since we only really care about the new normal we’ll focus on the time period starting in January 2007.

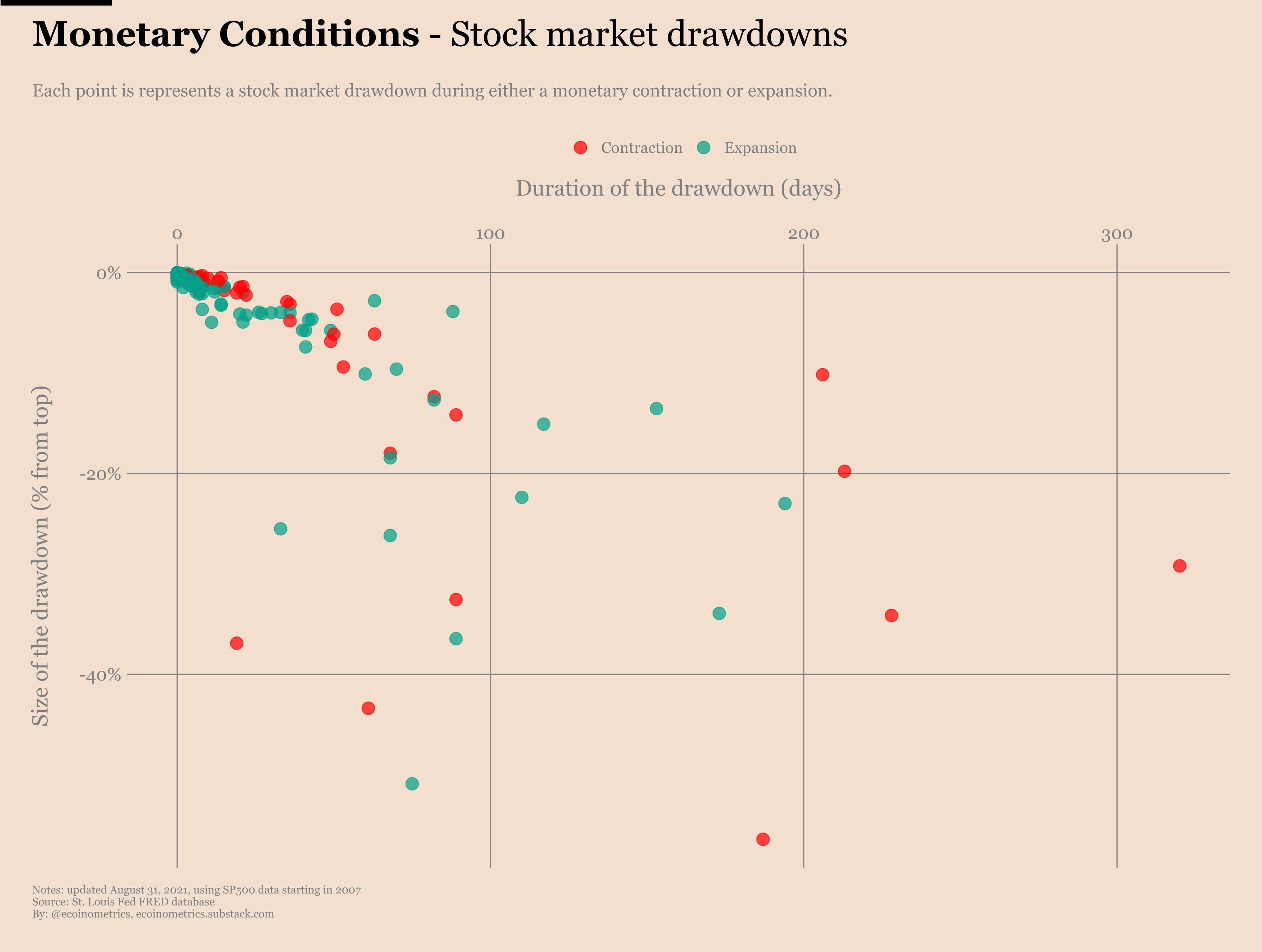

First stop, the distribution of the drawdowns by size.

Checkout the chart below.

Each point is a drawdown. On the horizontal axis you get the size of the drawdown which is the percentage drop from all-time high to bottom. In green you have the drawdowns that happened during an expansion phase, in red those that happened during a contraction phase.

At first sight there are no big differences between the two regimes. Both have drawdowns of all sizes. Both see drawdowns concentrated below the 5% mark.

What if we expand this chart to add the duration of each drawdown?

Take a look. The size of the dip is on the vertical axis (reverse order) and duration is on the horizontal axis.

Ok so if we are looking at the upper left quadrant (short duration and smaller corrections) there is not much difference between the two regimes.

But if you move towards long durations then the red dots become more prevalent. I guess this one is pretty intuitive. When the Fed is not adding liquidity to the system, it takes longer to get out of drawdowns.

Now, to quantify the risk associated with a change of monetary regime by the Fed is asking the following question:

How much more likely are you to see corrections when the Fed is contracting its balance sheet?

Since 2007 we have been more often in the expansion regime than in the contraction regime. So what we need to quantify is: relative to the number of trading days spent in each regime, how much more frequent are the corrections during a contraction regime?

When we run the numbers on this one, here is what we get:

If you consider all sizes of corrections then dips are 30% less frequent during a contraction phase than during an expansion phase. Hmmm...

Wait, actually that makes sense because the bigger corrections tend to be more frequent during contractions:

The dips larger than -5% are 30% more frequent.

The dips larger than -10% are 60% more frequent.

The dips larger than -20% are 40% more frequent.

So tl;dr when the Fed is not flooding the market with always more liquidity you are more likely to get bigger corrections.

And if you consider that corrections larger than -10% are very likely to also impact other markets, then that means if the Fed starts tapering we increase the risk of seeing a negative impact on Bitcoin by 60%.

To be fair we are far away from the Fed tapering and Jay Powell is sufficiently vague in his statements that it might never happen for all we know.

But still that’s a risk to keep in mind.

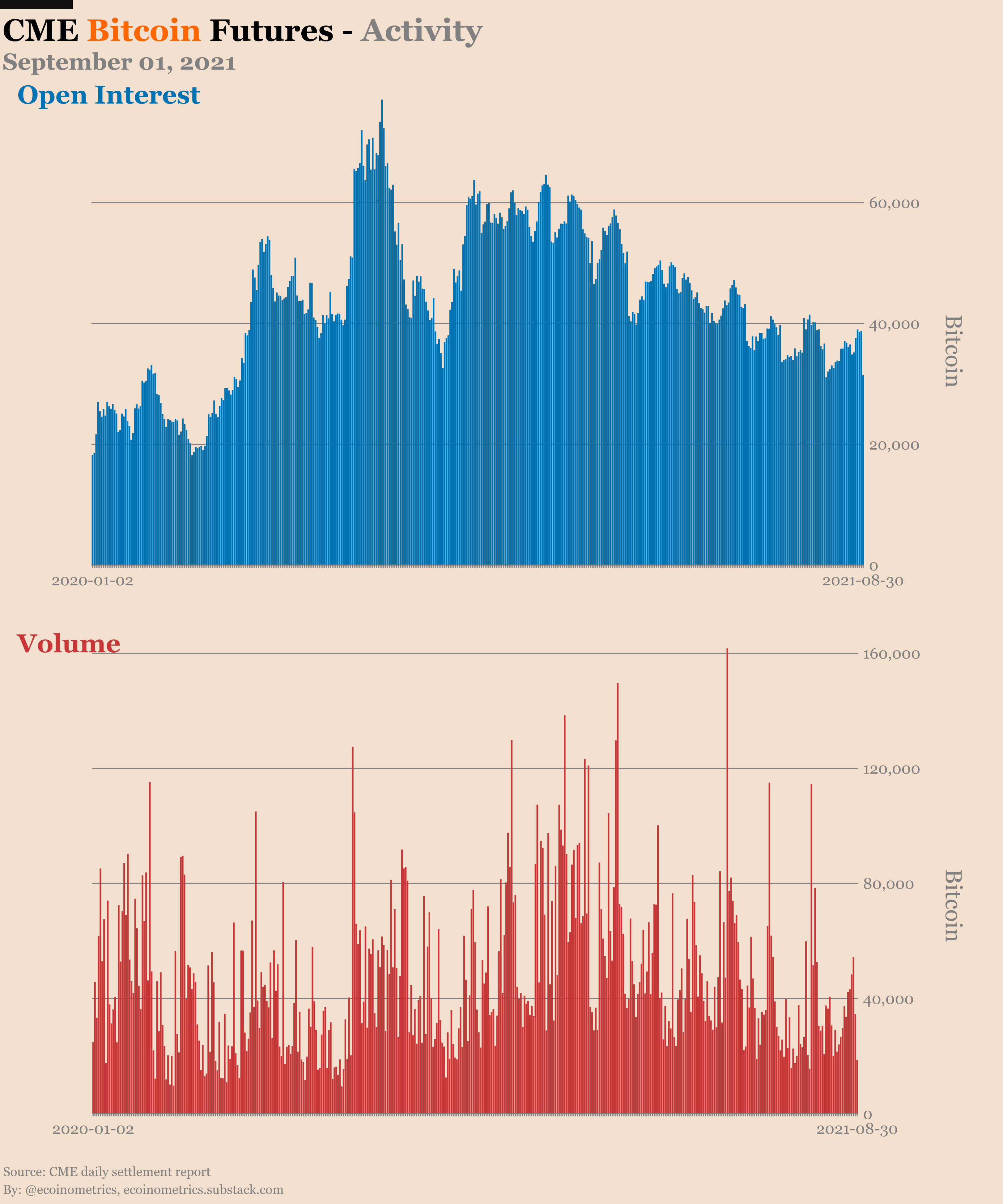

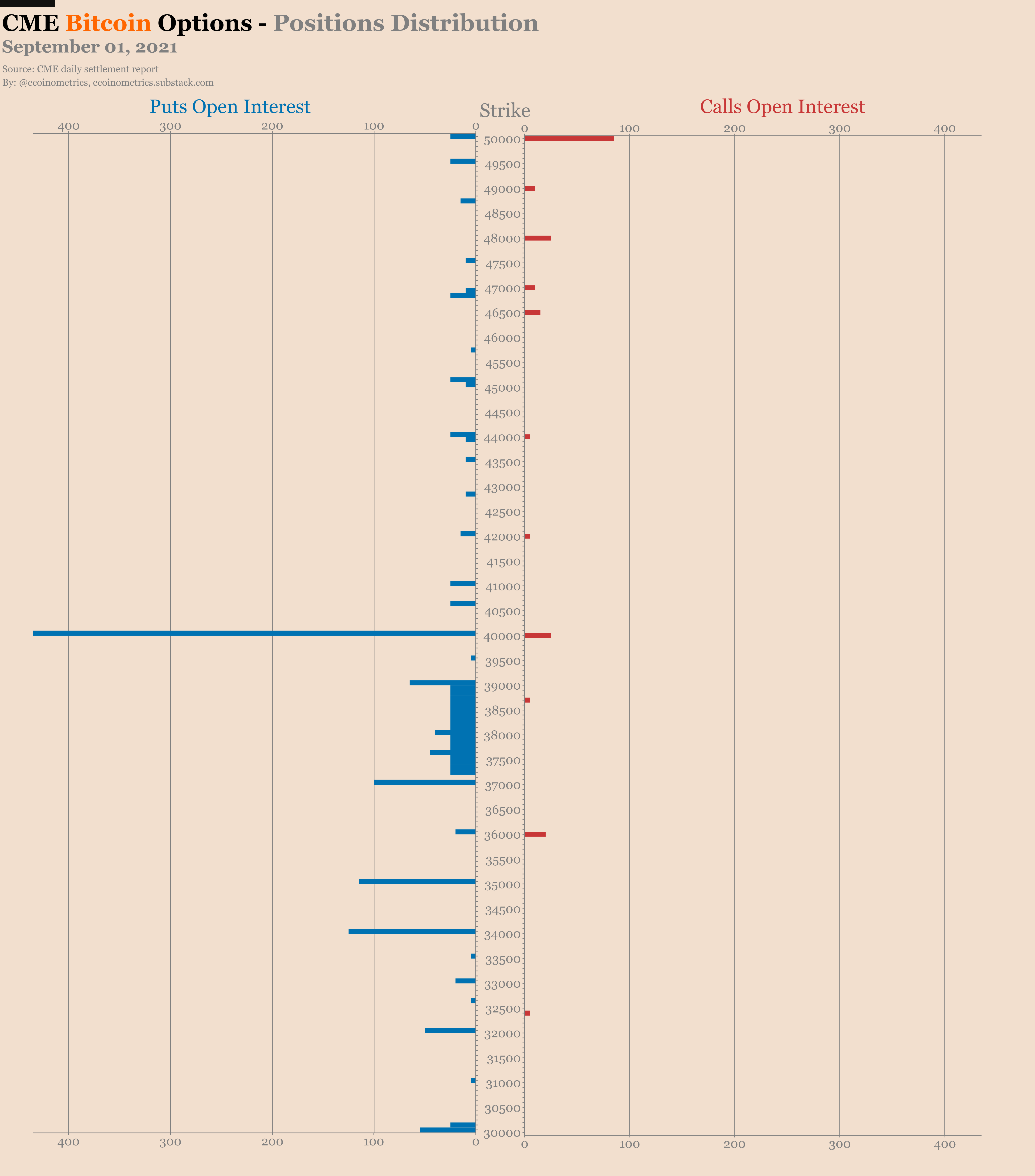

CME Bitcoin Derivatives

Last week was the expiration of the August contracts on the CME. No surprise, after a rise in trading activity just before Friday we are again back to a pretty low volume of transactions.

There was some activity on the options side with mostly traders buying puts. Looks like people are not yet convinced that Bitcoin has started a new leg up. So we are back at 2 puts for every call.

By the way the open interest on the options market is in a steady state. Not growing for sure but not shrinking either.

It looked like it was going to be huge last year when the contracts were launched on the CME. But this is a small market after all.

Maybe once we get a Bitcoin ETF in the US those options will find some more use.

Until then it seems that the retail crowd is buying the trend while the smart money isn’t doing anything new.

Let’s see how that plays out.

That’s it for today. If you have learned something please subscribe and share to help the newsletter grow.

Cheers,

Nick