Ecoinometrics - Portfolio Composition

August 18, 2021

Adding some amount of Bitcoin to a portfolio of traditional assets is working. Not only do you get larger returns, you also get better risk adjusted returns.

Why, though? Turns out it’s pretty simple. Let’s have a look.

The Ecoinometrics newsletter decrypts Bitcoin’s place in the global financial system. If you want to get an edge in understanding the future of finance you only have to do one thing, click on the subscribe button right below:

Done? Thanks! That’s great! Now let’s dive in.

Portfolio Composition

Last week we saw that allocating a fraction of the traditional 60/40 portfolio (60% stocks and 40% bonds) to Bitcoin was a good move.

Historically any amount of Bitcoin inside a monthly rebalanced portfolio would have boosted its total return.

More, it would have done so by improving the risk adjusted returns:

Allocating 5% of a 60/40 portfolio to Bitcoin doubled your risk adjusted returns!

Switching to a 60% stock, 40% Bitcoin composition would double them again!!

Of course it is nice to know that now. But unless you have a time travel machine this analysis is of limited use.

You know what they say, past performance is not indicative of future results.

Still, if we understand why it worked so well in the past we might be able to make some educated guesses about whether or not it will continue working in the future.

Thankfully, understanding why it worked in the past is very straightforward.

You see, the recipe to make a good portfolio is pretty simple:

Pick assets that are trending up over time. That takes care of the returns part.

Pick assets that are uncorrelated to each other. That takes care of the risk adjusted part.

Simple right?

Yep, simple but not easy.

It is definitely not easy to know in advance that something will go up. And it is definitely not easy to forecast if two things are going to be correlated in the future.

But at least we know what we are looking for.

So what about correlations? For this analysis we are talking about portfolios with a specific structure:

You decide in advance on a fixed composition, e.g. 5% BTC with 37.5% BND (bonds ETF) and 57.5% VOO (US stocks ETF).

You rebalance the portfolio to the same composition on a monthly basis.

In that context the only thing that matters is the correlation between the monthly returns of the assets in your portfolio.

Quick reminder, the correlation score measures if two assets tend to move together. A score close to +1 means they tend to move up or down at the same time. A score close to -1 means they tend to move in opposite directions at the same time. A score of 0 means that they move independently of each other.

Turns out, over the last 10 years stocks, bonds and Bitcoin have been uncorrelated:

BTC vs BND correlation score -0.025 (pretty much 0).

BTC vs VOO correlation score 0.157 (pretty small).

VOO vs BND correlation score -0.106 (pretty small).

See for yourself.

So naturally, adding Bitcoin to a 60/40 portfolio does not increase its risk profile. Which means that you can use Bitcoin’s growth to boost your returns for free.

Because of course you need each individual asset in your mix to be trending up. Stacking uncorrelated assets that are not growing will bring you nowhere.

Obviously Bitcoin is up over the last 10 years and so is the stock market. Check it out.

So I hope it is pretty clear now why 5% in Bitcoin performs better than a traditional 60/40 and why switching to a full 60% stock / 40% Bitcoin performs even better. It is all about uncorrelated growth.

Now:

Do you believe that Bitcoin, stocks and bonds will stay uncorrelated in the future?

Do you believe that Bitcoin, stocks and bonds will continue to grow in the future?

Those are the questions you need to answer in order to decide if the same strategy will continue to perform well in the coming years.

My position is that:

Bitcoin will continue to climb driven by adoption.

The Fed will continue to drive the stock market higher.

The actions of central banks will continue to distort the bonds market.

As a result a mix of at least Bitcoin and stocks should continue performing very well.

Time will tell.

CME Bitcoin Derivatives

Well, well, well, what do we have here? Is it just me or does it look like we are slowly getting back on track?

What did characterize the post-halving bull market when it comes to the CME Bitcoin derivatives?

First hedge funds positioned themselves net short on the futures market.

This might seem counterintuitive at first. Why would the smart money go short Bitcoin during a bull market? And actually double dip on that when the price is clearly going parabolic!

There is a simple explanation: they were playing the basis trade. They were actually buying spot BTC and selling the futures against it while pocketing the premium that the derivatives offered over spot.

The more bullish the market was on Bitcoin, the larger the futures premium and the more profitable this trade was.

So actually hedge funds turning again more net short on the futures could be a sign that we are starting a second phase in the bull market.

Second, asset managers (which are typically less aggressive in their positioning than hedge funds) are once more getting net long BTC. For sure the amount of positions isn’t massive, especially when compared to retail traders. But hey, that’s telling us something about the mood.

Then there is the retail crowd. For sure, those guys aren’t big on short positions. So what really matters is how long they are in aggregate. I don’t know, see for yourself, but it is possible they are slowly starting to consider hoping back on the momentum train.

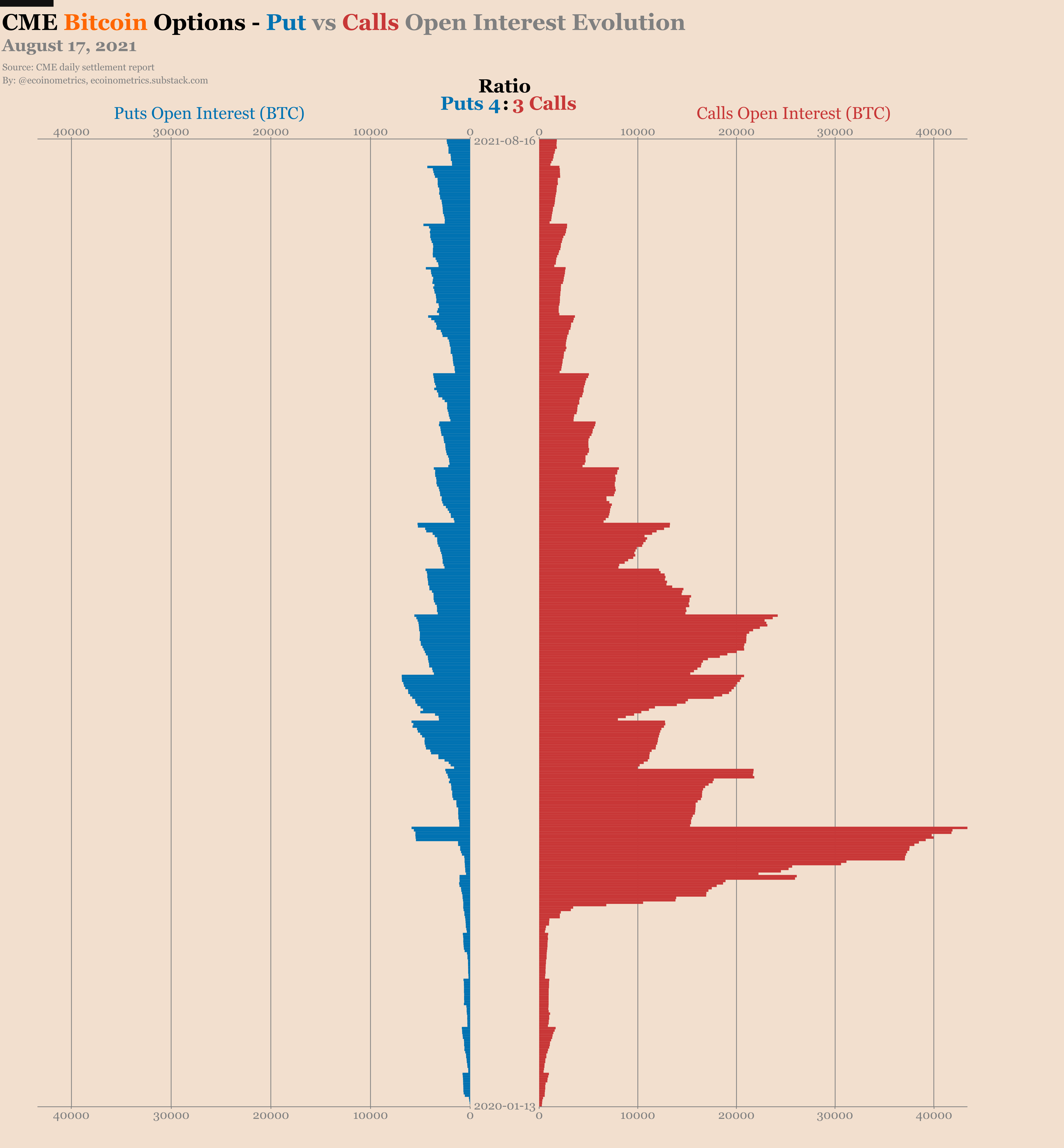

And what about the options market? I mean there is barely anything going on in there. The trading volume is extremely low and the open interest has declined dramatically when compared to where it was last year at the same time.

Still, there too the balance is slowly turning back to neutral. For the past four months the puts significantly outweighed the calls. But now we are back to 4 puts for every 3 calls. That’s much more sensible given the recent price action.

As I write these lines Bitcoin is around $45k, most of the puts are below the $40k strike and most of the calls are above the $50k strike.

So there is no crystal ball here, the market hasn’t made up its mind for where we are going in the short term.

That’s it for today. If you have learned something please subscribe and share to help the newsletter grow.

Cheers,

Nick