Everyone knows that Bitcoin is basically uncorrelated to the stock market, the US Treasury market, gold and commodities in general.

But one thing it is strongly correlated to is, well, the other digital assets…

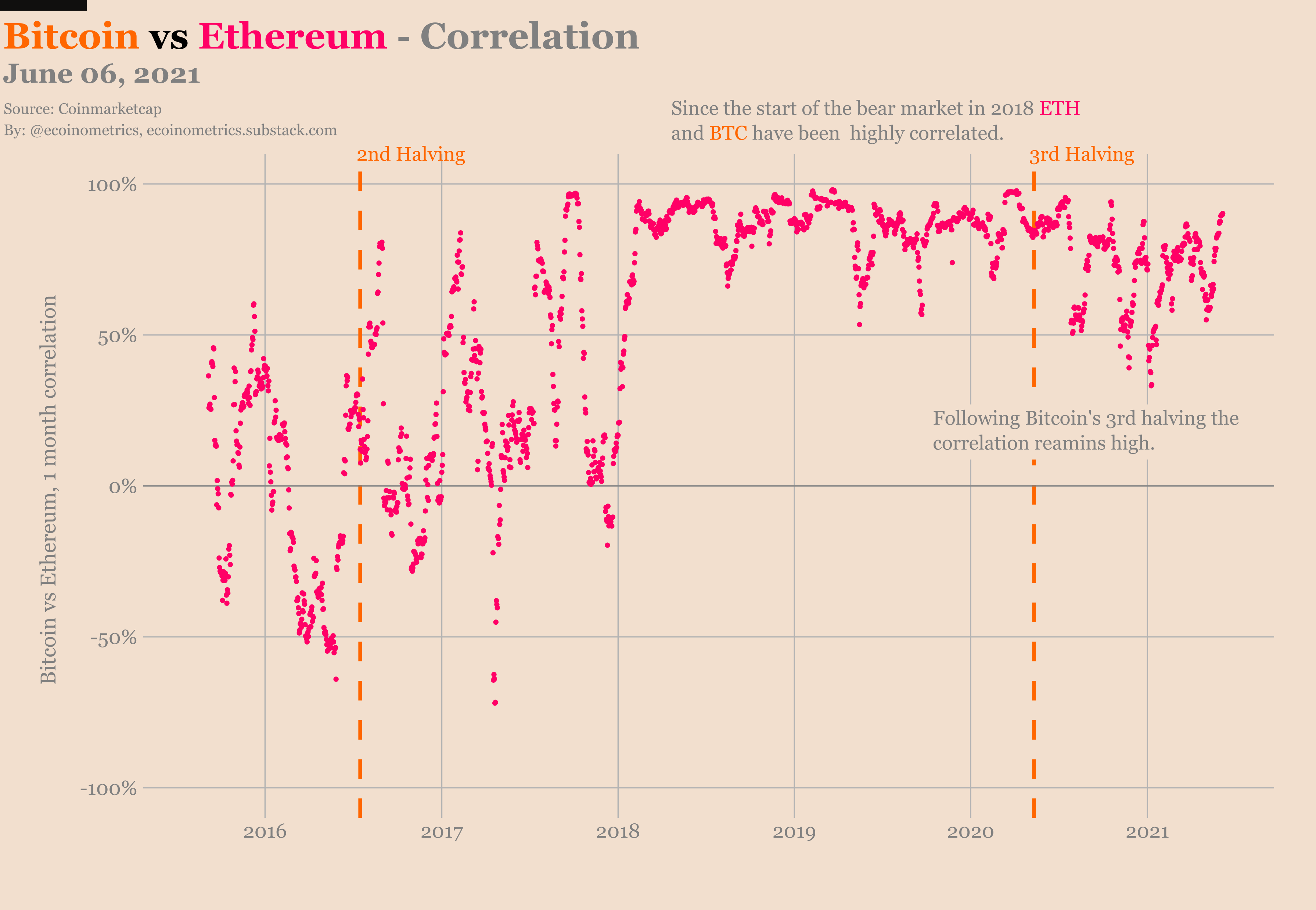

Yes, you guessed it, today is our monthly update on one of the big questions in crypto: will Ethereum decouple from Bitcoin?

The Ecoinometrics newsletter decrypts Bitcoin’s place in the global financial system. If you want to get an edge in understanding the future of finance you only have to do two things:

Click on the subscribe button right below.

Done? That’s great! Now let’s dive in.

The decoupling

As of now, the answer is that it hasn’t. And really there are no signs that this will happen anytime soon.

Since the correction, Bitcoin and Ethereum have been trading just below the growth trajectory of the 2017 bull market.

It is always hard to predict what is going to happen in the short term. But if your investment horizon is counted in months or years then paying attention to the long term trends can help you to form an accurate picture of where we are going.

With that in mind, despite the 50% drawdown in both BTC and ETH it is good to remember that since the 3rd Bitcoin halving:

BTC is up 4.2x

ETH is up 14.6x

The uptrend that started more than a year ago could very well resume anytime. Regardless of the short term price action it is unlikely to be the end of the road.

But back to our main topic. Clearly when Bitcoin is crashing so is Ethereum. There is no decoupling going on here. The timing and the magnitude of the corrections are very similar.

That is to say, BTC is leading ETH in the selloffs.

When Bitcoin is going south, nobody holding ETH sits there thinking “this is none of my business, DeFi and NFTs are doing fine, there is no reason for ETH to drop”.

Nope. Elon Musk dissing Bitcoin, China cracking down on mining, or institutional investors deciding it is time to take money off the table on their Bitcoin bet, none of that matters directly for ETH.

Yet, Ethereum cannot escape its link with Bitcoin.

This is even more clear when you look at the rolling one month correlation between ETH and BTC. Since last year we’ve barely spent any time below a 50% correlation score. Now that we are in a large drawdown the correlation is even back to 90%.

To be fair, that doesn’t mean ETH is not performing well. As we have seen it is up almost 15x in a year.

But Bitcoin is in the driver’s seat when it comes to the long term trend.

So at the moment there is no reason to think we are going towards a decoupling. My base case is that over the duration of this cycle ETH and BTC will be back at an equilibrium exchange rate not very far from where we started.

But I could be wrong. If the DeFi ecosystem really takes off on Ethereum (in a more sustainable way than the ICOs of 2017) then this time could be different.

The jury is still out.

We’ll check back next month to see if there is anything new on that front.

The state wants you to hodl

At first sight, China’s stance on Bitcoin is not entirely clear. Simultaneously:

The state is signalling that it will crackdown on miners.

The state media says it is ok for people to own Bitcoin (as in it isn’t illegal).

But they discourage people from using it as a speculative tool.

And domestic financial institutions have been ordered (for a while now) to fight on-ramp to crypto anyway.

Hmmm… so let me summarize. The Chinese government doesn’t want you to trade but you can own it. In other words, the authorities want you to hodl!

Jokes aside, China is trying to do some balancing act.

On one hand they have two main concerns: limit capital outflow and prevent financial bubbles.

Bitcoin is permissionless and operates without borders. So it creates a new venue for Chinese citizens to get their wealth out of the country. Obviously authorities don’t want that.

What they don’t want either is another debt fuelled bubble in the financial sector. And they see FOMO for Bitcoin as a risk on that side.

So to deal with that they make sure on-ramp is difficult and give stern official warnings not to touch crypto.

On the other hand if there is anything that can help undermine the US$ as a global reserve currency then of course China wants in.

Bitcoin is way too small to be a threat of that nature. But from a narrative perspective it does help raise questions about debt, global reserves and digital currencies.

China is about to launch its digital-yuan and there is no question that in the long term they want to see the sphere of influence of the dollar diminish.

So there it is. China is playing a complicated game and even if Bitcoin is not their preferred solution it can help them to achieve strategic goals at the international level.

Accounting for institutions

Institutions have entered the Bitcoin market. This is a fact. Not all of them. Probably not even the majority of them. But enough that thinking about their impact on Bitcoin is important.

This is a vast topic. Today I just want to start thinking about it. We’ll come back to that regularly with some appropriate metrics in the future.

So here is what I think.

Most institutional investors won’t be long term hodlers.

Why am I saying that? Here is a famous quote from Charlie Munger:

Show me the incentives and I’ll show you the outcome.

Right now, there are very few incentives for fund managers to hold on to Bitcoin forever.

You have to remember that most hedge funds don’t work on the Venture Capital model. They can’t afford to wait for years to see their bets materialize.

Their performance is measured on a monthly, quarterly and yearly basis. That’s about it.

So the calendar matters. If they need to sell today to make sure they’ll post good quarterly results then they will do so.

After all, they are here to make profits for their investors.

That means institutions will be long or short depending on the direction of the wind. And that isn’t going to dampen volatility or save Bitcoin from large corrections.

Now I don’t mean to say that institutional investors are bad for Bitcoin. I’m just saying they are at least neutral and probably a net positive if you consider second order effects.

Indeed more diverse participants in the market is a good thing. The more widespread Bitcoin becomes, the more likely it is going to endure.

And if most institutions won’t hodl, some will. And since there is only a finite amount of coins to go around that’s a net benefit in the long run.

Down the road Bitcoin will grow much larger and be more stable than it is now. When that happens it could very well transition to become a pristine collateral for institutions and that will also drive demand.

But I don’t think we are in that phase yet.

So here are a few questions we’ll need to answer:

Can we spot calendar effects on the price of Bitcoin (end of month, end of quarter, around derivatives events)?

Can we quantify the effects of the momentum strategies used by hedge funds?

Are there any on-chain patterns that we can tie to institutional positions?

We’ll cover that in future editions of the newsletter. So don’t forget to subscribe to get those answers directly in your inbox.

That’s it for today. If you have learned something please subscribe and share to help the newsletter grow.

Cheers,

Nick

Question: other than monthly cycles, why is ETH gradually de-correlating from BTC since 2018? Would it be that the "proof-of-stake" switch makes ETH look less appealing, or similar than BTC?