Ecoinometrics - Transitory inflation ™

July 19, 2021

Another month of post-pandemic recovery and another month of high inflation print.

At this point it looks like transitory inflation is going to be there for a while.

But transitory or not, does it really matter?

The Ecoinometrics newsletter decrypts Bitcoin’s place in the global financial system. If you want to get an edge in understanding the future of finance you only have to do one thing, click on the subscribe button right below:

Done? Thanks! That’s great! Now let’s dive in.

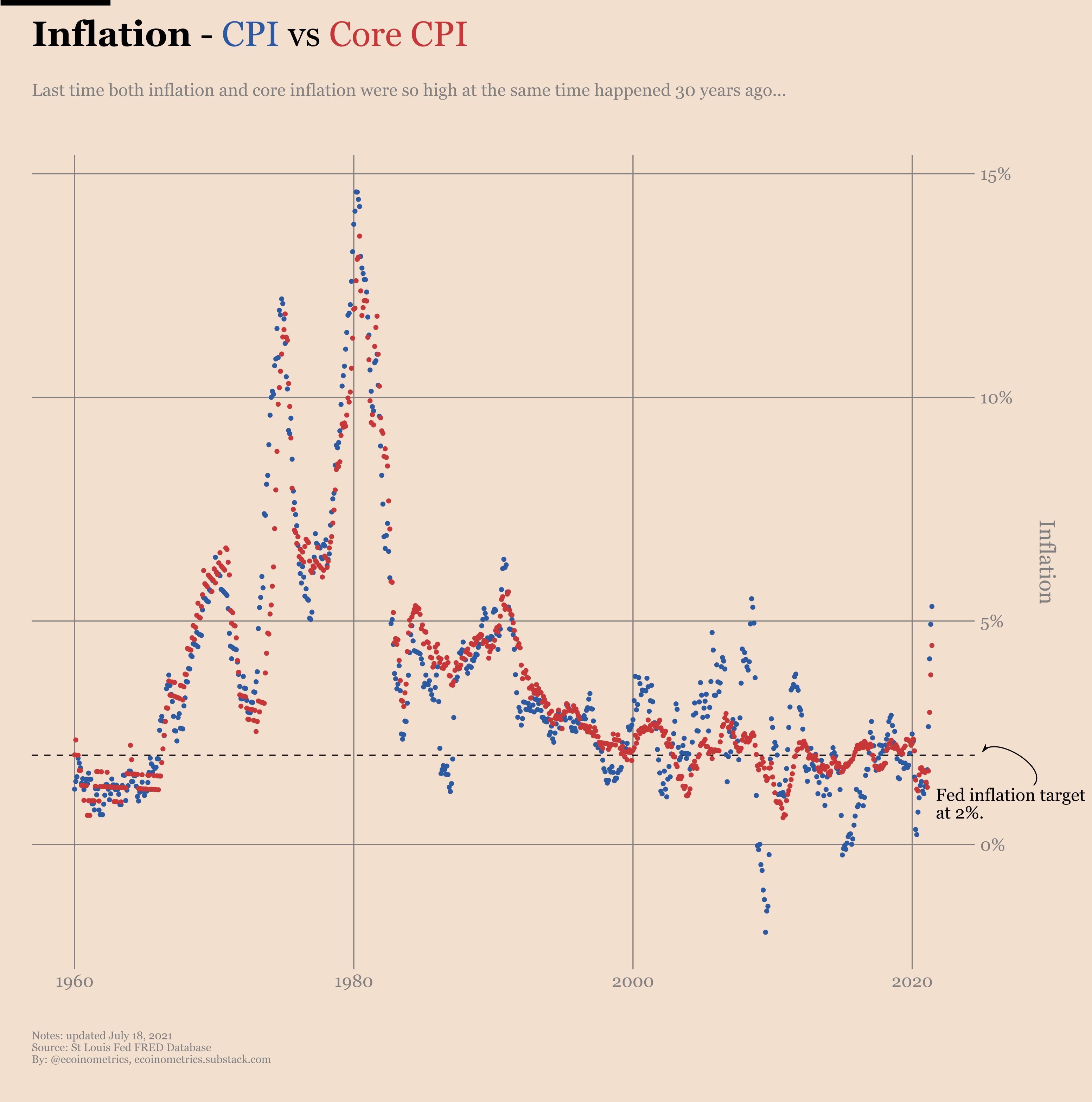

Transitory inflation ™

The US Federal Reserve used to have a goal: an average inflation rate of 2%.

Well, the most recent CPI data puts us there:

Core inflation for June 4.5%

Headline inflation for June 5.4%

Last time both headline and core inflation were that high was 30 years ago. And back then the average inflation rate used to be much higher than it is now.

So I’d say that’s a big deal.

As a reminder, core inflation is calculated using the CPI minus some of the most volatile components such as gasoline.

Core inflation is supposed to give you a smoother picture of what’s going on with prices.

So when both headline and core inflation are going parabolic together, you know that there is an issue…

Now, inflation has been running hot for the past few months, so naturally it is starting to have a significant effect on the average inflation rate that the Fed cares about.

For those keeping score at home:

The 2-year core inflation is above 2%.

The 4-year core inflation is above 2%.

The 8-year core inflation is just below 2%.

The 4 -year headline inflation is above 2%.

Sure, the Fed can always decide to move the goalpost, say conditions are uncertain or choose to focus more on the job market. But when you just focus on the data, things aren’t looking good.

Check it out.

Of course the big debate is whether or not inflation is transitory. But what do we really mean by that?

Let’s backoff a minute to remember what inflation actually measures.

The US Bureau of Labor Statistics tracks the price of a basket of items at regular time intervals. A weighted average is then assembled from those to form a price index. That’s the CPI and its various sub-categories.

Once you have your price index, the inflation rate is defined to be the year -over-year change of this price index.

So when economists are talking about transitory inflation they don’t mean “prices are rising now but don’t worry they will fall back down later”.

Nope. What they mean is that prices are rising fast now but later they will rise… well… less fast.

That’s not the same thing as saying life will be cheaper!

Indeed to see prices actually decrease you need to get a negative inflation rate. But if you go back to the first chart you can see that since the 1960s, the inflation rate has very rarely been below zero. In particular, core inflation has never been below zero at all.

So chances are, even if inflation were to start coming back down towards 2% over the following months, you’ll still be stuck with higher prices on almost all items.

You don’t believe me?

Well, here is a question for you: the US Bureau of Labor Statistics breaks down the CPI into 12 main categories (housing, food, education and so on). How many of those categories have a price index higher than their pre-pandemic level?

The answer is 9 categories, 9 out of 12.

And when you look in more detail it is worse than that. Actually there is only one group of categories that is still below pre-pandemic levels: apparels…

See for yourself.

Do you really think housing will get cheaper in the months to come? Is the cost of medical care suddenly going to drop as we are moving away from the pandemic? Are services going back to their level of January 2020?

History tells you to not bet on that. Don’t expect prices to ever come back down after the pandemic.

When you zoom out, since 2000, the cost of medical care has doubled, services are 60% more expensive while food and housing cost 50% more.

Even if this inflation spike is transitory there is very little chance that this trend will change.

That being said, it is entirely possible that some prices will come down in the short term.

Even if over the long run almost everything gets more expensive, some categories of items are more volatile than others.

Check out the difference in the growth trajectories between medical care, food, commodities and transportation costs since 2000.

Medical care costs have doubled since 2000 moving pretty much in a straight line.

Food and beverage item prices are up more than 60% and here too the ride up is pretty smooth.

But come to commodities or transportation and you see big swings on the way up.

That makes sense. The cost of crude oil, gasoline and raw materials is strongly tied to dynamics of supply and demand that tend to be cyclical in nature.

Meanwhile food or medical care are further away from physical constraints, more artificially driven and thus tend to not stray far away from the big trend.

If for one reason or another the supply-demand situation was to change for commodities and transportation we could see the inflation rate slow down and the transitory inflation camp cry victory.

That won’t mean life is getting cheaper though…

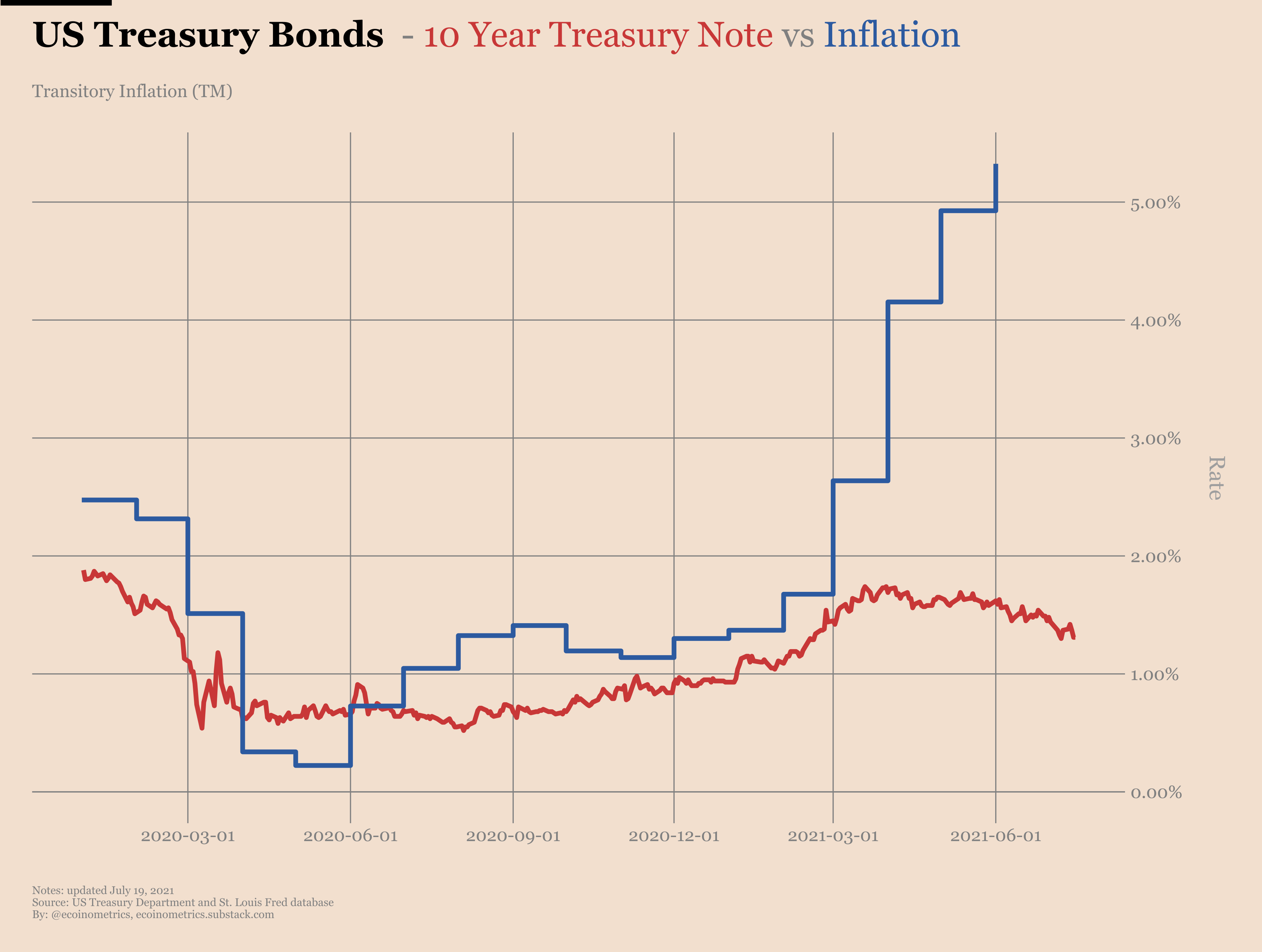

Alright, so that’s for the real economy side of the story. But what do financial markets actually think of this rising inflation?

With an inflation rate above 5% (and climbing) you might have guessed that the bond investors would be shaking their fist in the air, dumping their 10-year notes and demand higher rates.

But nope… look at the divergence between inflation and the 10-year treasury rate...

That means bond holders apparently do not care that the purchasing power of their bonds is melting away with inflation.

This is puzzling.

I can only come up with a few reasons for that:

Maybe they do care. But the Fed owns a big enough chunk of the bonds market that it distorts what would happen in a more “free” market.

Maybe they do care. But they see alternatives as more risky. After all, the stock market is very expensive by many measures. And even though negative real yields are attractive for assets like gold and Bitcoin, if you are worried about a market crash, you might decide to wait before investing in a store of value.

Maybe they actually don’t care. They might be onboard with the Fed reasoning. Inflation is transitory, we’ll be back below 2% in no time.

Honestly I don’t know which scenario is most plausible. But the risk is rising that at some point inflation could become an issue.

If the divergence between inflation and bond rates continues to be high, betting on gold and Bitcoin outperforming seems like a good idea but for different reasons.

For gold it is all about changes in real yield. Historically when the real yield falls to negative territories gold tends to follow with a big rally.

Since the beginning of the year we have moved into very negative real yield territory but we have yet to see a big rally. So a parabolic move could be in the making.

Bitcoin itself tends to be uncorrelated to the real yield. But a negative real yield environment created by high inflation is good for the narrative.

With the price already depressed some investors might decide to bet on Bitcoin rather than gold as a store of value.

If that’s the case then it would be the first time that a Bitcoin rally is triggered by negative real yields. In reality such a move would still qualify as an adoption play since you could see that as a transfer from gold to Bitcoin.

But all this will depend on how the Federal Reserve decides to deal with rates and inflation. So let’s keep an eye on it.

That’s it for today. If you have learned something please subscribe and share to help the newsletter grow.

Cheers,

Nick

P.S. For daily updates follow Ecoinometrics on Twitter.

Always a good read, thanks