Ecoinometrics - Treasuries update

Ecoinometrics - Treasuries update

June 21, 2021

It has been almost a year since people have started to think seriously about Bitcoin as a treasury asset. You have Michael Saylor to thank for that.

So where are we now?

The Ecoinometrics newsletter decrypts Bitcoin’s place in the global financial system. If you want to get an edge in understanding the future of finance you only have to do two things:

Click on the subscribe button right below.

Done? That’s great! Now let’s dive in.

Treasuries update

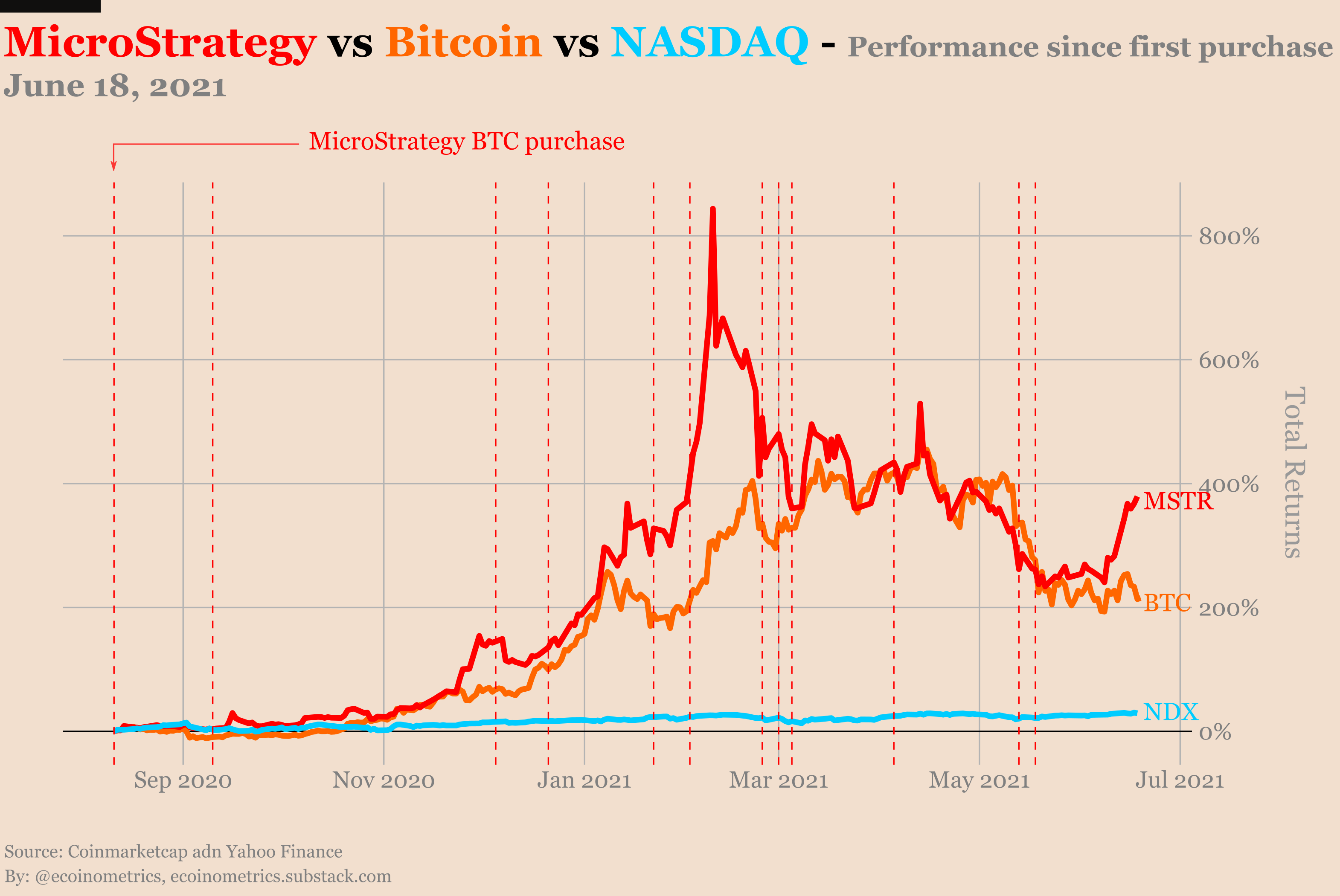

In the summer of 2020, Michael Saylor pivoted MicroStrategy from a business intelligence company to a pseudo-ETF for Bitcoin.

If you look at the performance of the MicroStrategy stock before and after, clearly that was a genius move.

In less than a year MSTR is up 400%. Instead of being more or less driven by what’s going on in the NASDAQ it is now strongly correlated to Bitcoin itself.

While of course that brought a lot of volatility, most of it has been to the upside.

But the stock price is not the only thing that went up. The main part of the bet is the value of their Bitcoin treasury holdings.

Even in the middle of this deep correction they are still up 50%.

To be fair this number could have been much higher if they had just settled for buying a large sum in August 2020.

But instead Michael Saylor is playing the long game with a strategy of dollar cost averaging.

Every time they manage to get their hands on some cash, either as profits from the business or by raising debt, they go and do another buy.

They have done that 12 times since August last year and recently MSTR raised another round of debt to buy even more coins.

Levering up with debt is a risky strategy. But to be fair they are getting pretty good terms since a lot of people are interested in getting some indirect exposure to Bitcoin by buying MSTR instead.

So as long as they can hang on to their treasury until Bitcoin makes its next parabolic rise they are likely to win on both fronts: higher stock price and massive treasury.

That’s for MicroStrategy itself. Michael Saylor didn’t leave it at that. You don’t simply invest in Bitcoin.

Nope, he became an evangelist of the “Bitcoin as a treasury asset” movement. Incidentally, this is good for marketing and for talking up his book.

Now, given how long it takes for your average corporate structure to decide on these kinds of investments, it is way too early to know how many CEOs have heard the message.

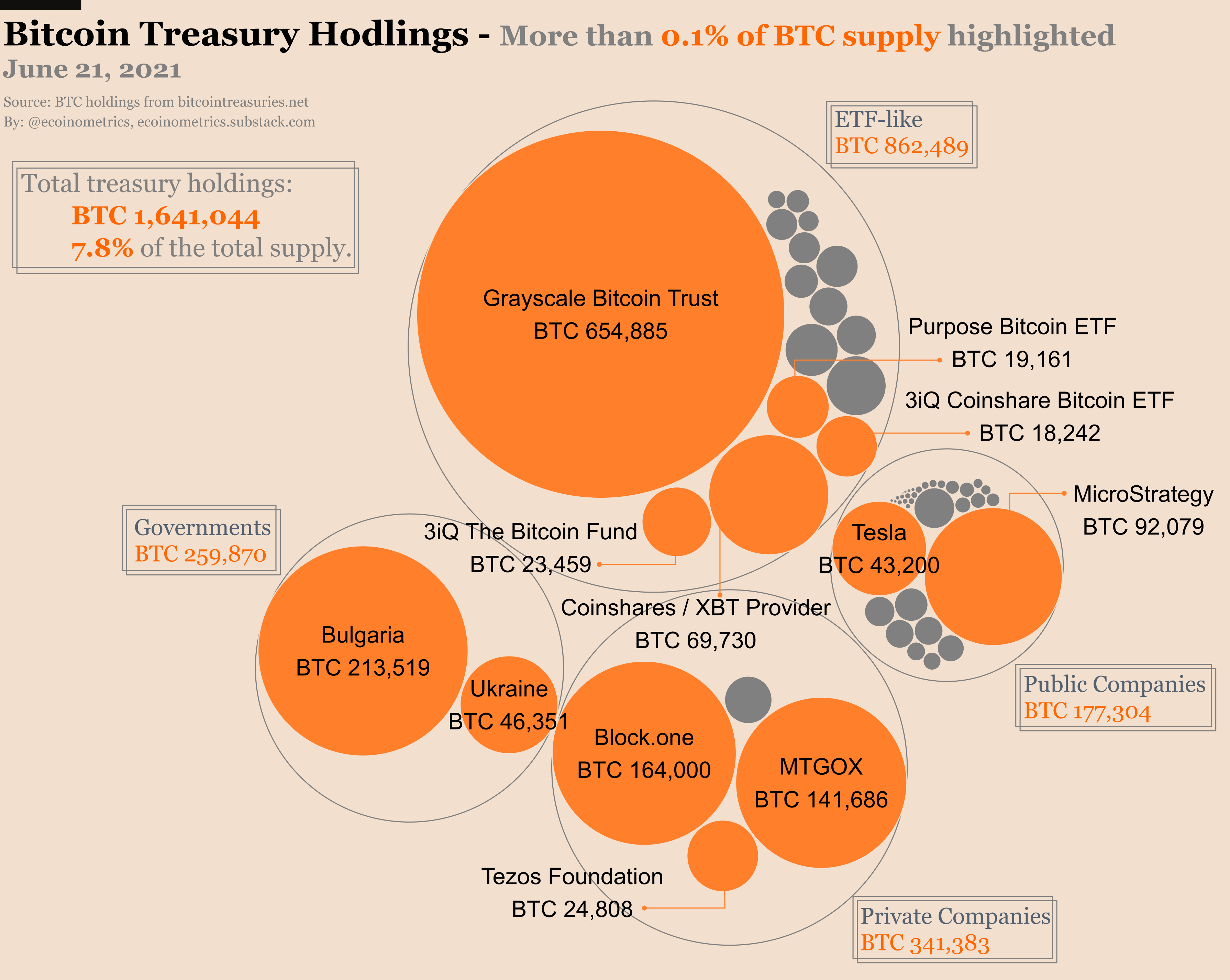

So far, the data collected by BitcoinTreasuries.net shows that:

Among public companies MicroStrategy is still by far the company with the largest investment in Bitcoin.

While Tesla is coming in second, there are still questions around Elon Musk flip-flopping on Bitcoin.

The rest of the public companies who have invested in Bitcoin consists of relatively small stakes.

Check out the chart below. The area of each disk corresponds to the amount of Bitcoin held on some balance sheet.

Clearly public companies do not capture a very big part of the Bitcoin supply. Actually they represent the smallest part of the 7.8% of the Bitcoin supply held on balance sheets.

ETF-like investment vehicles like the Grayscale Bitcoin Trust capture the majority of those coins. And actually if you were to move MSTR (as a pseudo ETF) from the category of public companies to ETF-like instruments things would be even more tilted.

See for yourself.

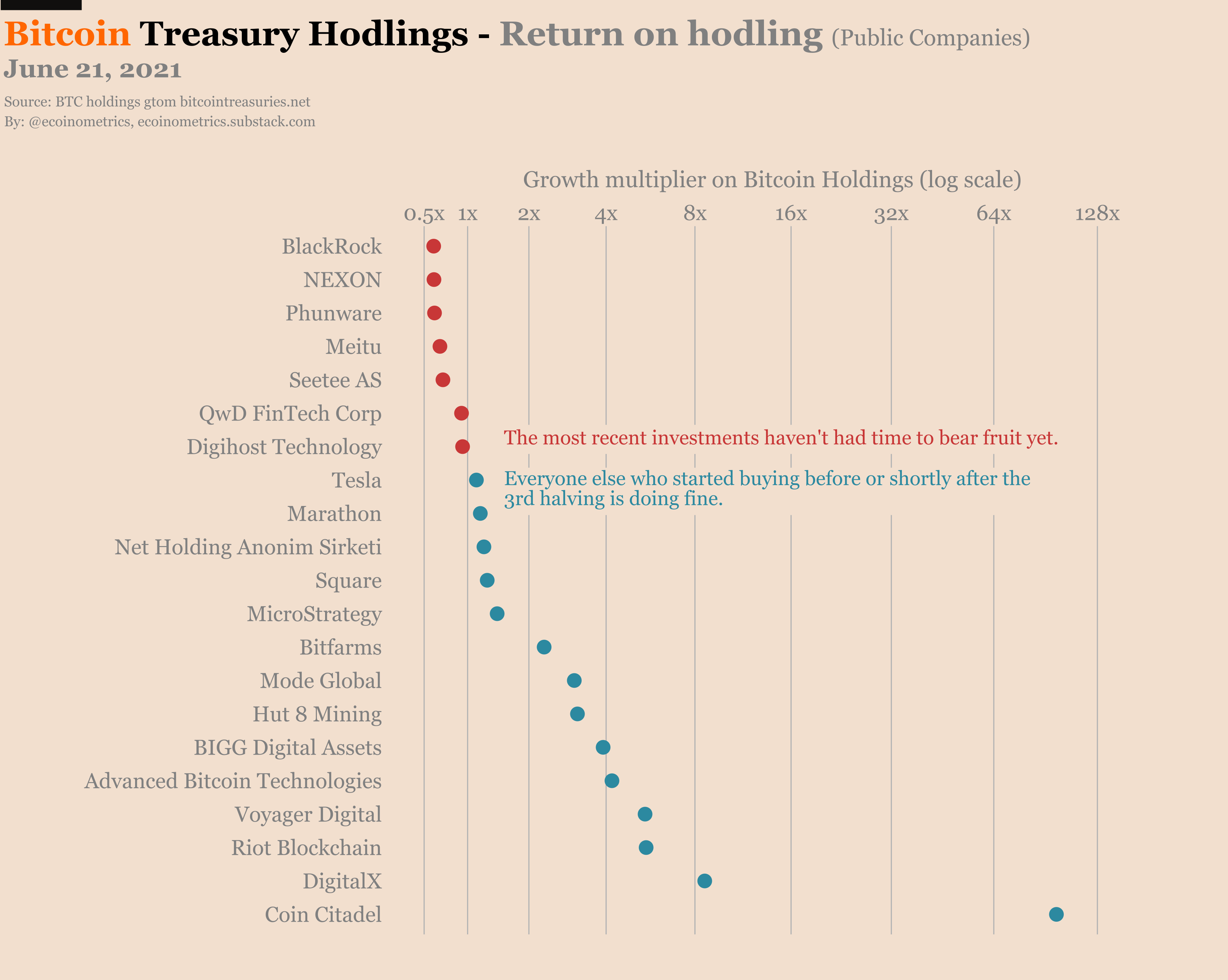

When it comes to public companies for which we have enough data, all but the more recent investments have had a positive return on hodling.

So if you want to see the cup half full then you can say that this is good news:

The approval of a Bitcoin ETF in the US would likely suck a big part of the supply of coins and that’s not priced in.

Moreover we haven’t yet seen the pressure coming from larger companies starting to convert parts of their balance sheet to Bitcoin.

If you want to see the cup half empty you can say that maybe Michael Saylor’s evangelism has been falling on deaf ears. Maybe only smaller companies will buy small stakes. Or maybe only public companies whose CEO exerts enough control to decide by themselves are going to invest in Bitcoin (the Elon Musk or Michael Saylor types).

In the first scenario there are potentially large untapped balance sheets ready to siphon the BTC supply. Clearly that’s bullish.

In the second scenario there are only small marginal buyers left to enter the market. This isn’t bullish but it isn’t bearish either.

Most likely the big money inflow will come from financial institutions getting into the Bitcoin game. And we haven’t seen that yet. There is still more potential upside than downside.

FOMC

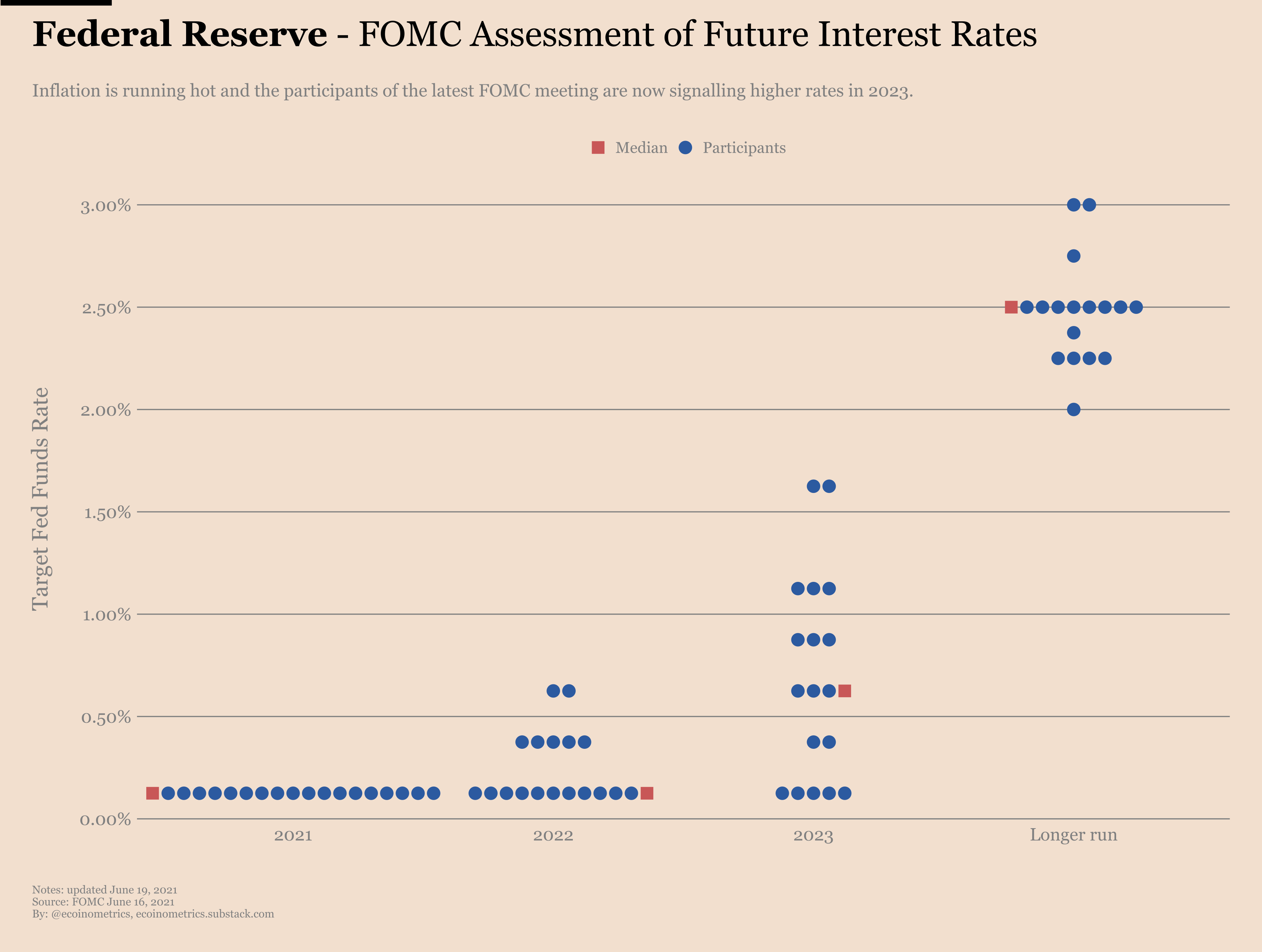

Last week was the Federal Open Market Committee meeting for the US Federal Reserve.

Nothing terribly surprising came out of it.

To remind you of the context, last month inflation spiked again. In particular, the core inflation number (inflation less food and energy) is now at its highest since the 90s.

So naturally everyone was waiting to hear what the Fed had to say about that.

While he did acknowledge that inflation is on the high side, Jay Powell continued to say that he expects this to be transitory.

More likely than not he is right.

At the moment the year-over-year inflation is propped higher by the base effect. But as we are moving away from March the base effect will get smaller and smaller. So unless something goes terribly wrong ,core inflation probably is at its highest point.

That’s not to say we are going back to zero though. Core inflation above 2% at least for the next few months is the most likely scenario.

And that’s kind of what the Fed is saying indirectly when it comes to the projection of future rates.

The participants of the FOMC have voted and it looks like they have decided the US economy will be ready for a rate hike as early as 2023.

I don’t know if they believe in that themselves, but at least this is what they signal.

For the longer run the FOMC is targeting a return of the Fed Funds Rate at 2.5%... I don’t know what they mean by longer run but that number seems totally unrealistic.

The last time the Fed Funds Rate reached 2.5% was in the second half of 2020.

That was before the pandemic. And already before the pandemic they had to start cutting rates again because the market couldn’t tolerate it.

Remember that when people blame the low rates on COVID. Clearly even without external events the US economy has its weaknesses.

Let’s see where this is going.

That’s it for today. If you have learned something please subscribe and share to help the newsletter grow.

Cheers,

Nick