Ecoinometrics - Wen moon?

Ecoinometrics - Wen moon?

November 03, 2021

Wen moon? The eternal question everyone is asking in the cryptocurrencies trading circles. Sorry to disappoint but I don't have the answer.

But I do have something to say about the effect of the moon cycles on Bitcoin’s price action...

The Ecoinometrics newsletter decrypts the place of Bitcoin and digital assets in the global financial system. If you want to get an edge in understanding the future of finance you only have to do one thing, click on the subscribe button right below:

Done? Thanks! That’s great! Now let’s dive in.

Wen moon?

If you have been following this newsletter for a while, you know that short term trades aren’t really my focus. Most of my time is spent looking at long term trends and macro plays.

But from my past life as a quantitative trader I’ve kept a keen interest in looking at statistical anomalies that sometimes give rise to profitable trading strategies.

So when someone asked me the other day what I think about the effect of the moon cycles on the price of Bitcoin I thought “hey, why not, let’s have a look”.

From what a quick google search tells me, there are countless variations of trading strategies that involve buying when the moon is in a certain phase and selling when the configuration changes.

Obviously it is impossible to cover all the possibilities so here we’ll be restricting ourselves to a simple type of strategy.

It goes like that:

Buy at the start of the full moon.

Sell at the end of the full moon.

Well while we are at it we can as easily look at what happens if you buy at the beginning of a moon phase and sell at the end. This way we can see if the full moon really stands out.

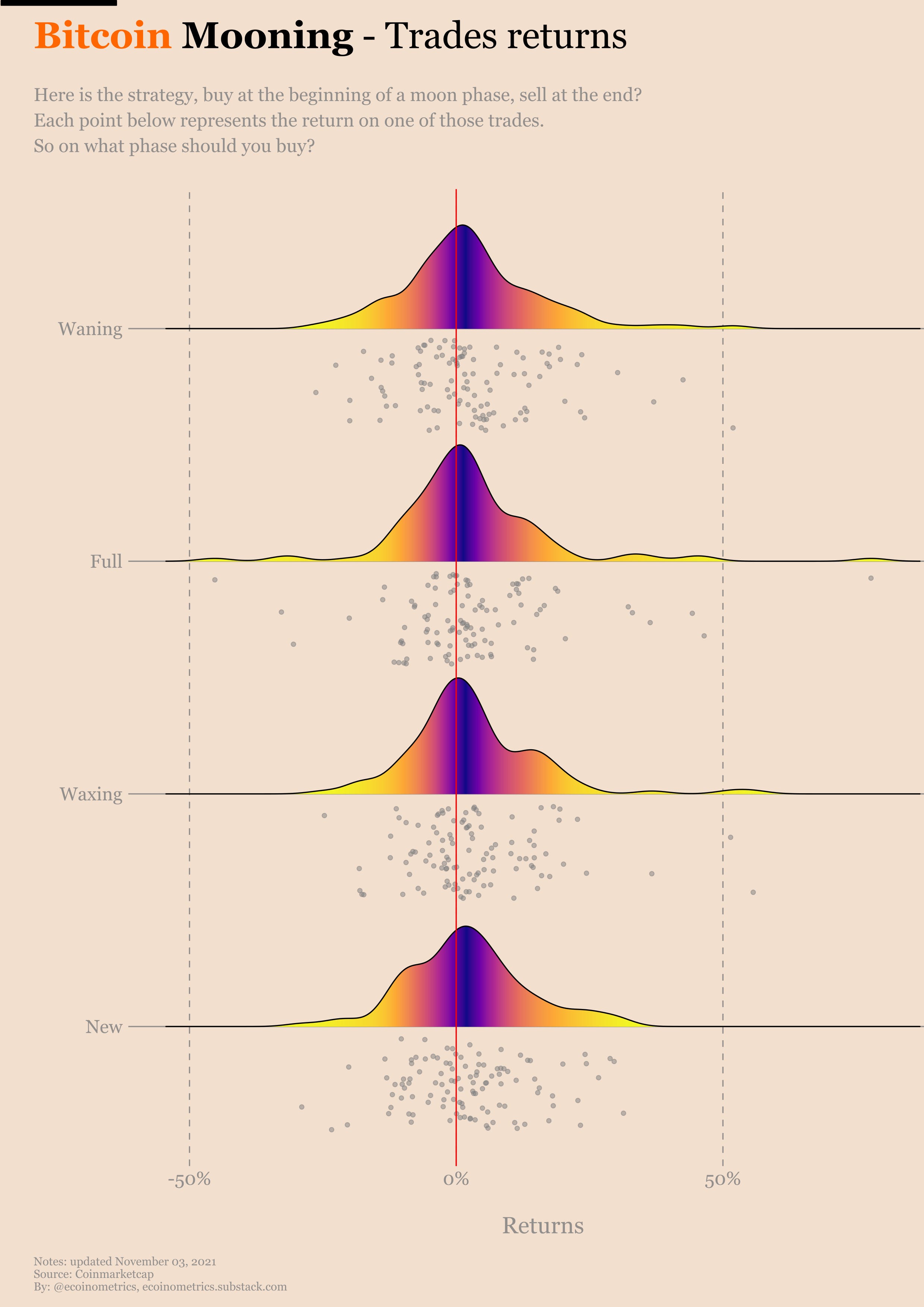

Here are the results. Each point below is a trade that buys BTC at the open (GMT) of a moon phase and close at the end (GMT) of the same phase. The returns are on the horizontal axis. The density gives you an idea of the distribution of those returns with the darker the zone, the closer to the average return.

Check it out.

First observation is that actually regardless of the phase of the moon this trade has a positive expected value:

Waning, average return +2.68%, median return +1.42%

Full, average return +2.67%, median return +1.26%

Waxing, average return +3.1%, median return +1.60%

New, average return +2.24%, median return +1.55%

That’s good… and it also shows that there is actually nothing special about the full moon, at least with this trading setup.

But the popular belief seems to be that the full moon pumps your bags while the new moon is bad.

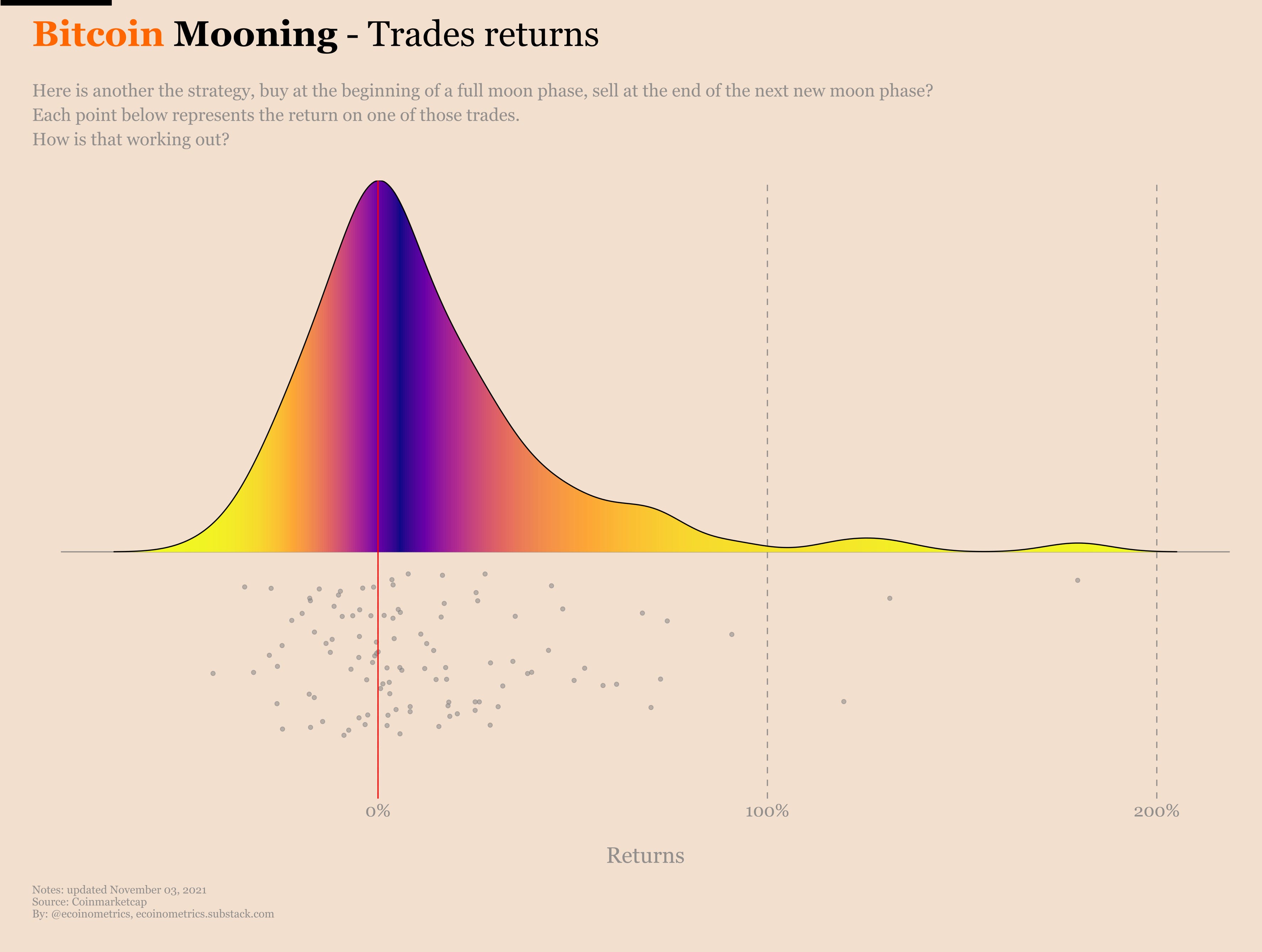

So maybe a better trading strategy is the following:

Buy on the first day of the full moon.

Sell on the last day of the next new moon.

Well here are the results:

Average return +12.1%

Median return +3.85%

Nice! Here is another profitable trading strategy.

But wait a minute. Is the moon really giving us some alpha here? Or is it just that, you know, numbers go up…

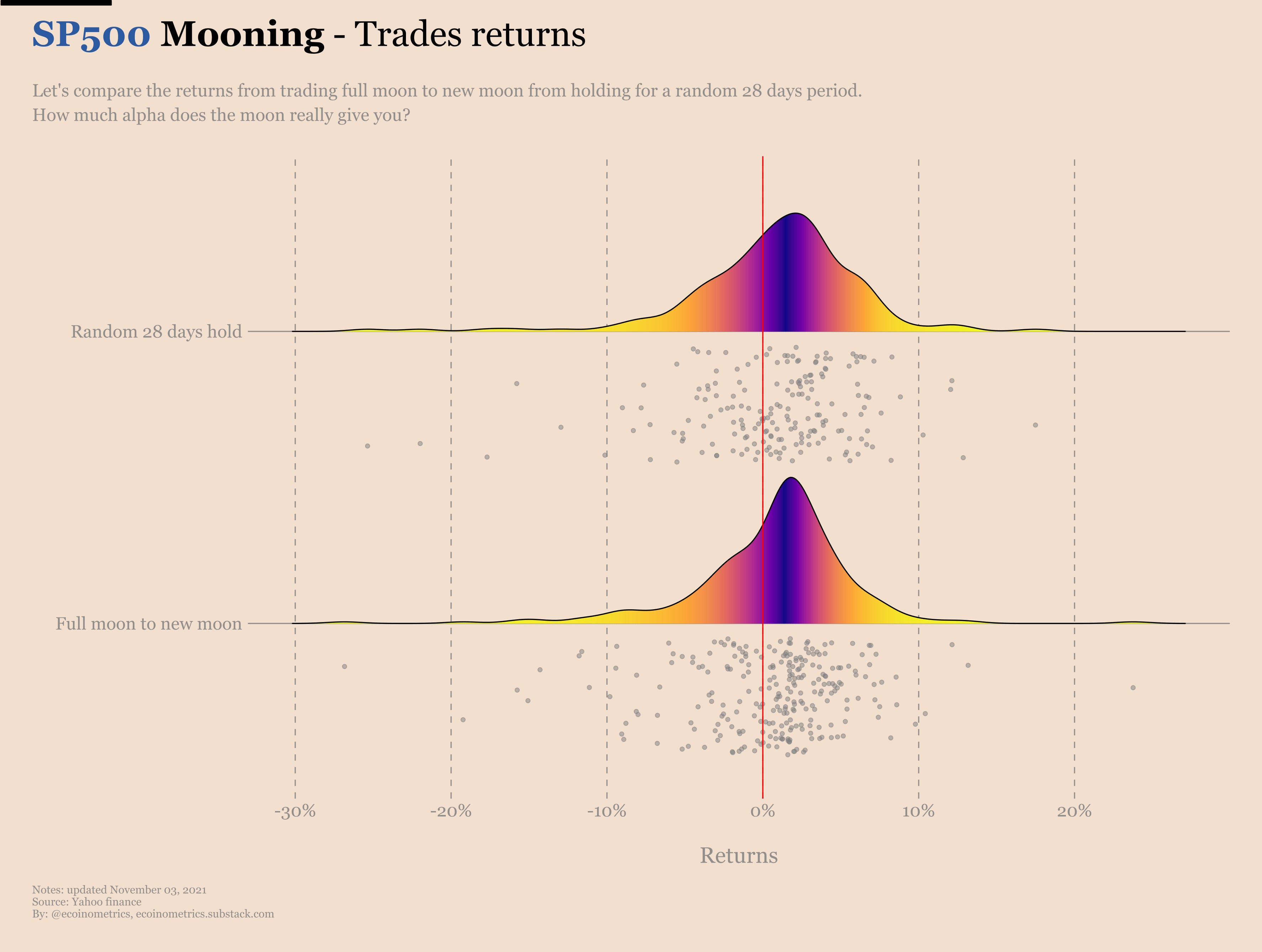

Well to settle that we can compare the trading setup from full moon to new moon to a simple strategy that consists in buying on a random day and waiting 28 days to sell.

See for yourself...

Suddenly the alpha coming from the moon is starting to be less convincing:

Full moon to new moon, average return +12.1%, median return +2.85%

Random 28 days hold, average return +12.9%, median return +5%

We’ve tried a number of ways of selecting random 28 days holding period and this observation seems consistent.

It seems to me that these moon strategies aren’t giving me any particular edge compared to just buying Bitcoin.

By the way, people are claiming the same thing about the stock market. Buying stocks on a full moon is good, new moon not so much.

And surprise, surprise when you apply the same analysis as we did above to the SP500 you find that, again, the moon doesn’t work much better than a random 28 days period:

Full moon to new moon, average return +6.28%, median return +1.54%

Random 28 days hold, average return +8.33%, median return +1.55%

I’m sure there are more complicated setups that people have come up with that work great on backtesting. Usually that just comes down to overfitting the strategy to the past.

My view is that if the simple version of the strategy doesn’t show any significant promise then there is no point in making it more complex. At the end of the day you end up adjusting to the noise and lose track of the signal.

Simple tends to be more future-proof than complex. The simpler the better.

So if you think a simple buy and hold of BTC for a year can 5x your investment I’d say just do that.

CME Bitcoin Derivatives

If you didn’t know that the SEC had approved a Bitcoin futures ETF in the US then you just have to look at what’s happening on the CME to realize that something is different.

There was a big pump in the open interest, even though it came down a little bit after the October contract expired last Friday.

If you look at the data coming out of the Commitment of Traders report you can see a massive spike in the amount of long positions held by retail traders.

However I am not sure of the way the longs are attributed to the ETFs. Unfortunately I did not have the occasion to dig into the data before getting this newsletter out but we’ll report on the details of how it works in the future.

The smart money is taking advantage of the big premium of the futures over spot to make a killing with the carry trade. This is going to last as long as the Bitcoin ETFs continue to see more inflow.

Notably the asset managers (who are less prone to use arbitrage strategies) are now record net long BTC.

Did anyone say bullish?

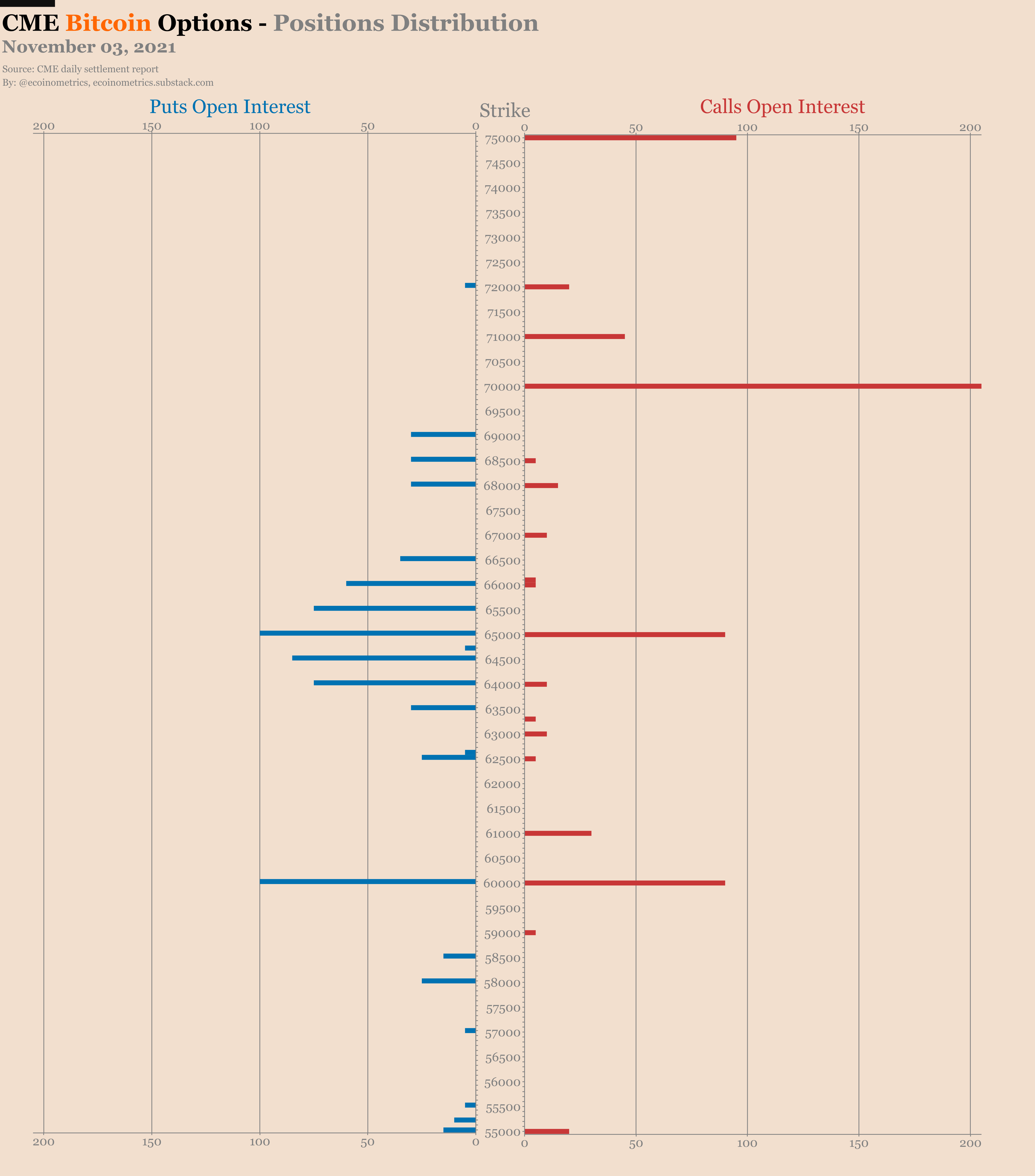

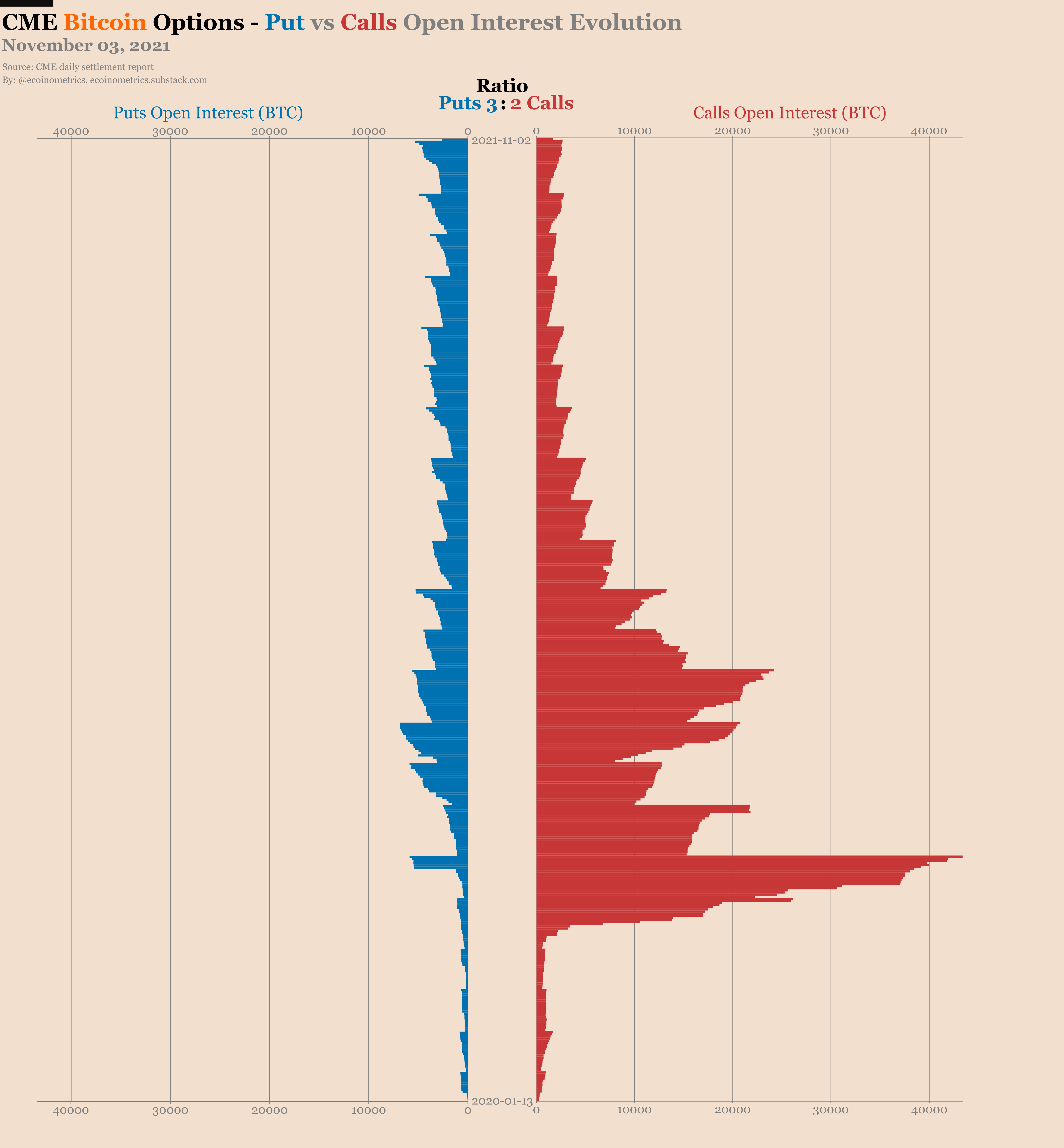

There isn’t much to say about the CME Bitcoin options market. The puts to calls ratio has been remarkably stable at 3 puts for every 2 calls for a long time now.

Most of the puts are concentrated in the $60k to $67k region. While the calls are piled up at round strikes ($60k, $65k, $70k, $75k). That tells you everything you need to know about how people are using those derivatives.

The calls are speculative bets on Bitcoin’s price rising this month. The puts are just there to hedge other positions.

Let’s see how that plays out.

That’s it for today. If you have learned something please subscribe and share to help the newsletter grow.

Cheers,

Nick

Question: in a semantic sense, are crypto asset managers just half-baked indexers with some hedge fund elements (thereby function similarly to bonds in relations to S&P)?