Looking at the Futures - May 28, 2020

Bakkt vs CME

All over the world many crypto exchanges are offering derivatives on Bitcoin: BitMEX, OKEx, Huobi, Binance, FTX…

But when it comes to US regulated products that have the potential to absorb large amounts of institutional money the field is much smaller.

Looking at the Futures is a weekly newsletter where we are making sense of the Bitcoin derivatives market. Emphasis is put on the CME products as they dominate the field for institutional investors. But we’ll occasionally look at other venues too.

Subscribe now and don’t miss anything!

Bakkt vs CME

Actually in the US regulated Bitcoin derivatives market you have two main players: Bakkt and the CME.

It used to be that the CBOE offered cash settled Bitcoin futures but due to low traded volume they got rid of this product last year.

So if you are a fund or an institutional client you have to make a choice between:

Bakkt offering physically settled futures and options on Bitcoin.

CME offering cash settled futures and options on Bitcoin.

Bakkt only started operating in September last year. At the beginning trading activity was pretty strong and open interest climbed fast. But as you can see in the latest Bakkt futures daily activity report, that growth broke down at some point. And since then Bakkt trading is stuck at around 50% of what it was at its peak.

Actually when you compare Bakkt to the CME you can see that Bakkt is taking a very small share of the market. In terms of open interest the CME futures are 50 times larger than Bakkt.

And the trend is getting worst. Open interest is climbing consistently on the cash settled futures. That made Bakkt go from a maximum of 5% market share down to 2% at the end of May.

I’m not even talking about the Bakkt options market which is a ghost town. Less than 10 positions opened every month. No daily trading activity whatsoever. Compared to the thriving CME Bitcoin options market that launched in January it looks very bad.

At some point we need to wonder if the Bakkt derivatives are going to go the way of the CBOE: simply disappear.

That’s possible. But there is a big difference. Both the CBOE and the CME contracts were cash settled. So they were in direct competition. Bakkt is dealing with physical delivery of Bitcoins in the Bakkt warehouse.

The real question is then: what’s the demand for physical delivery of Bitcoin?

If you are a big institutional player you don’t want to handle the cryptographic keys directly. There are way too many regulatory uncertainties with that at the moment. Plus you’d need some people working for you with the technical ability of doing that securely. Given the size of the Bitcoin market there is probably little interest in dealing with that for the big players.

So you are left with two options:

Get exposure through cash settled products.

Outsource the logistics of taking care of your coins, say through Bakkt.

How many people are choosing option 2? We can gauge the appetite for that by looking at how many of the Bakkt contracts are held for physical settlement every month.

Before January that number was pretty low. Since then we consistently see between 100 and 300 Bitcoin futures physically settled in the Bakkt warehouse every month.

And if we look at the ratio of Bitcoin physically settled to the maximum open interest for the month we get a stable range. In the past 8 months an average of 22% of the max open interest in a month is settled physically.

My view is that it means Bakkt is playing its role as an interface between the derivatives and the physical Bitcoin markets. For sure this is only a niche role for now. But as Bitcoin market cap will grow and institutional interest will rise I can see it being a viable market.

That might take some time though, so who knows if Bakkt can survive that long.

Last trading days on the CME

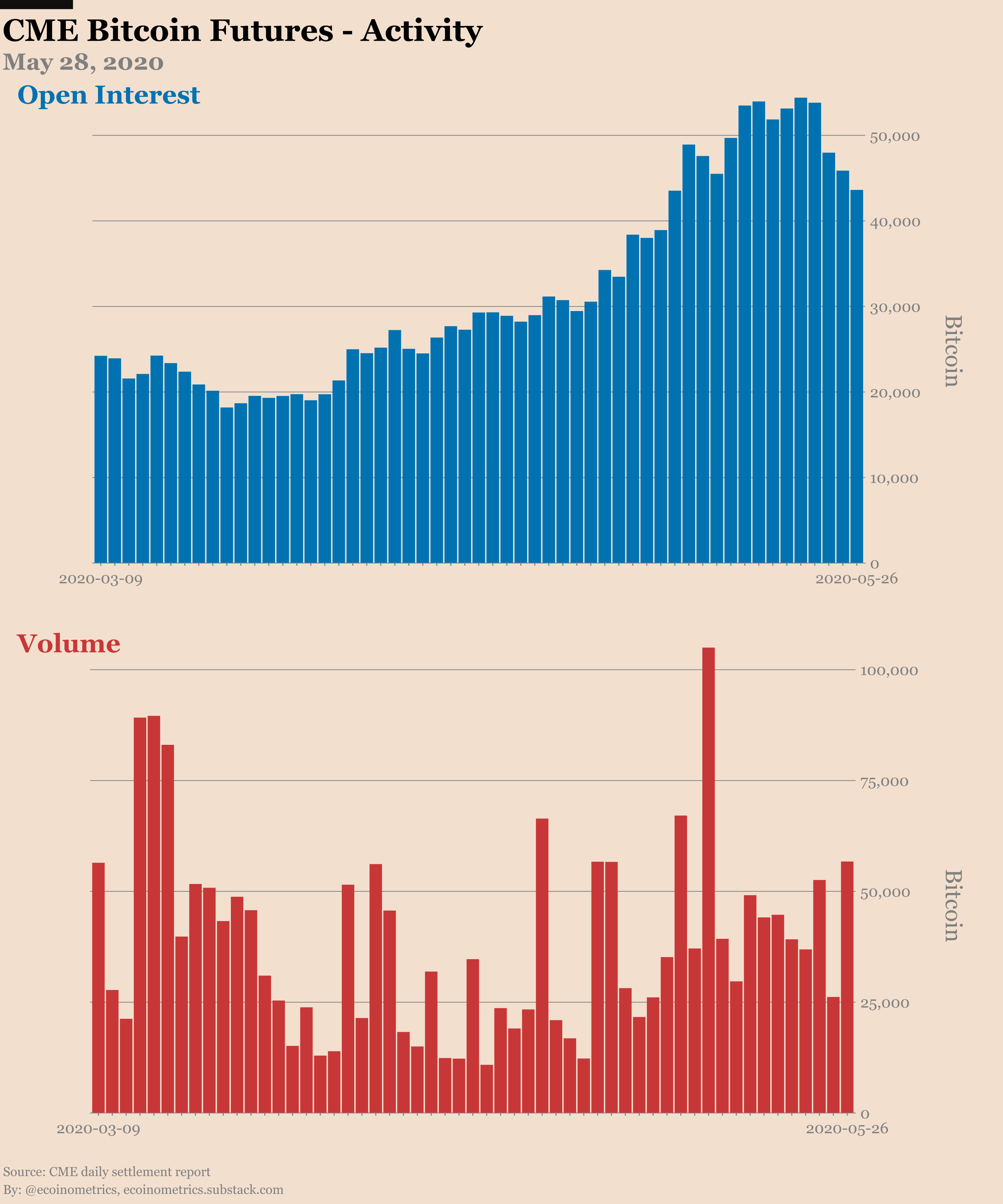

Now let’s go over this week’s activity in the CME markets. The May contract last trading day is coming this Friday. That means it is roll over week.

Open interest has shifted from May’20 to Jun’20 but the total positions count is moving down from its peak.

We can attribute that to the Bitcoin price action. Since the low of March BTC is up 100%. That certainly attracted a lot of new long positions. But the rally stopped at $10k. Now BTC is moving sideway to lower between $8k and $10k.

If you have captured a 100% percent run I won’t blame you for taking some money off the table. Combined that with the traders looking to settle their positions before the Memorial day weekend and you get some decline in open interest. No big deal.

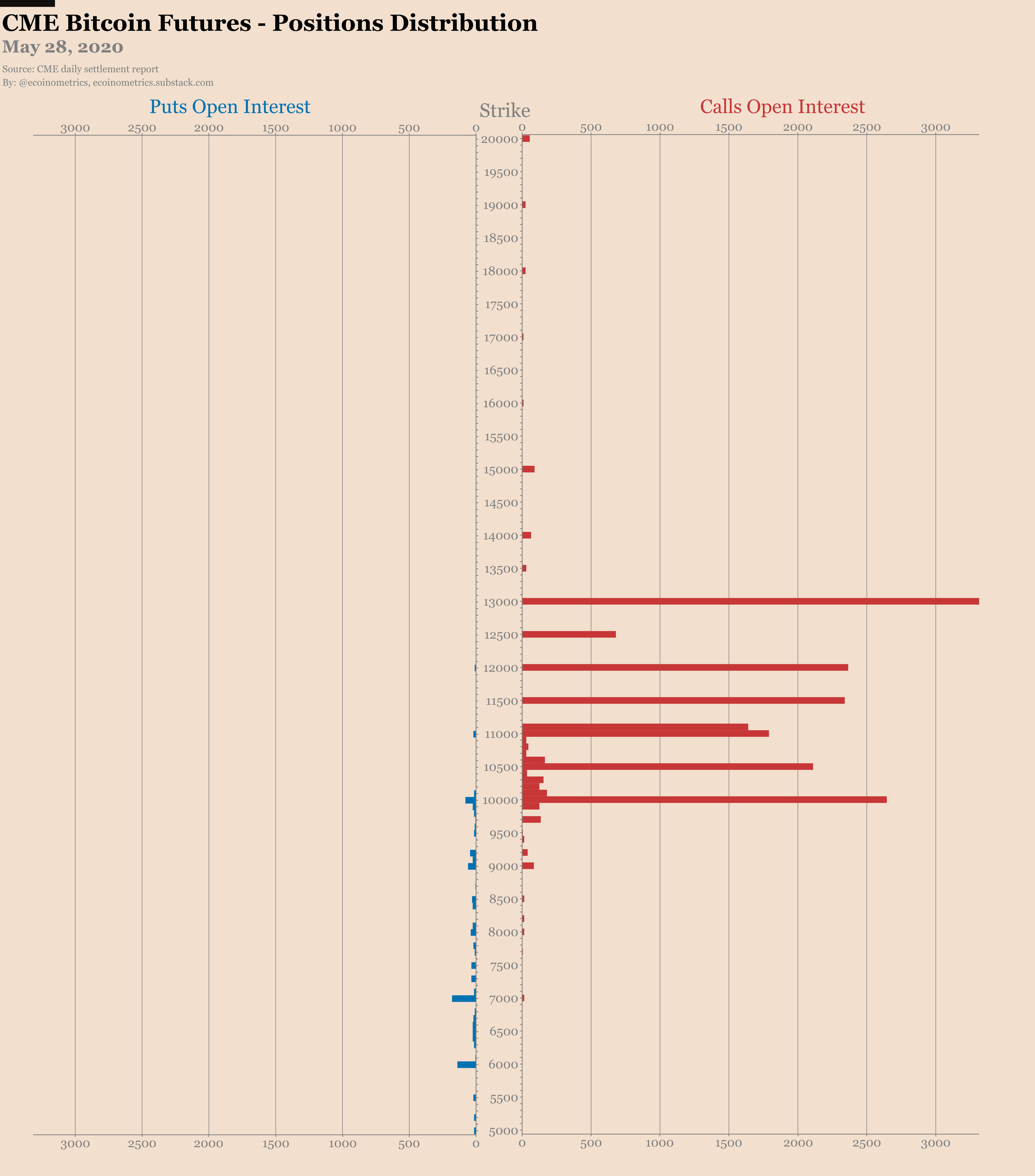

On the options side of things the bulls are probably sweating right now. Two days to go but $10k is so close and yet so far at the same time. To start making some money the bull calls in May are waiting for a 20% pump in Bitcoin. That can happen in one day. So wait and see…

What if those May positions don’t pay off? No worries we have the same ones waiting on the June contract. The put/call ratio is still at a very high 17 calls for every 1 put.

No need to say more, just look at the chart.

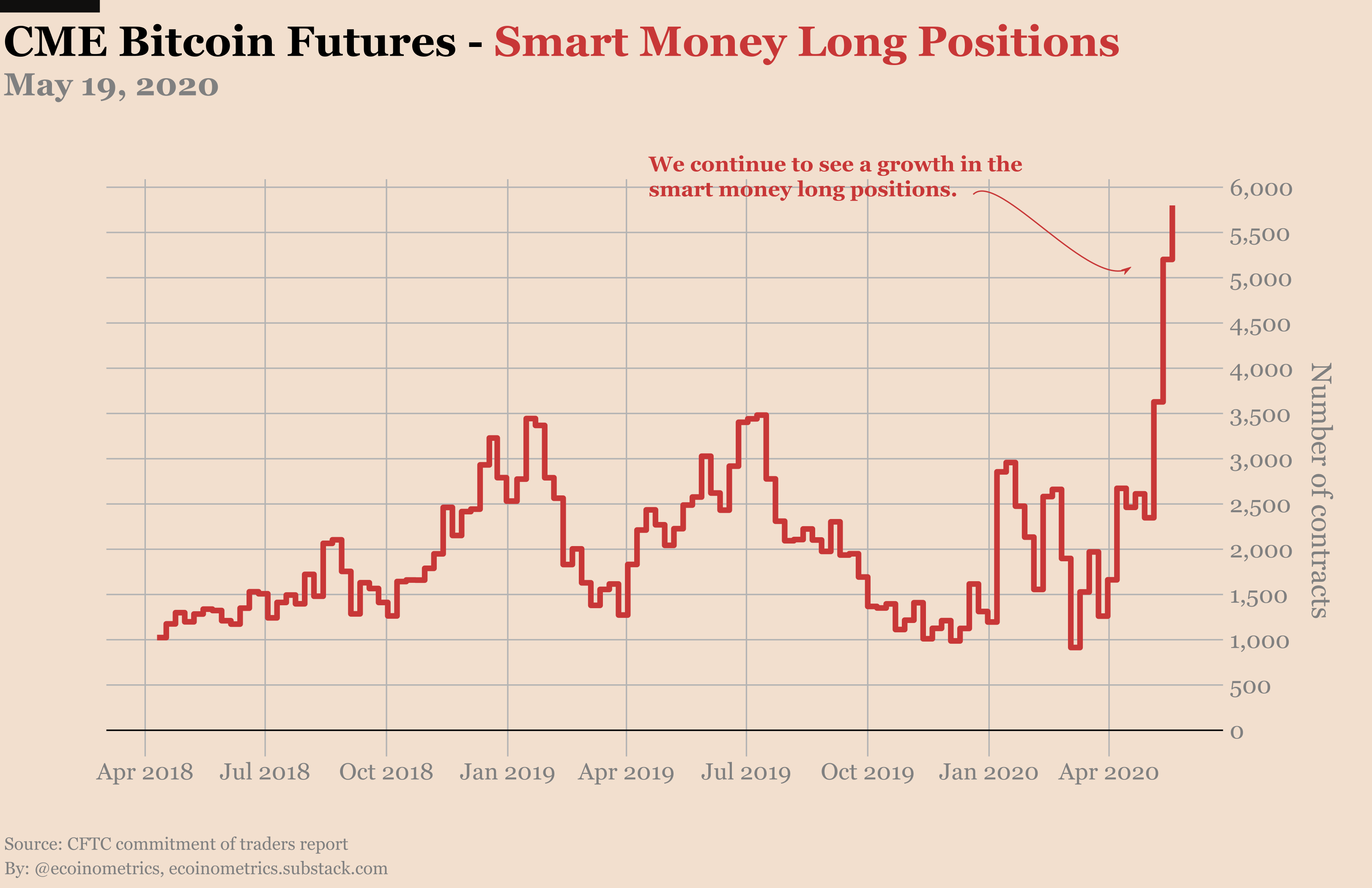

Looking at the CFTC commitment of traders data we can see that the smart money continues to add long positions. But in aggregate those traders remain very much short Bitcoin.

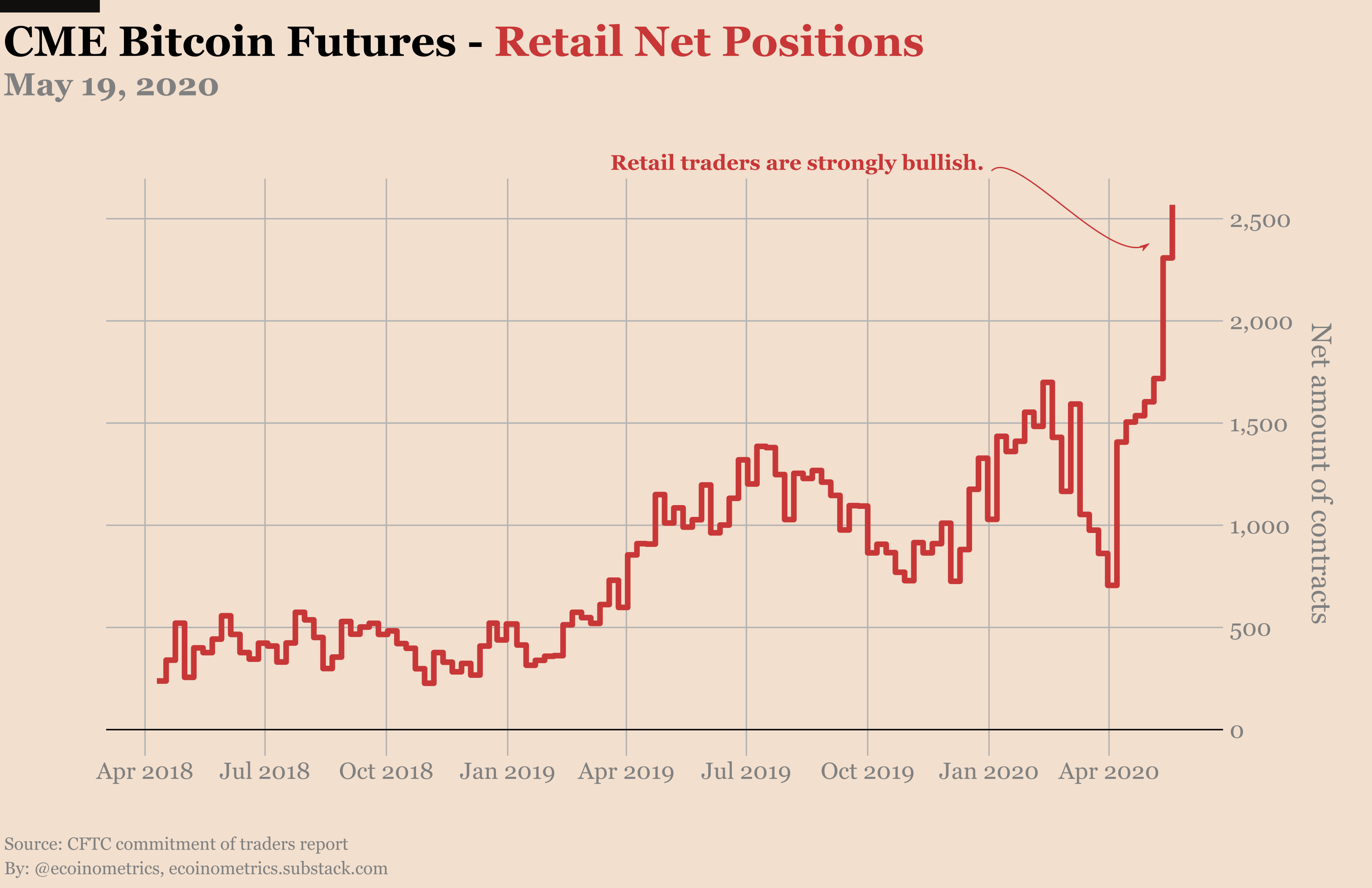

Meanwhile the retail accounts are more bullish than ever with record high net long positions.

But remember that the commitment of traders report is always lagging. So it will be interesting to see who took money off the table in the next few reports. Is it retail or smart money driven? We’ll see.

Looking forward:

Will Bitcoin break decisively over $10k?

Will the bull calls be paid this month?

Is the options market going to maintain this high level of trading activity?

Let’s keep an eye on that and see how it plays out.

If you liked this article please share and subscribe!