No Demand, No Rally: Bitcoin ETF Flows Still Weak

Also The Liquidity Tailwind Is Over & Hawkish Tone Persists as Macro Stalls

Welcome to Ecoinometrics' Friday edition.

Each week, we analyze the three most critical market signals impacting Bitcoin and macro assets, delivering institutional-grade insights through data-driven charts and analysis.

Today we'll cover:

No Demand, No Rally: Bitcoin ETF Flows Still Weak

The Liquidity Tailwind Is Over

Hawkish Tone Persists as Macro Stalls

Together, these signals paint a cautious picture. Institutional demand is tepid, financial conditions are tightening, and the Fed shows no signs of pivoting. That’s not a bullish backdrop, at least for now.

In case you missed it, here are the other topics we covered this week:

Essential Decision-Making Tools

Bitcoin Market Monitor - Key Drivers in Five Charts:

Bitcoin Market Forecast - Probability Scenarios & Risk Metrics:

Get these professional-grade insights delivered to your inbox:

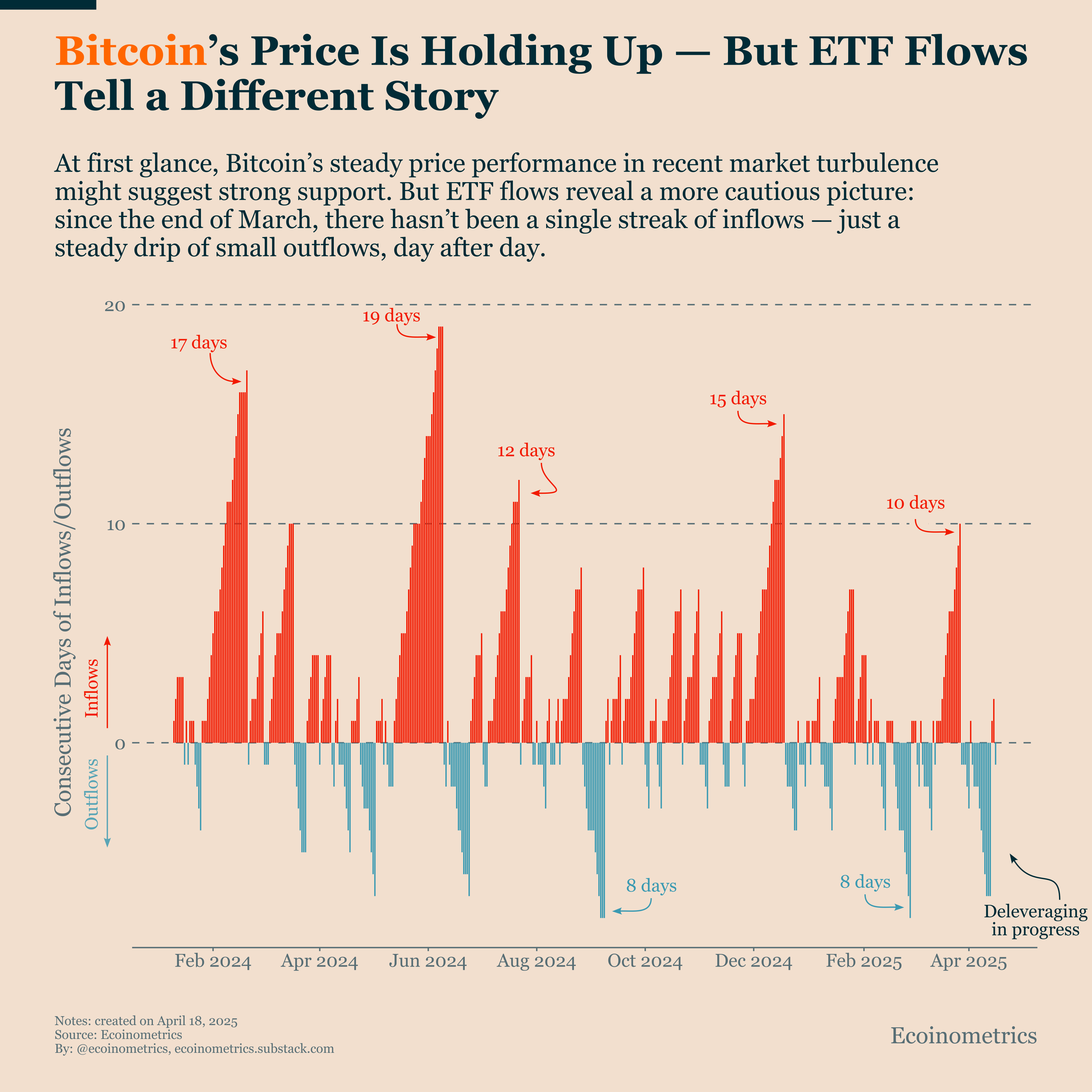

No Demand, No Rally: ETF Flows Still Weak

Since bouncing off the $75,000 level, Bitcoin has managed to hold a tight range around $84,000. You might think that stability, especially in the current uncertain environment, is a positive sign. And in many ways, it is.

But the real question is whether this price action is being driven by renewed demand or if it’s just technical noise. That distinction matters because the long-term outlook is very different depending on the answer.

If Bitcoin were supported by a return of institutional demand, we could argue there’s a higher probability of exiting the bearish pullback regime and entering a genuine phase of neutral consolidation.

The problem is: ETF flows aren’t showing that return of demand.

As the chart below shows, since the end of March, we’ve mostly seen long streaks of outflows, interrupted only by a few isolated days of inflows. Granted, those outflows haven’t been large. The rolling net flows over the last 30 days are close to zero.

So if you want to be optimistic, the best-case scenario is that we’re moving from a deleveraging phase to something more stable. But history tells us that it takes sustained inflows (at least 30,000 BTC over a month) to trigger meaningful price appreciation.

We’re nowhere near that kind of dynamic right now. So short-term upside remains limited. On top of that, this kind of weak demand environment increases the fragility of Bitcoin’s current price level. If volatility returns, the lack of ETF inflows may leave the price exposed.

The Liquidity Tailwind Is Over

Bitcoin doesn’t trade in a vacuum. As a risk-on asset, it’s highly sensitive to financial conditions in the U.S. And one of the best indicators for tracking that is the National Financial Conditions Index (NFCI).

The NFCI measures the overall tightness or looseness of financial conditions across credit, funding, and leverage markets. When the index goes down, conditions are loose, which supports risk assets. When it rises, conditions tighten, usually a headwind for assets like Bitcoin.

After the COVID crash, the Fed injected massive liquidity into the system, and the NFCI dropped to multi-year lows. That period of easy money helped propel Bitcoin to an all-time high of $69K in 2021.

But loose conditions also fuelled inflation. In response, the Fed launched an aggressive quantitative tightening campaign in 2022. Over the course of a year, financial conditions tightened rapidly, which coincided with a sharp correction in Bitcoin’s price.

When it became clear in 2023 that the Fed was nearing its terminal rate, financial conditions began to ease. Even without actual rate cuts or balance sheet expansion, markets relaxed yielding a two-year window of improving conditions. During that time, Bitcoin’s price rose nearly fivefold.

That easing trend, however, ended in February. Sticky inflation, uncertainty around U.S. trade policy, and the Fed’s ongoing hawkish stance have spooked markets. As a result, financial conditions are tightening sharply again.

If this turns into a sustained trend, the current Bitcoin bull market could stall or worse, reverse.

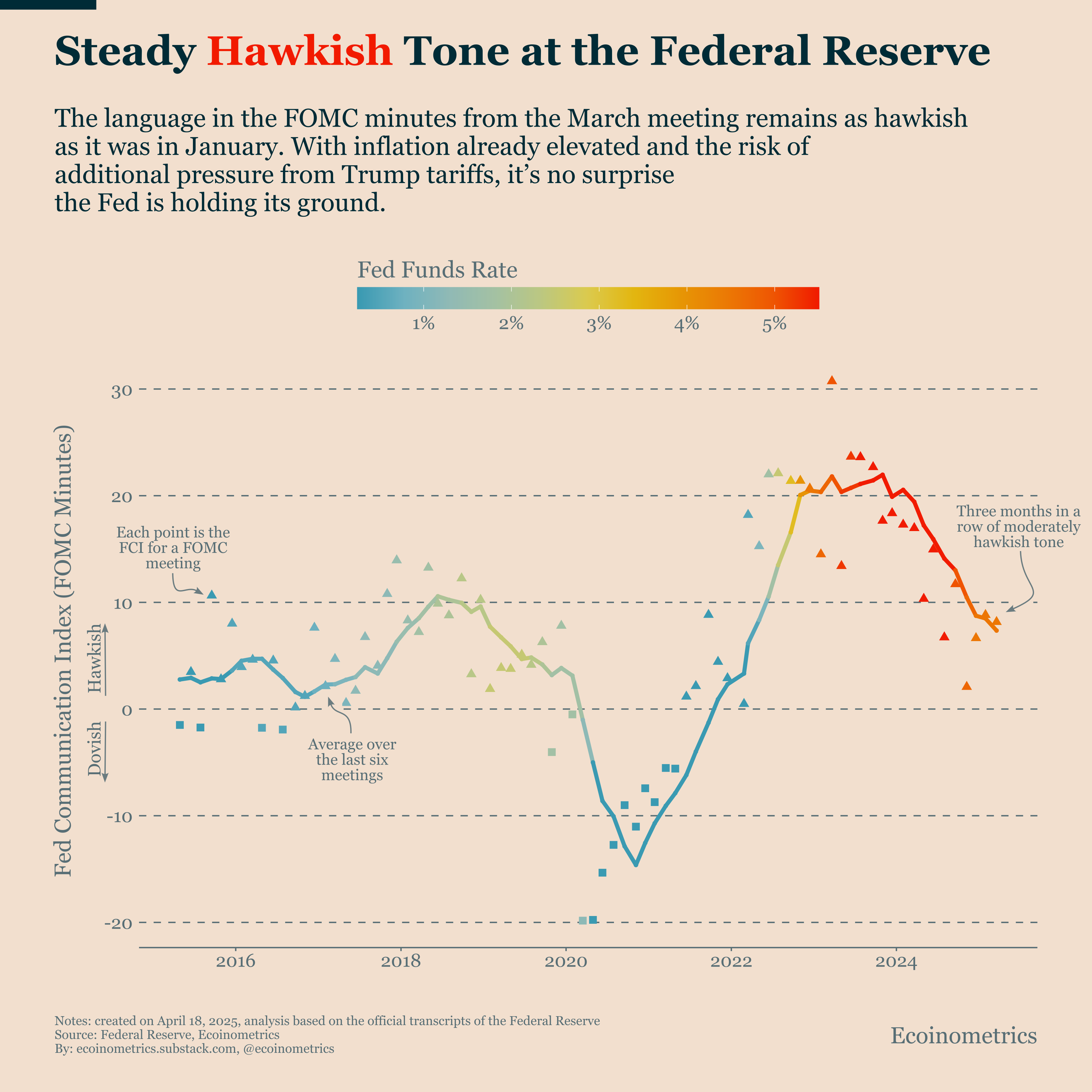

Hawkish Tone Persists as Macro Stalls

The Federal Reserve just released the minutes from its March FOMC meeting. We ran the text through our algorithm to calculate the Fed Communication Index, a quantitative score fine-tuned to assess how hawkish or dovish the Fed sounds in its official communications.

Markets pay close attention to that tone. What the Fed says often shapes expectations as much as what it does, especially because policy shifts are typically telegraphed well in advance.

For March, the Fed Communication Index once again reads hawkish. That’s not surprising, but the key point is this: it’s essentially the same level of hawkishness we saw in both January and December. We’re seeing a clear clustering in sentiment.

This likely reflects the macro backdrop, which hasn’t changed much in the past few months. The labor market is still tight, inflation remains elevated, and consumption trends are stable.

With inflation still the Fed’s primary concern, there’s no reason to expect a shift in tone unless we see a sustained move in the PCE index. If anything, the escalating trade tensions (particularly tariff risks) may push the rhetoric further in the hawkish direction.

That would mean tighter financial conditions ahead, and as we’ve already seen, that’s not good for Bitcoin.

That's it for today. Thanks for reading.

Cheers,

Nick

P.S. Every week, our team conducts extensive research analyzing market data, tracking emerging trends, and creating professional-grade charts and analysis.

Our mission: Deliver actionable macro and Bitcoin insights that help institutional investors and financial advisors make better-informed decisions.

Ready for institutional-grade research that puts you ahead of the market? Click below to access our premium insights.