Ecoinometrics - February 03, 2021

Portfolio allocation

Let’s say you don’t want to just hodl Bitcoin. Or maybe you already have a portfolio of assets and you are wondering what to do with Bitcoin.

The most important decision you have to make is allocation. How much of your portfolio should be allocated to Bitcoin?

Let’s have a look.

The Ecoinometrics newsletter decrypts Bitcoin’s place in the global financial system. If you want to get an edge in understanding the future of finance you only have to do two things:

Click on the subscribe button right below.

Done? That’s great! Now let’s dive in.

Portfolio allocation

How much Bitcoin should you hodl? This is a pretty vast topic.

Today let’s just keep things simple. We want to be able to reason about this question without falling into technical details that might obscure the big picture.

What kind of portfolio are we running?

The rules:

We don’t hold any cash. We are 100% invested at all times.

We can only be long Bitcoin, the SP500 and gold.

We fix the percentage of our portfolio allocated to each asset and we rebalance to this fixed percentage on the first of every month.

What does rebalancing mean?

Say I’ve fixed my percentage allocations to be 50% Bitcoin and 50% SP500.

At the end of the month Bitcoin has had a good run and suddenly my portfolio looks like 75% Bitcoin and 25% SP500.

Rebalancing means that on the first trading day of the next month I’ll sell some of my Bitcoin holdings and use the proceeds to buy more of the SP500 so that I’m back to 50% Bitcoin and 50% SP500.

Pretty simple right?

Bitcoin, the SP500 and gold are uncorrelated over long enough periods of time. That means you can expect that putting them together in your portfolio with some rebalancing mechanism should give you more than the sum of the parts.

Now we have to figure out what percentage allocation to choose.

To help with this choice we can run a bunch of scenarios on historical data and look at some performance metrics:

The total return or annualized return of the portfolio over the historical period.

The largest drawdown of the portfolio over the historical period.

The risk adjusted return of the portfolio over the historical period. For that I’ll use the Sortino ratio calculated from monthly returns. See here for why I like to use the Sortino ratio.

Here are a few extreme scenarios using the past 8 years as our historical data.

Bitcoin 100%, SP500 0%, Gold 0% aka all in on BTC:

Annualized return 100%, largest drawdown 89%, Sortino ratio 1.26.

If you can stomach some massive drawdown then this is a great risk adjusted performance.

Bitcoin 0%, SP500 100%, Gold 0% aka all in on stonks:

Annualized return 9%, largest drawdown 37%, Sortino ratio 0.28.

That doesn’t look so good compared to BTC. You only get 9% annualized return while still having to put up with a 37% drawdown…

Bitcoin 0%, SP500 0%, Gold 100% aka the Peter Schiff portfolio:

Annualized return -1%, largest drawdown 42%, Sortino ratio 0.

No comment. Unless you timed the bottom somehow, holding gold alone isn’t great to say the least.

Ok, so that’s what you get if you put all your eggs in one basket. But obviously if you do that there is no rebalancing at all.

Bitcoin looks great but if history repeats itself you might still need to deal with very large drawdowns until we reach much broader adoption.

But what if we combine two assets? Can we improve our performance? Ideally we’d like to add something to Bitcoin to reduce our risk of large drawdowns. And adding Bitcoin to any other asset would certainly juice its performance.

Bitcoin 0%, SP500 50%, Gold 50%:

Annualized return 4%, largest drawdown 23%, Sortino ratio 0.27.

Alright… that didn’t improve anything really.

Bitcoin 50%, SP500 50%, Gold 0%:

Annualized return 63%, largest drawdown 58%, Sortino ratio 1.29.

That’s better already. Adding stocks to Bitcoin reduced the size of the largest drawdown while keeping the risk adjusted return the same.

Bitcoin 50%, SP500 0%, Gold 50%:

Annualized return 56%, largest drawdown 64%, Sortino ratio 1.16.

Not as good as adding stocks but that’s fine.

Conclusion? Yes you can get some performance improvements by mixing those assets together.

Click on the chart to see the details of those scenarios.

If your goal is to get those drawdowns under control then you’ll definitely want to make a more balanced allocation mix. Example.

Bitcoin 34%, SP500 33%, Gold 33%:

Annualized return 43%, largest drawdown 45%, Sortino ratio 1.21.

Adding gold on top of stocks helps to reduce again the maximum drawdown while keeping your risk adjusted return in the same ballpark.

The whole point is that when you mix uncorrelated assets together in your portfolio you open yourself to the possibility of improving your risk adjusted return.

Ok. Few. That was a lot of numbers… but that only covered a few possible scenarios...

After all, any combination of Bitcoin, the SP500 and Gold is allowed in this portfolio.

Don’t worry I got you covered. I’ve run the numbers for you.

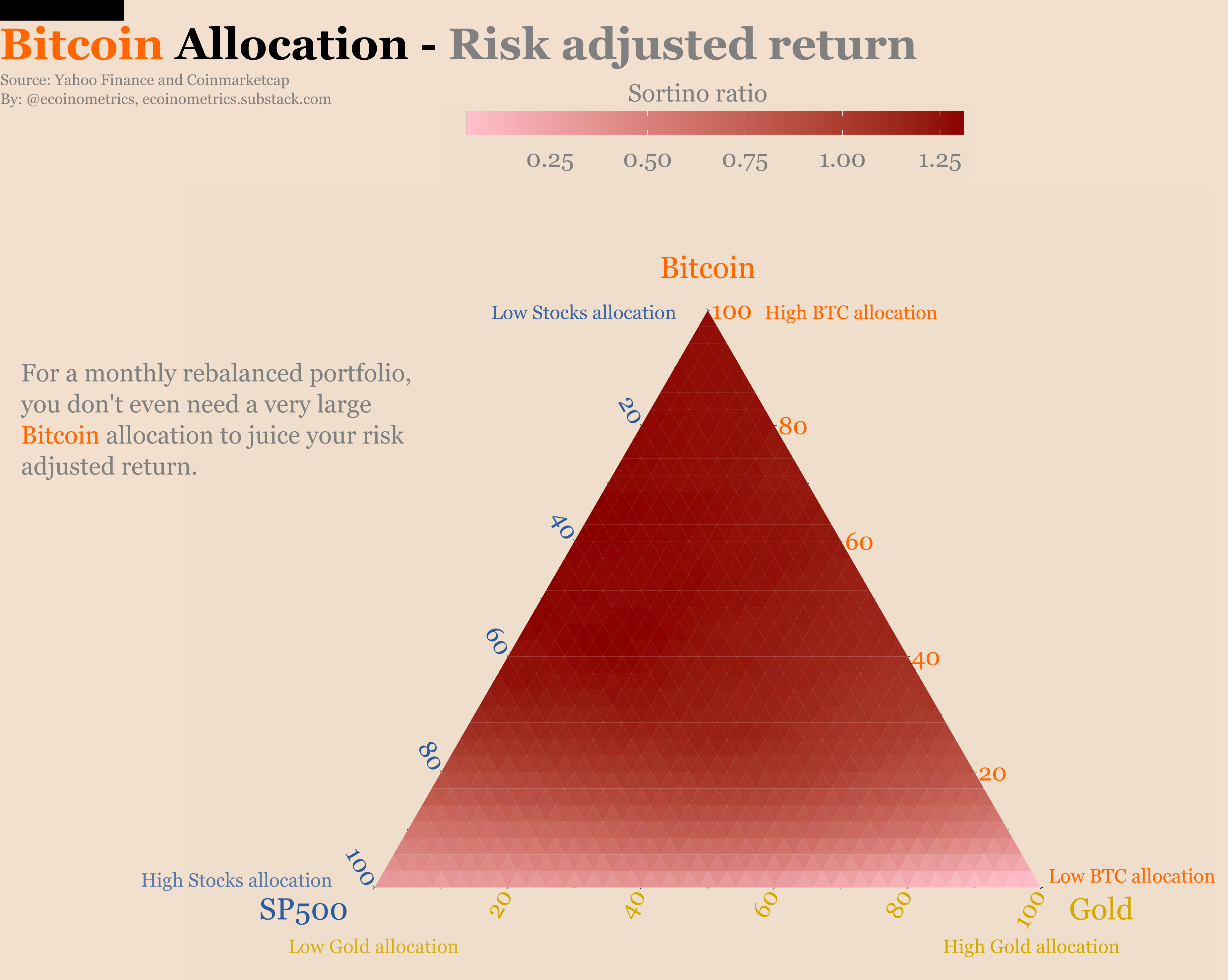

To make it easy to understand, let’s use a bunch of ternary graphs to look at the results.

First how do you read those? If you aren’t familiar don’t panic. It’s easy.

Look at the chart below. You can see a triangle. Each corner is labelled Bitcoin, SP500, Gold. The closer you get to a corner the larger the allocation to the asset.

Example. Bitcoin is the top corner. That means the higher you are inside the triangle the larger your Bitcoin allocation. The top corner is a portfolio 100% allocated to Bitcoin.

The SP500 is the bottom left corner. The more you go towards the bottom left the higher your SP500 allocation. At the bottom left corner you are 100% allocated to the stock market.

In the middle of the triangle you get a portfolio that’s exactly one third Bitcoin, one third SP500 and one third Gold.

The colour encodes our performance metric. The darker the colour the larger the metric.

Take a look.

When it comes to annualized returns there is no surprise. The larger your Bitcoin allocation the better.

For drawdowns this is the opposite. The larger your Bitcoin allocation the worst the drawdowns. But adding a mix of stocks and gold helps with that.

Finally for risk adjusted returns we see something interesting. You don’t need to be unreasonably long Bitcoin to get a great Sortino ratio.

If you are in the middle of the triangle you are already in deep red territory. That means a balanced portfolio of equal parts Bitcoin, SP500 and gold already gives you a nice risk adjusted performance.

At this point some of you are thinking: “so what is the BEST portfolio composition”?

Stop.

That’s not the way to think about it.

There are no magic numbers.

The main reason is that this is all based on historical data.

You’ve heard it before past performance is not indicative of future results. That doesn’t mean my analysis is useless. But that means there is no point in fine tuning your allocation parameters to the past.

Instead you should use this analysis to develop some heuristics for the future.

You only need to ask two questions:

Why does mixing Bitcoin, the SP500 and gold improved the risk adjusted return of this portfolio?

Will these factors continue to be true in the future?

The answer to the first question can be divided in two parts:

Those three assets are uncorrelated over long enough periods of time. Thus rebalancing helps smooth the returns by mitigating some of Bitcoin’s downside volatility.

Bitcoin has been growing at a much faster rate than the stock market. That’s why having it in your portfolio gives a huge performance boost.

In my opinion this will still hold for the years to come.

Bitcoin is still in the adoption phase. That can only generate more exponential growth in the future.

Bitcoin, the SP500 and gold have separate market dynamics. So again there is no reason for those assets to all become correlated over long periods of time.

Conclusion: you should go ahead and add Bitcoin to your portfolio if you haven’t already done so.

CME Bitcoin Derivatives

We are already running a bit long for today’s newsletter so let’s have a quick look at the CME Bitcoin derivatives.

After the January contract expired last Friday the trading activity has been sliding.

The Commitment of Traders report was showing that before the expiry both retail traders and the smart money had been deleveraging. This is just a continuation of that.

Same thing goes in the options market. Except for people buying puts in case BTC drops back below $30k there is nothing going on.

That’s it for today. If you have learned something please subscribe and share to help the newsletter grow.

Cheers,

Nick

The Ecoinometrics newsletter decrypts Bitcoin’s place in the global financial system. If you want to get an edge in understanding the future of finance you only have to do two things:

Click on the subscribe button right below.

Done? That’s great!