Ecoinometrics - January 13, 2021

Follow up...

So last week I wrote about the drawdowns during the previous Bitcoin bull markets. Then a couple of days later we get a 27% pullback… I swear I didn’t have any insider information…

But it is time for a follow up.

The Ecoinometrics newsletter decrypts Bitcoin’s place in the global financial system. If you want to get an edge in understanding the future of finance you only have to do two things:

Click on the subscribe button right below.

Done? That’s great! Now let’s dive in.

Follow up

Last week we looked at the drawdowns during the previous bull cycles.

To clarify, this analysis didn’t give any idea on how you would evaluate the probability that a pullback would happen. It simply gathered some statistics on what drawdowns look like when they happen.

But now that we are in the middle of one, let’s see how the current dip compares to the historical ones.

At the end of January 12:

From top to bottom this dip was about 27%.

It took 4 days to find a bottom.

That would put us here...

As you can see it is relatively rare to have dips of this size. Only about 15% of the historical drawdowns are larger than this one.

At the same time this dip looks similar to the significant dips that happened on the way up during the 2017 post halving bull market.

So as far as good opportunities to accumulate more during a bull market it doesn’t get much better than that.

Which means that if you were waiting to buy the dip now is a good time to act. Don’t chicken out.

We aren’t yet out of this drawdown so who knows if the bottom is in. As I’m writing this BTC went as low as $30,500 but is currently back at $34,500.

If your thesis is that this halving cycle is going to play out no different that the previous ones then just zoom out. This is just a blip in the big picture.

Now moving on to more stats, someone had a great question on Twitter:

Basically, how does the price action before a drawdown influence the size of the dip?

What’s your guess? I would have said that the bigger the run up before a drawdown the larger the correction.

So what is it? Here is a partial answer to this question.

Define the run up between two drawdowns as the period of continuous growth starting when the price moves above the previous top and finishing when the next pullback starts.

That means the run up is the price surge that happens between two drawdowns (here analyzed using daily candles).

We can plot the magnitude of this run up against the magnitude of the drawdown that follows it to see if there is any relationship between those two.

Here is what you get using a log-log chart…

I haven’t run any regression statistics on that but you can see that roughly you get a linear relationship between the log of the run up and the log of the dip.

So here is your answer: yes the larger the run up, the larger the dip.

I usually try to keep this newsletter relatively non technical when it comes to doing statistical analysis so I won’t dig deeper on the subject.

But if there is enough interest from you readers to get more in depth statistical analysis in some special issues of the newsletter I’m open to the idea. Let me know.

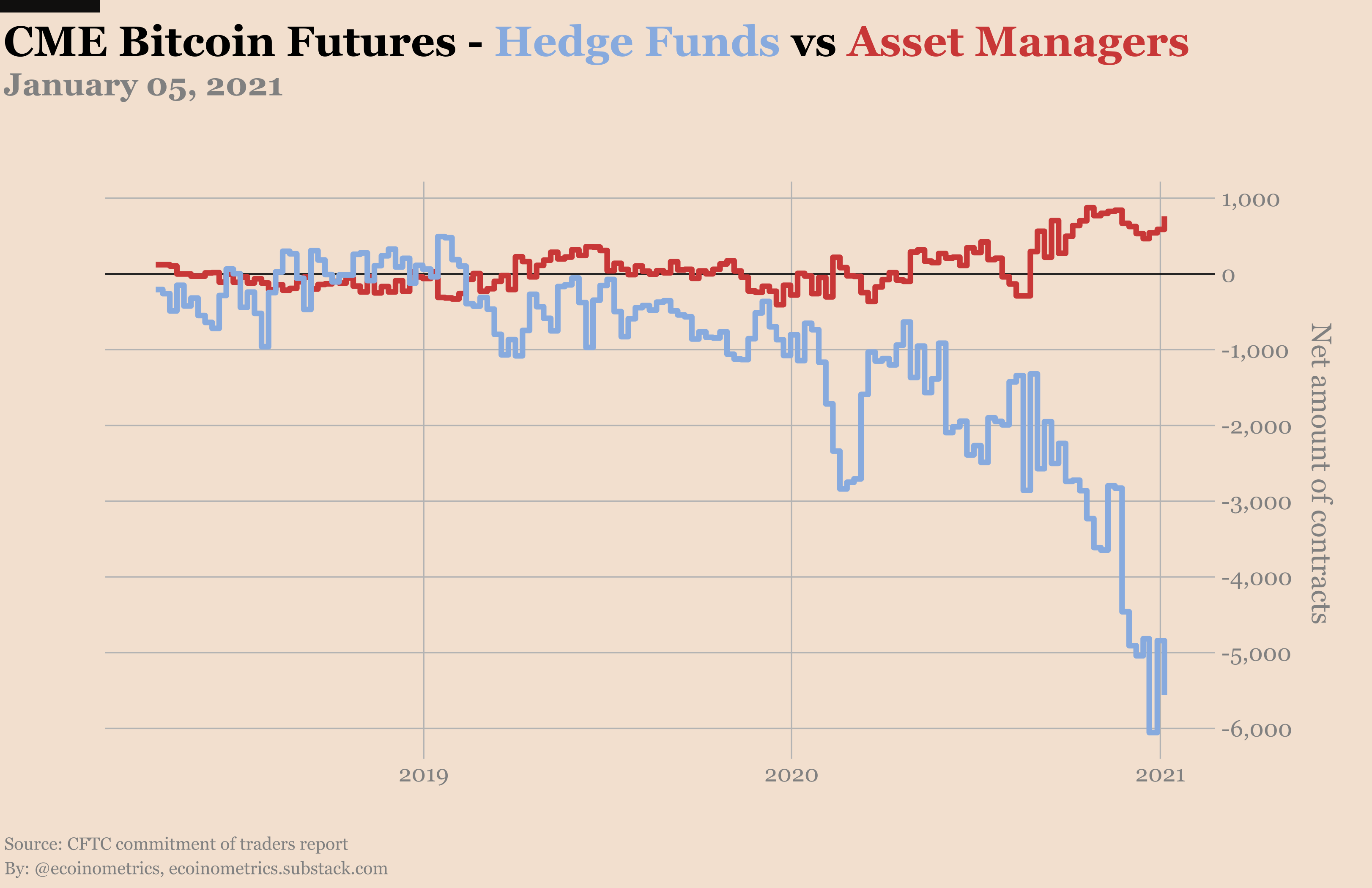

CME Bitcoin Derivatives

There is nothing like a sharp pullback to drive trading activity. This is exactly what we have witnessed during the trading session on Monday.

Result, a new record in traded volume on the CME:

27,690 contracts changed hands (with each contract being worth 5 BTC).

This corresponds to more than $4 billion of volume in one trading session.

Impressive, but that didn't change the open interest very much. So all of this just amounts to shuffling positions around.

Meanwhile the theme on the futures market is still: milk those premiums. Sure, when you look at the Commitment of Traders report you see that some short positions get closed here, some long positions get opened there, but when you squint at the charts there is only one big pattern.

The smart money is not net short Bitcoin. They are neutral. They are playing the arbitrage game.

From time to time I hear that the sole purpose of the CME Bitcoin futures is to suppress the BTC price. Honestly that theory doesn't have legs. This is not what you see play out in the market. People in the finance business are motivated to make money. That's the primary driver.

Right now what is literally printing money is to run neutral strategies arbitraging the premium between spot and futures on Bitcoin. So that's what people do. I don't think there are deeper motives to uncover.

Now, what's going on with the CME Bitcoin options market. Not much... not much. I mean, I'm not suggesting that it is dying the same way the Bakkt options market did, but things aren't looking great.

Today, January 13, the CME options market is one year old:

- January 13, 2020 Open Interest 55 contracts (start)

- June 06, 2020 Open Interest 5400 contracts (max)

- January 13, 2021 Open Interest 2000 contracts (now)

Look at the trend and make up your mind...

The lack of interest in the options market probably has to do with the kind of strategies traders are running on the cash settled futures market. Your use for options contract is very limited if you are just running the basis trade arbitrage all day long.

We'll see where this goes in the next 6 months.

That’s it for today. If you have learned something please subscribe and share to help the newsletter grow.

Cheers,

Nick

The Ecoinometrics newsletter decrypts Bitcoin’s place in the global financial system. If you want to get an edge in understanding the future of finance you only have to do two things:

Click on the subscribe button right below.

Done? That’s great!

Ever do a video explaining some of the more complicated futures charts?

Great newsletter!! ♥️ I read that smart players are almost record net short from the chart. What did I miss regarding smart money not being that short now as you wrote?