Ecoinometrics - March 03, 2021

Down days...

Volatility comes up all the time when we talk about Bitcoin.

Is Bitcoin too volatile? Volatile compared to what? How do you even look at volatility?

Let’s look at some stats.

The Ecoinometrics newsletter decrypts Bitcoin’s place in the global financial system. If you want to get an edge in understanding the future of finance you only have to do two things:

Click on the subscribe button right below.

Done? That’s great! Now let’s dive in.

Down days

Raise your hand if you haven’t heard this one before “Bitcoin is not a good investment because it is too volatile” or that one “Bitcoin is too volatile to be a medium of exchange”.

These are two common critics.

I’ve dedicated a number of issues of this newsletter explaining why these points are not relevant. You can go here for an example but the main ideas are pretty simple:

Looking at volatility alone is not relevant to decide whether or not an asset is a good investment. The only metric you should care about is the risk adjusted return. Or more specifically the return adjusted for downside risk such as in the Sortino ratio. On that scale Bitcoin is a great investment.

Bitcoin is very early on the adoption curve. In the current phase, the rapid growth of the network means an exponential increase in its value. Obviously this does not result in stable prices. As adoption grows it will naturally reach a mature stage and transition to something that can be used as a medium of exchange. But we aren’t there yet. No point worrying about that.

But still, volatility is a recurring question so I thought we’d take a slightly different approach today.

When I talk about volatility I tend to use a somewhat technical definition. You take a given period of times and look at the variance of the daily returns over that period.

When you look at it this way, the picture is clear:

Bitcoin is more volatile than say gold or your favourite index.

But there are assets like Tesla which are about as volatile as Bitcoin.

And some stocks are even more volatile than Bitcoin.

But this kind of volatility is not exactly the one your read about in the news. The volatility most people have in mind is the Bloomberg volatility: "Today Bitcoin peaked at $X dollars but finished the day down 20%! Bitcoin is dead."

How is Bitcoin doing on this “news headlines” volatility scale?

Here are some stats.

Take all the days for which the daily return was negative. We'll call these down days. Now look at the percentage change from the high to the closing price. That percentage is typically what will make the headline of the news.

We can look at the distribution of this high to close amplitude for all the down days of a bunch of assets and see how Bitcoin compares.

On the graph below:

Each point is a down day.

The further you go to the right the bigger the drop.

For each asset you can see the density of points at each high to close level.

The higher the density the more down days in the region.

The darker the colour of the density the closer you are to the average high to close amplitude.

Alright, take a look.

Can you spot what distinguishes Bitcoin from the other assets?

The tail. The difference in the tail.

For most assets the distribution of the down days can be decomposed as:

The bulk in the the 0% to 5% drop range.

The tail extending from 5% to 10%.

A few rare events extending past 10%.

For Bitcoin the distribution looks more like:

A bulk in the 0% to 10% range.

A fat tail in the 10% to 20% range.

A few rare events past 20%.

So if that high to close is your point of reference for looking at the volatility then yes Bitcoin tends to be more volatile to the downside.

But you could be surprised that it isn't even more volatile for one reason.

There is a crucial difference between Bitcoin and those other assets: Bitcoin trades all around the world, 24 hours a day, 7 days a week, all year long and without circuit breakers.

If your average stock traded in those conditions it might end up with a fat tail too.

Interestingly if you break down the distribution of the down days by halving cycles the fat tail does not seem to become thinner over time.

But honestly it is still early for Bitcoin.

It will be time to revisit that at the end of this halving cycle.

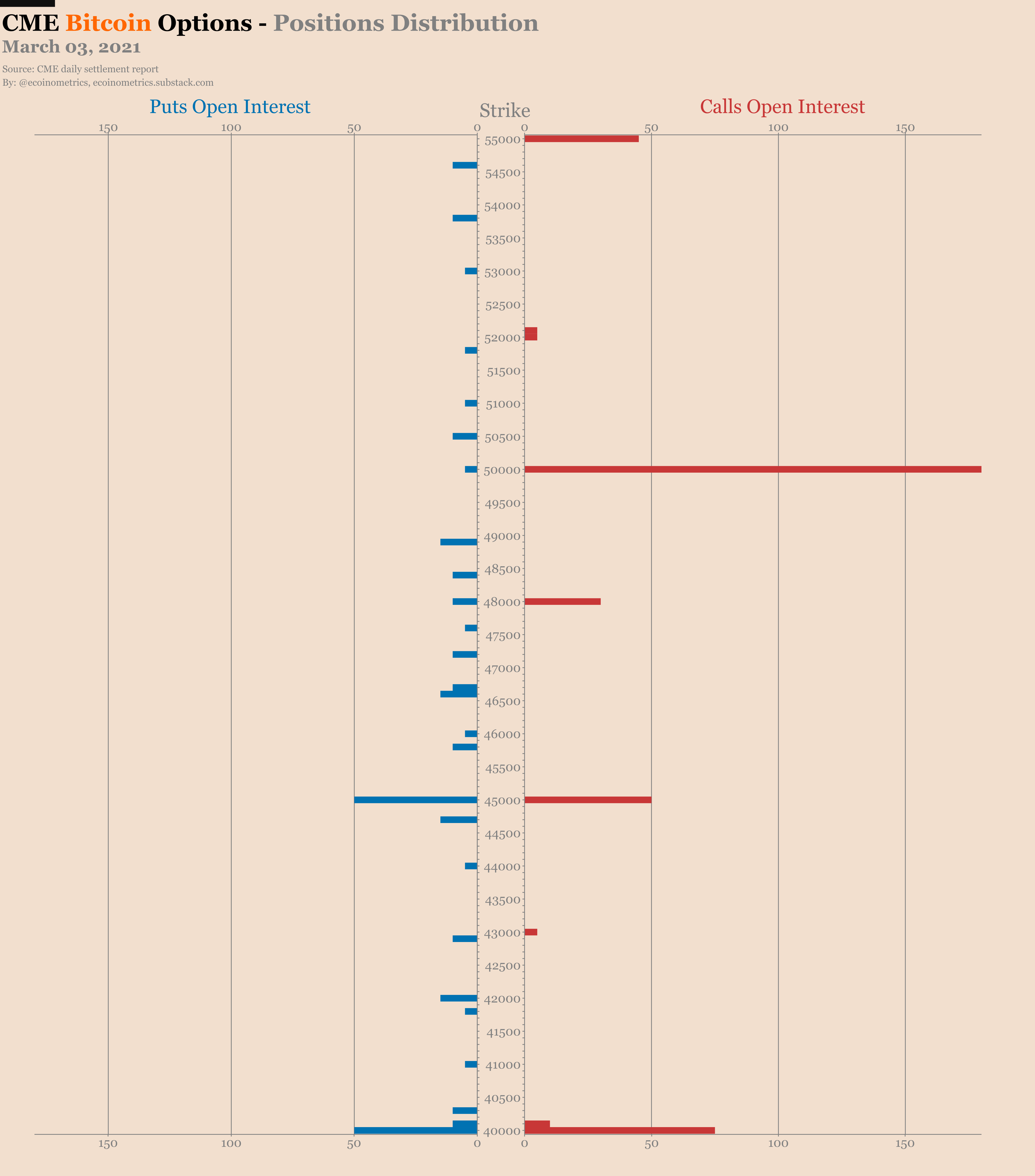

CME Bitcoin Derivatives

The theme of this week for the CME Bitcoin derivatives is deleveraging. The February contract expired last week and the result is a significant drop in open interest.

So obviously the main question is who closed those positions? Is it the shorts from the basis trade? Is it the traders long the momentum strategy taking profit?

The answer to those questions is: yes.

All of the above.

According to the latest data from the commitment of traders report:

Retail traders closed a lot of their long positions probably taking some profit with the drop last week.

At the same time the smart money closed some short positions and some long positions although in much smaller amounts than retail traders.

We’ll have to see where this is going next week. Could be something only temporary with the combination of the end of the month and the drop.

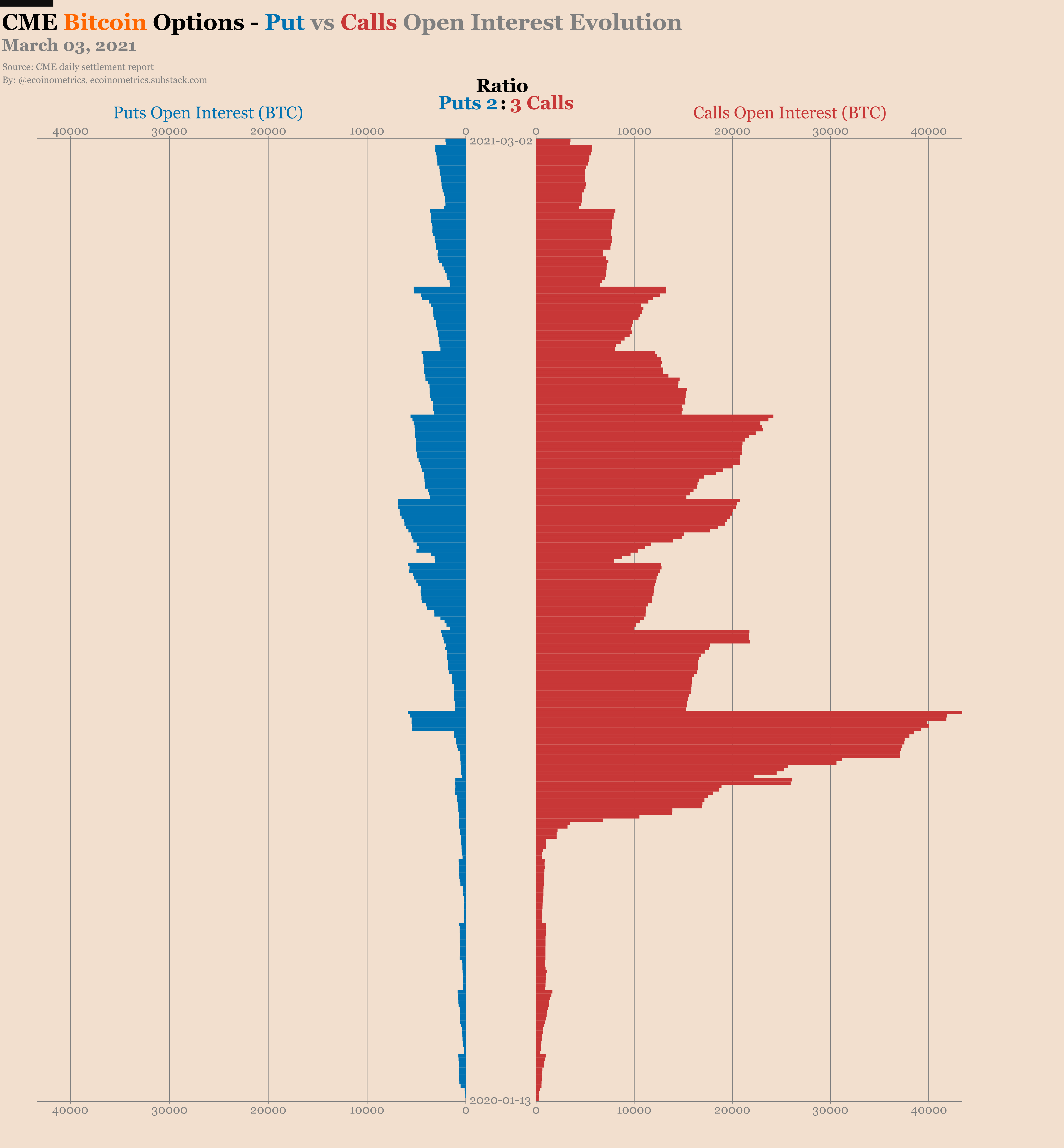

The options market continues to shrink. At this rate the open interest will vanish in a few months.

We’ll look at that in more detail next week.

That’s it for today. If you have learned something please subscribe and share to help the newsletter grow.

Cheers,

Nick

The Ecoinometrics newsletter decrypts Bitcoin’s place in the global financial system. If you want to get an edge in understanding the future of finance you only have to do two things:

Click on the subscribe button right below.

Done? That’s great!