Ecoinometrics - May 19, 2021

Inflation hedge...

Bitcoin is digital gold. That’s the main narrative driving adoption. To be a good store of value, you expect that Bitcoin can keep up with inflation.

But it feels like some people have lost their perspective on what that means.

The Ecoinometrics newsletter decrypts Bitcoin’s place in the global financial system. If you want to get an edge in understanding the future of finance you only have to do two things:

Click on the subscribe button right below.

Done? That’s great! Now let’s dive in.

A hedge against inflation

Apparently not everyone is convinced that Bitcoin can be a hedge against inflation:

And you know what? Joe’s observation in the article is correct… the conclusion isn’t.

But let’s backoff a minute.

Last week the US had some CPI inflation print that came up hotter than expected. Even slightly hotter than what you’d get after taking the base effect from the lows of April 2020 into account.

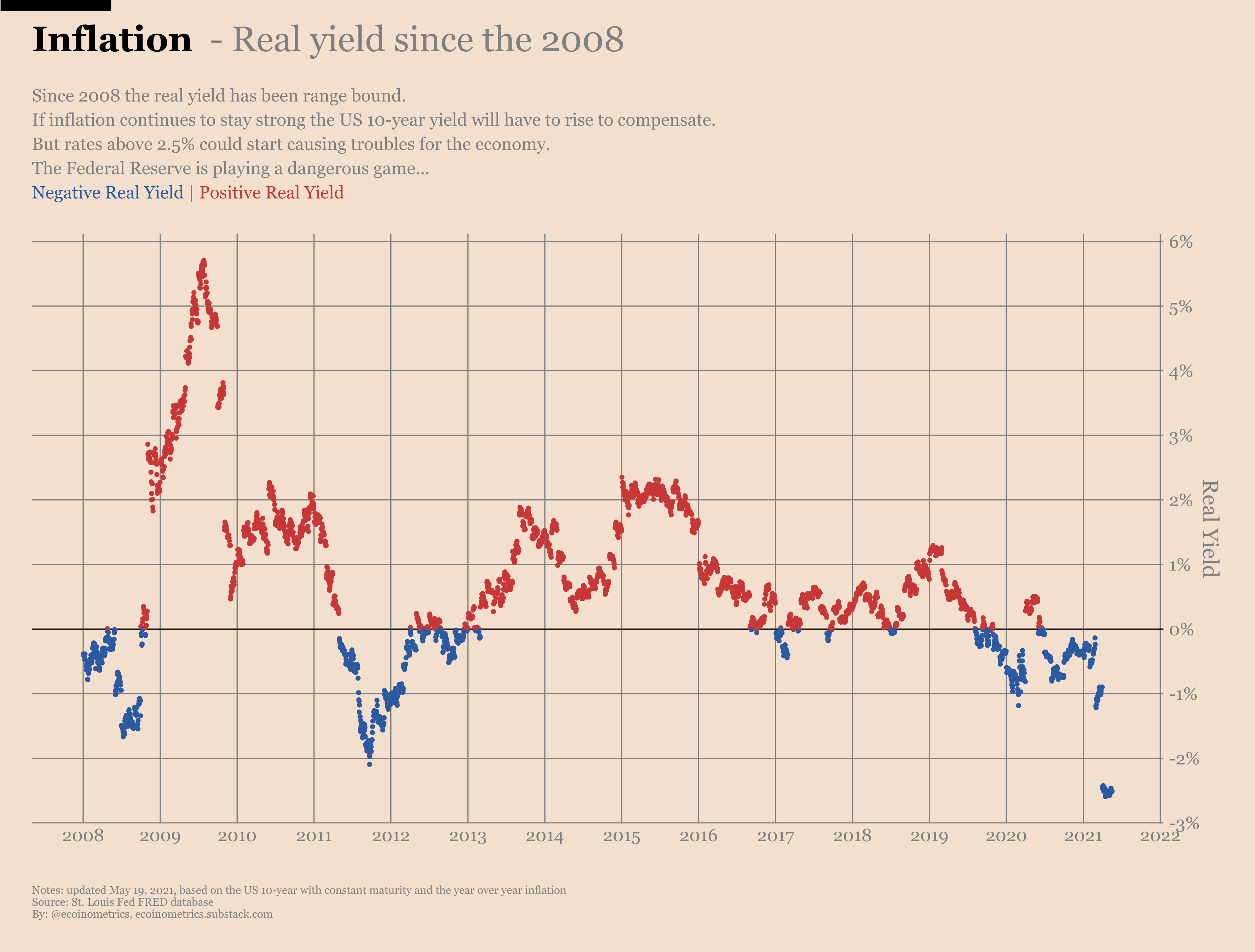

A sudden rise in inflation coupled with the US 10-year Treasury yield staying pretty stable sent the real yield out of the range it established since 2008.

The real yield is calculated by taking the yield of your favourite bond, here the US 10-year, and subtracting the inflation rate.

If the real yield is positive, holding your US Treasury bond does preserve your wealth.

If the real yield is negative, holding your US Treasury bond is not enough to keep up with inflation.

Now a store of value like gold or Bitcoin does not produce any yield. So if you can get a positive real yield with bonds, parking your cash in a store of value can look less attractive.

But when the real yield is negative it is game on for any store of value.

Now, after the CPI data came out last week, Bitcoin moved lower. Conclusion from Joe: Bitcoin is not a hedge against inflation...

Alright, maybe one data point is a bit light for this kind of conclusion no?

The fact is, to qualify as a hedge against inflation what Bitcoin did in any given day is completely irrelevant.

Inflation is a phenomenon that erodes the purchasing power of your cash over a certain period of time. But that period of time is definitely longer than a day. We are talking about something that plays out over months or years.

So no, the price action from last week does not disqualify Bitcoin as a hedge against inflation.

But Joe’s observation is correct. While Bitcoin may be a hedge against inflation over the long run, it does not trade like one on a day to day basis. And the reason is simple.

Financial institutions are the one trading around inflation over short time frames. But most financial institutions haven’t gotten their hands on Bitcoin yet. As a consequence Bitcoin does not trade like gold.

This behaviour is simply a function of the level of adoption of Bitcoin as a store of value within the global financial system.

Actually we could use that as another measure of Bitcoin’s adoption by traditional finance. The more Bitcoin becomes sensitive to changes in the real yield, the more it becomes like a traditional store of value.

So how does THE traditional store of value aka gold behave with respect to real yields?

Well if we go way back, the real yield was negative on average in the 70s and early 80s. Then things got better in the mid 80s. And since then we have been in a very long downtrend that has more to do with falling bond yields than rising inflation.

Check it out.

Now let’s do the following:

Let’s plot the price of gold from 1970 to now (on a log scale).

Each point representing the price of gold is coloured based on the real yield on that day.

The lighter the colour the higher the real yield. The darker the colour the lower the real yield.

Here is what we get.

Observations:

Relative changes in real yield seem to do a pretty good job at explaining the long term trends in the gold market.

Typically when the curve shifts from light to dark, gold is rising and when it shifts from dark to light, gold is falling.

But this is not an exact science.

It definitely looks like investors really start to consider buying gold only when the real yield is below 2%. Relative changes above that level don’t seem to have any long term impact on the trend.

For a more detailed view of recent data here is a zoom on the period from 2008 to now.

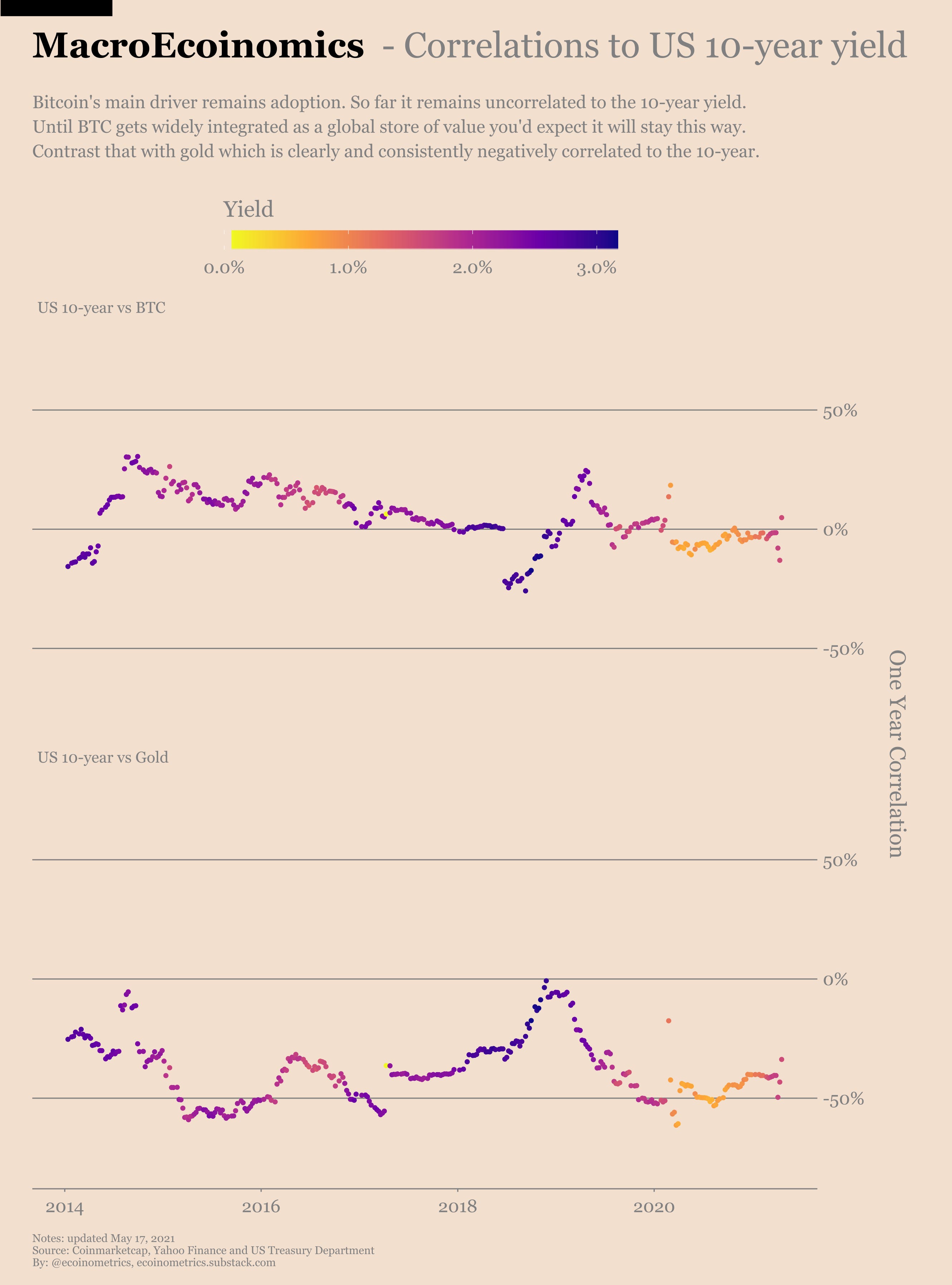

With Bitcoin we don’t have (yet) the luxury to go back 50 years and look for patterns. But as you might have expected, for the past three cycles real yield doesn’t drive the market.

The growing demand coming from adoption coupled with the post-halving supply crunch is what’s starting the big trends.

See for yourself.

When Bitcoin gets larger and adoption within financial institutions gets wider we’ll likely see real yield play a more important role in the long term trends.

But we are not there yet.

For now enjoy Bitcoin as an asset uncorrelated to gold and the bond market. Adoption alone should be enough to keep up with inflation for a while.

CME Bitcoin Derivatives

Bitcoin is taking a dive. But unfortunately the data for the positions of traders on the CME comes with a one week lag.

Right now all we have is the Commitment of Traders report from May 11, 2021. On that date Bitcoin was doing fine, hanging around $55k. So all we can see is how traders were positioned just before things started going south.

Interestingly there have been two trends in the retail crowd since the start of the year:

The amount of long positions is on a significant downtrend.

The amount of short positions is slowly rising.

So somehow the sentiment was already tilted towards a correction before the whole Tesla story…

But at the same time the smart money has remained unfazed by the price action.

That’s understandable.

The smart money is running an arbitrage strategy (the basis trade) while retail traders mainly run directional strategies.

So the smart money cares about spreads (relative movements) while retail traders need to follow the momentum.

We’ll need to check out two things in next week’s data:

Is the retail crowd buying this correction or getting short? That would give a hint about the general sentiment in the futures market.

Is the price collapse making the futures premium over spot smaller? If the premium is shrinking we might see a deleveraging of the basis trade.

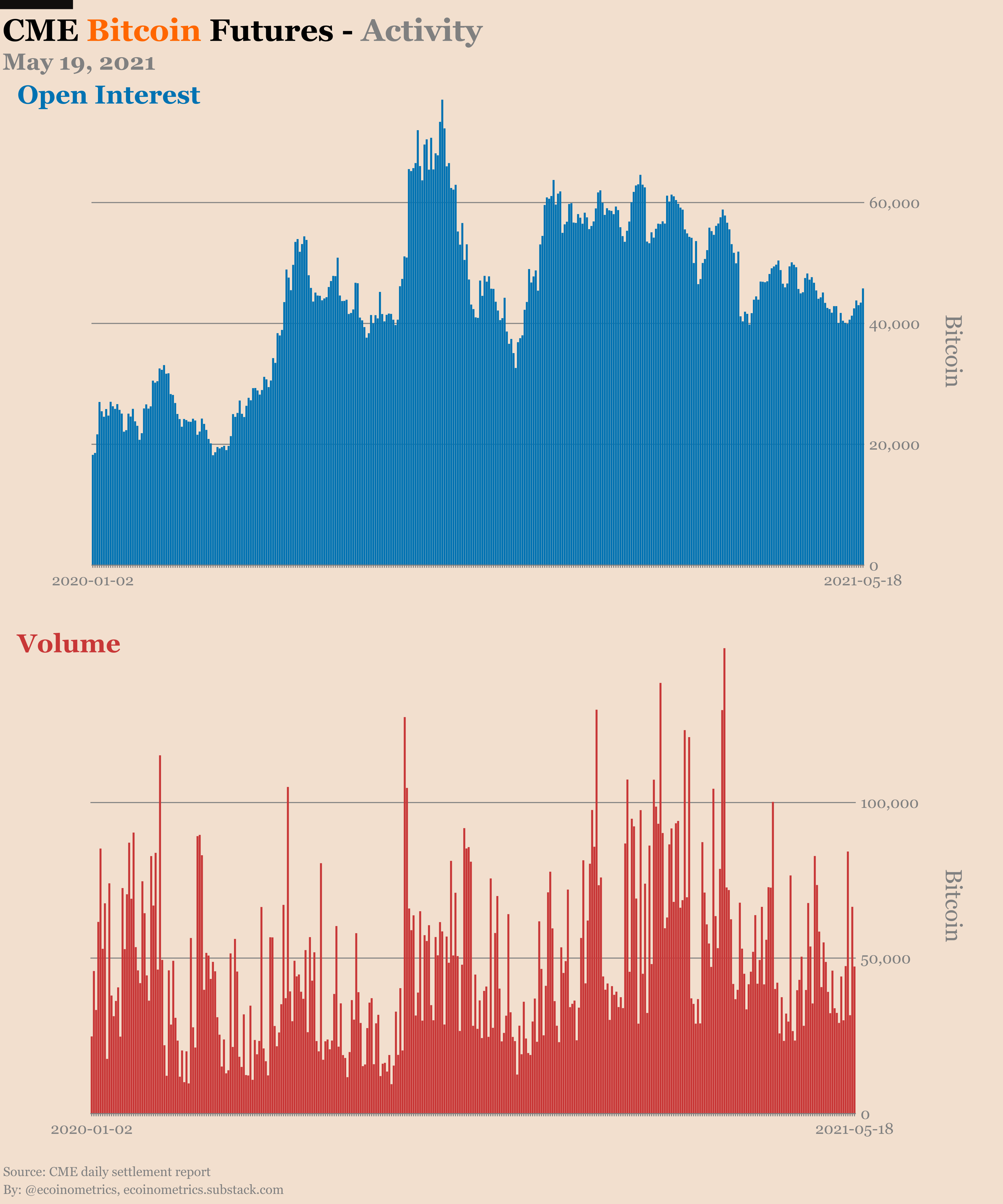

Note that despite Bitcoin falling hard and fast there has been no massive surge in trading activity on the CME futures.

No record in daily traded volume. Only a moderate increase in the open interest.

So at least it doesn’t look like everyone is panicking.

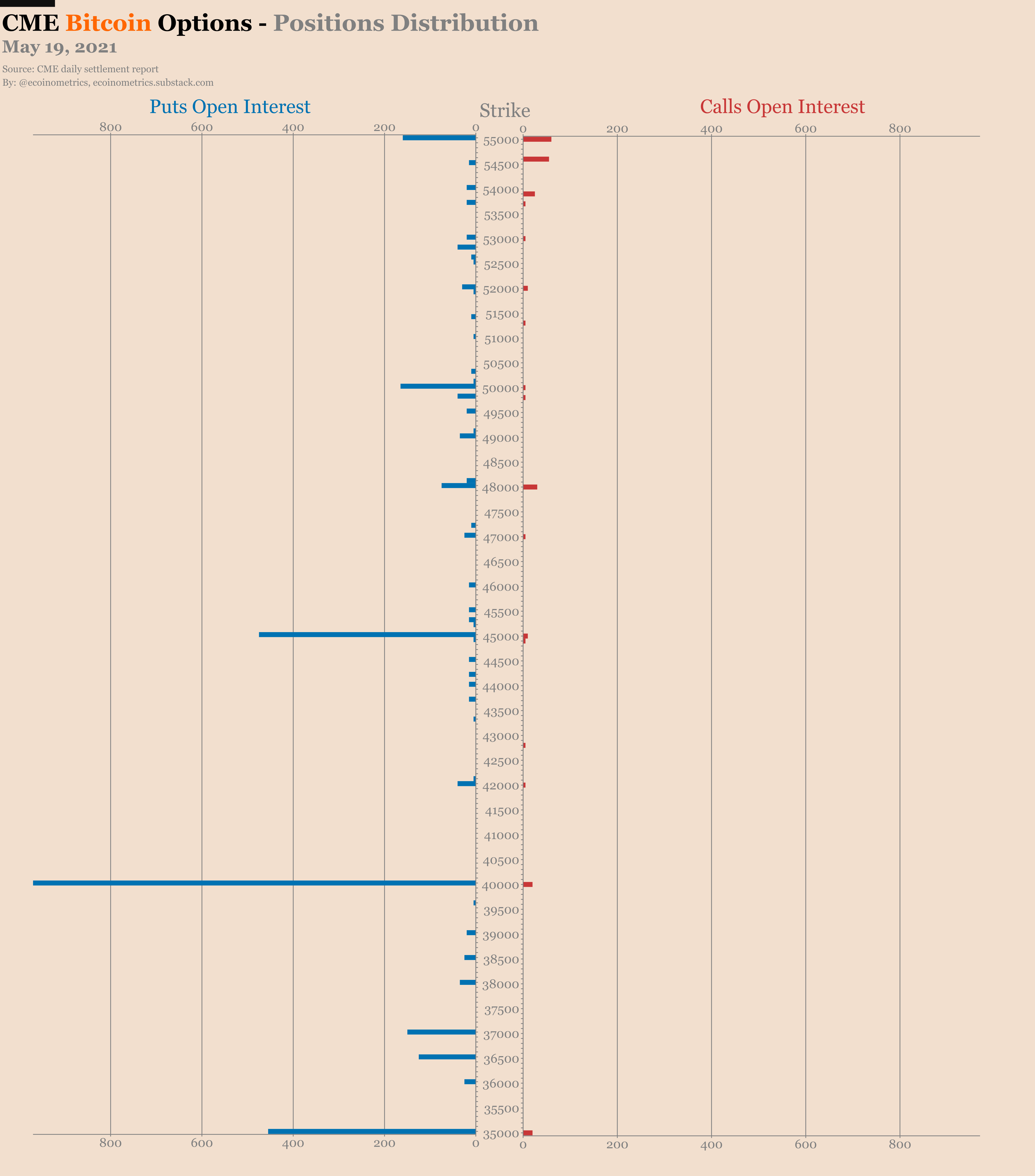

You know how we have been observing for weeks that the puts to calls ratio is at an all time high?

Well that was a pretty good timing by options traders…

When the CME options market closed yesterday BTC futures settled at $43,150. At that price, for the May contracts that expire in 10 days:

Only 4% of the calls are in the money.

But 64% of the puts are in the money.

This is basically the reversed situation compared to what we see usually.

Good bet for those who bought puts betting on a dip. Also good bet for those who decided they needed to buy protective puts on their long BTC position.

Not much to do now, let’s just see where the price can stabilize.

That’s it for today. If you have learned something please subscribe and share to help the newsletter grow.

Cheers,

Nick

The Ecoinometrics newsletter decrypts Bitcoin’s place in the global financial system. If you want to get an edge in understanding the future of finance you only have to do two things:

Click on the subscribe button right below.

Done? That’s great! Now let’s dive in.

I finally understad this chart CME Bitcoin Derivates - Retail Traders'

The sentiment was already set before Elon Musk spells.

Thank you! Well articulated... Much appreciated...