Ecoinometrics - January 20, 2021

Real Yield...

Institutional investors are entering the Bitcoin market.

Given the amount of cash they can bring into the space it is probably worth considering why they might want to include Bitcoin in their portfolio.

One of those reasons is the real yield...

The Ecoinometrics newsletter decrypts Bitcoin’s place in the global financial system. If you want to get an edge in understanding the future of finance you only have to do two things:

Click on the subscribe button right below.

Done? That’s great! Now let’s dive in.

Real Yield

Institutional investors usually don’t invest in a single asset. They run a more or less (often less) diversified portfolio.

You’ll find them holding mostly stocks and bonds. Sometimes they will add exposure to gold and commodities.

So where does Bitcoin fit in that picture?

To see that we need to go back to the narrative. What is the value proposition of Bitcoin for investors?

These days the dominant narrative is that Bitcoin is digital gold. That means Bitcoin as an asset is sold as being a store of value, a hedge against inflation.

Ok.

Then Bitcoin is mainly competing against two things:

- Gold since they are both stores of value.

- Bonds since you might prefer to hold those if you aren't worried about inflation or default risk.

How do you decide as an institutional investor if you want to buy gold or Bitcoin?

You look at the real yield.

Take the US 10-Year Treasury rate and subtract from it the CPI inflation. The result is the yield you get from those Treasury bonds after taking inflation into account. That's the real yield.

Say you have some cash. You need to decide what to do with it:

- If you sit on that cash inflation will erode your purchasing power.

- If the real yield is positive then you might want to hold some bonds to farm that yield.

- If the real yield is negative then there is nothing to milk from those bonds so you might as well buy a store of value like gold or Bitcoin to preserve your purchasing power.

I'm simplifying a little bit but you get the idea.

When bonds have a negative real yield or trend in that direction you are more likely than not to see cash that would have gone to the bonds market be deployed on stores of value instead.

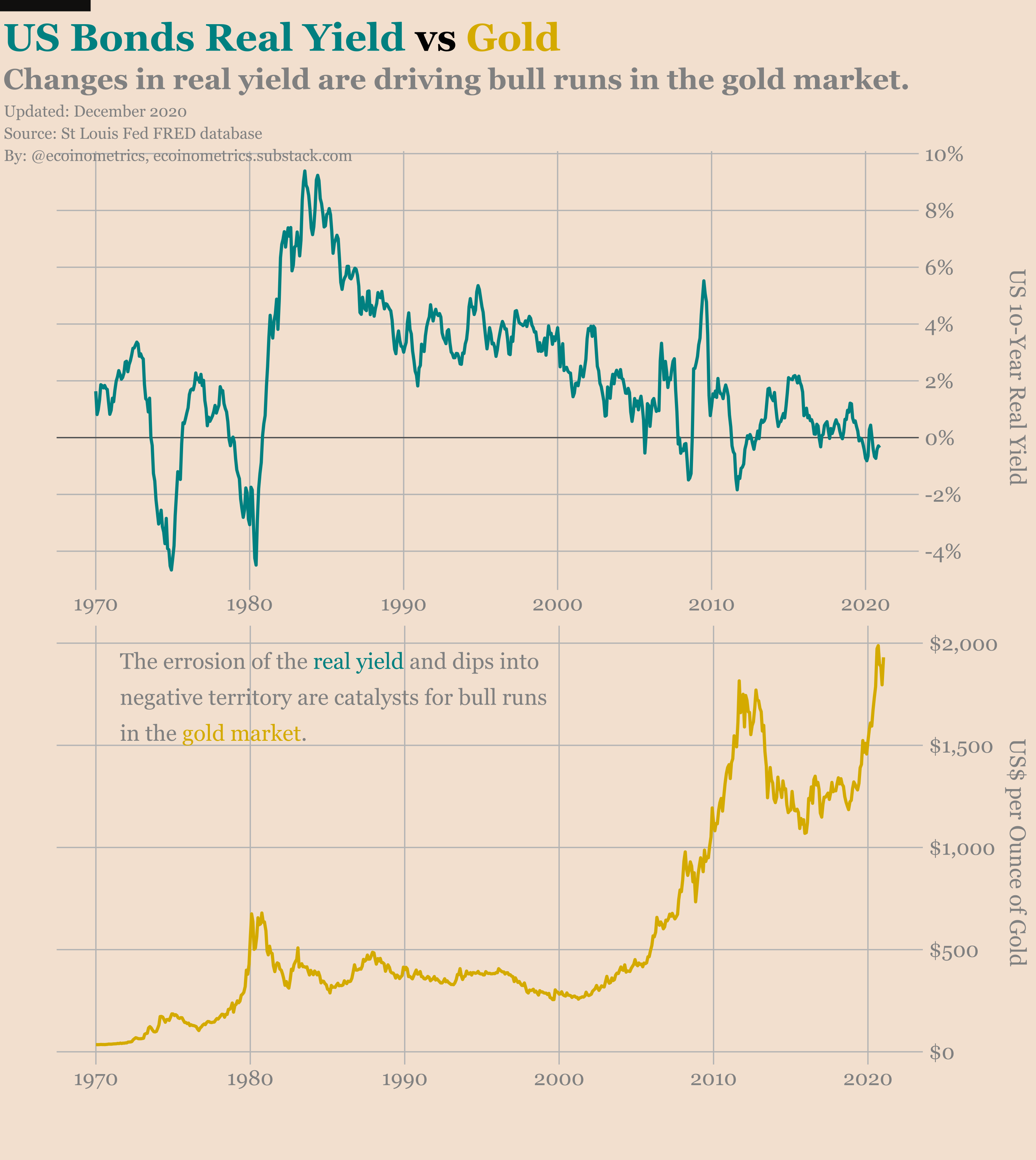

There is a long history of that for gold. Check it out.

You can follow on the chart.

The 1970s were a decade of large inflation in the US which kept the real yield low or negative for long periods of time. Of course this coincided with the great boom of gold.

But a sudden rise in the real yield starting in 1981 stopped the gold bull run. That was the start of the bonds bull market which has been ongoing for 40 years…

In the mid 2000s the real yield was once more closing in on zero. And at this point the gold trade became tempting again. That all stopped when we got out of the great recession and the real yield seemed to move back up.

Gold bottomed in the mid 2010s when the real yield topped. Since then gold is back in business.

Of course the real yield doesn’t predict everything. But when the real yield is negative (or simply looks like it might become negative) you can bet that institutional investors are looking to park some of their cash outside of the bond market.

That doesn’t mean they would drop all their US Treasury bonds for gold and Bitcoin. But that means they’ll start allocating a fraction of their portfolio to assets that act as a store of value.

So where are we now?

The real yield of the US 10-Year Treasury is negative. Gold is up. Bitcoin is up.

And where are we going?

I’ve touched on that last Monday, with the Biden administration now in charge we have a trifecta in the US:

Janet Yellen is Treasury Secretary.

Jerome Powell is Chairman of the Fed.

Bernie Sanders is Chairman of the Senate Budget Committee.

Another way of writing that would be:

Stimulus (Janet Yellen).

Debt monetization (Jerome Powell).

MMT (Bernie Sanders).

If you had any doubt regarding what will happen, Janet Yellen is spelling it out for you:

The net result is likely to be:

More money distributed in the system using MMT principles (say UBI) thus increasing the risk of a rising inflation.

An always rising debt requiring yield curve control to be manageable i.e. rates will be capped by the Fed.

Yield capped with rising inflation means declining real yield. And the real yield is already starting negative...

Tl;dr this is good for Bitcoin.

CME Bitcoin Derivatives

Let’s talk about the CME Bitcoin derivatives… *yawn* … I mean things are really boring around here.

Bitcoin goes up, the positions are unchanged.

Bitcoin goes down, the positions are unchanged.

For months we have been seeing the same thing play out, the same strategy being milked.

Traders are in their majority positioned to take advantage of the futures premium over the spot market.

Buy BTC in the spot market. Sell BTC futures. Pocket the difference. Roll and repeat.

There is almost nothing else going on in the market these days. After all, this trade makes money so if it ain’t broke don’t fix it.

We have 10 days to go on the January contract which means traders are going to start to roll over their positions. We’ll have to see what it does to the spread.

The options side of things is as boring as the futures. The market is positioned bullish with 5 calls for every 2 puts.

With Bitcoin trading sideways in the $35,000 to $40,000 range we can expect that 65% of the calls on the January contract are going to expire in the money next week.

Compared to last week’s Commitment of Traders report nothing has changed for the smart money but retail traders have suddenly increased the size of their long positions.

That’s it for today. If you have learned something please subscribe and share to help the newsletter grow.

Cheers,

Nick

The Ecoinometrics newsletter decrypts Bitcoin’s place in the global financial system. If you want to get an edge in understanding the future of finance you only have to do two things:

Click on the subscribe button right below.

Done? That’s great!